Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s agriculture topics include:

- Soybeans: Arkansas farmers shift heavily toward soybeans—up roughly 20% in projected acreage—as rising input costs make soybeans the only crop with potential positive returns, raising concerns about oversupply and harvest‑time price pressure.

- Corn: Fertilizer prices surge due to disruptions in the Strait of Hormuz, adding up to $35 per acre for U.S. corn and pressuring farm economics as futures slide and global buyers increase tender activity.

- Wheat: Ukraine deepens its push into African markets as Ghana considers a new wheat‑processing plant, part of a broader shift toward domestic food production amid rising import dependence and global supply shocks.

- Wild Card: The effective closure of the Strait of Hormuz triggers a global fertilizer shock, with urea up ~$80/ton and nitrogen markets tightening sharply, prompting farmers worldwide to cut application rates and pivot toward lower‑input crops.

Let’s begin.

Soybeans

Source: Fundamental Analytics

Arkansas farmers shift to soybeans amid rising costs

Jake Tester, K8 News

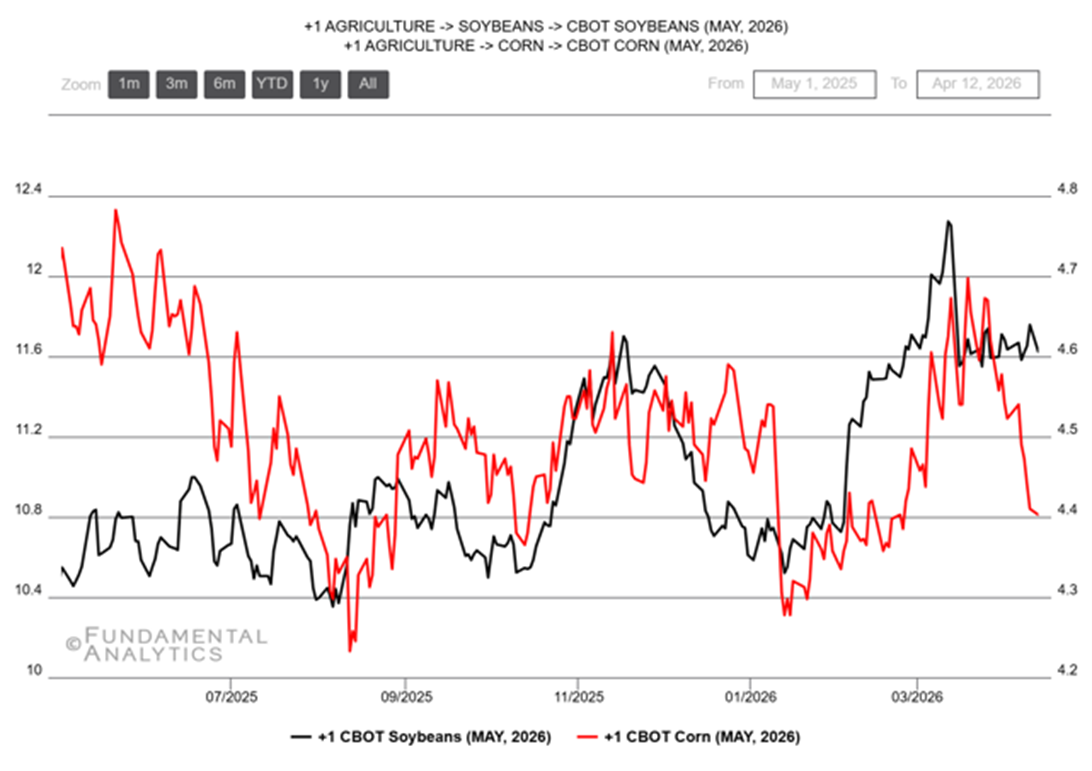

Arkansas farmers have shifted heavily toward soybeans in the 2026 planting season. On average, USDA projects have seen a 20% increase in soybean acreage coupled with a 22% and 27% decrease in rice and corn. Soybeans are viewed as the only crop with potential positive returns with the surge in input costs. Farmer sentiment signals a shift defined by the need for survival rather than the pursuit of optimization. Movements toward lowest cost, lease input intensive crops are emerging across a multitude of agriculture dependent states. For the markets, this means a risk of oversupply if all farmers move to soybeans and a potential price collapse at harvest due to the oversupply. The “don’t put all your eggs in one basket” dynamic is beginning to emerge. Farmers with forward contracts may be better insulated, but severe financial stress across the community looks inevitable. Profitability challenges are especially acute for rice at current prices. Final USDA acreage data is pending for later in the summer, but narrow margins and elevated volatility already seem to be a guarantee. In the chart below, you can see the volatility that informs the trade-off between corn and soybeans as well as the unstable situation present despite increasing price differences after May.

Corn

Source: Fundamental Analytics

Corn Slipping on Thursday, as USDA Raises World Stocks

Austin Schroeder, Barchart

Here are 4 post-WASDE marketing tips

J.D. Schuerman, Farm Progress

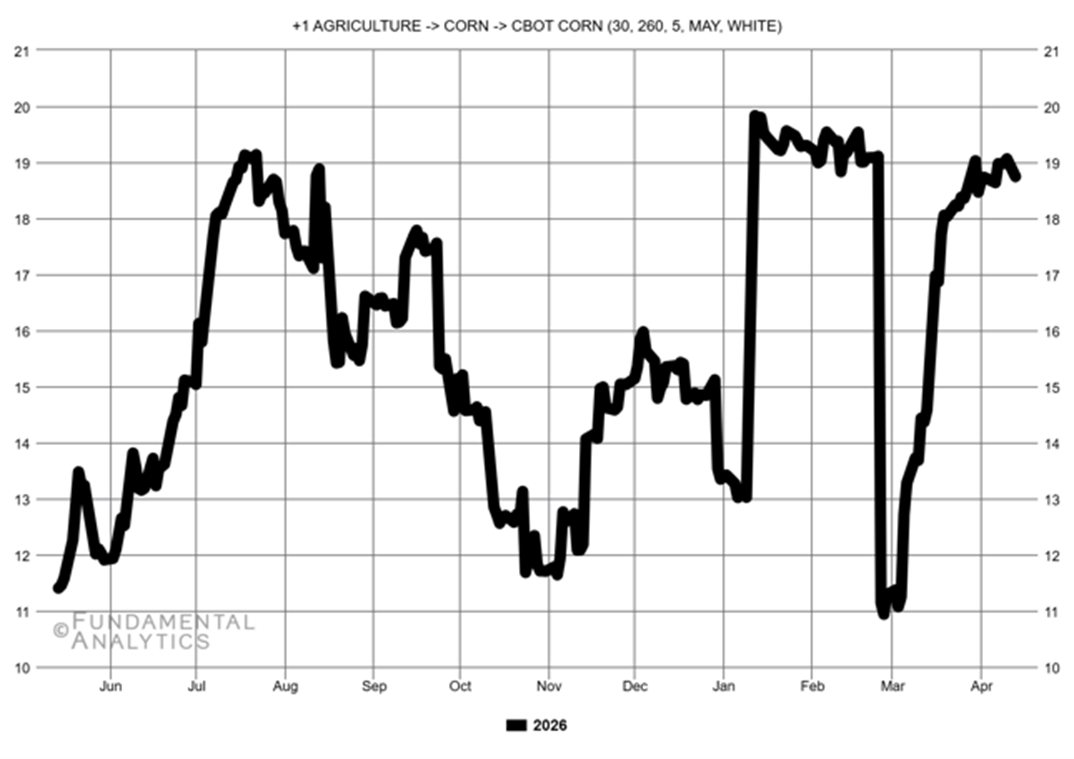

The supply chain disruptions in the Strait of Hormuz have driven sharp increases in fertilizer prices adding up to $35 per acre for US corn. The subsequent outlook for 2026 includes widespread demand destruction, pressure on farm economics, risk to crop production, and food price stability. As of April 9th, corn futures were trading with 3-5% losses at midday and the average cash corn price was down 4 cents. South Korean importers purchased 136,000 MT of corn in tenders overnight, following the purchases from the day before. USDA’s flash reporting system suggested it was US origin, reporting a private sector sale to South Korea. Note the major volatility in futures after January shown below. The April USDA WASDE report showed largely unchanged balance sheets with corn ending at 2.127 billion bushels. Corn demand is robust, but profits seem weak compared to soybeans, therefore supply is not matching demand for exports.

Wheat

Source: Fundamental Analytics

Source: United States Department of Agriculture

Ukraine moves into Africa’s food supply chain with Ghana wheat plant plan

Ayodeji Adegboyega, Business Insider Africa

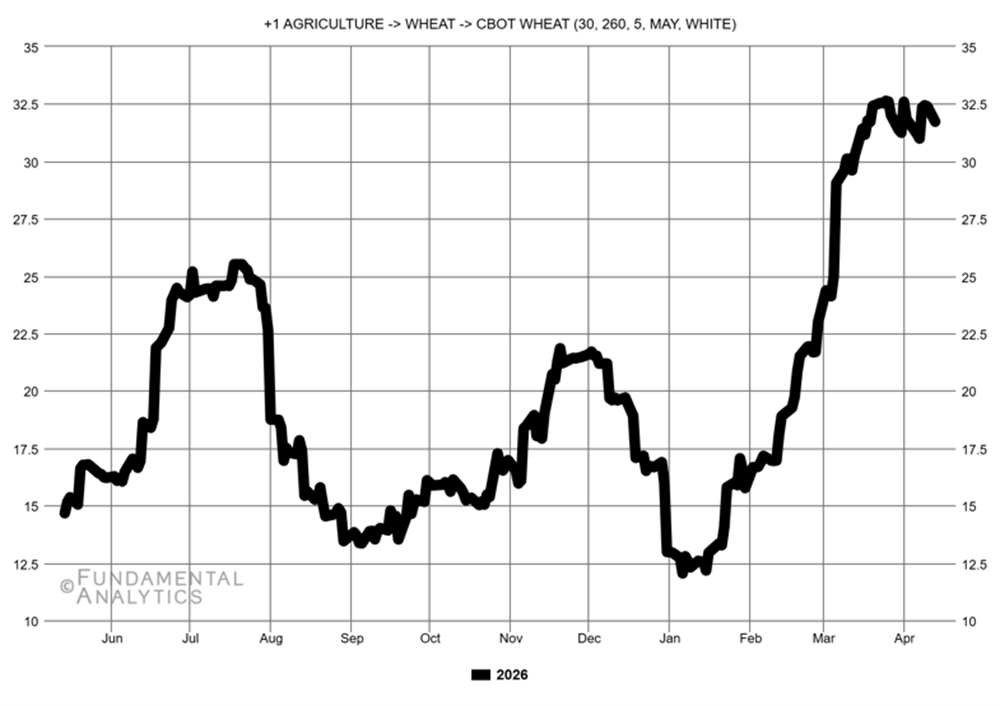

Ghana and Ukraine have begun discussions around a potential wheat processing plant to limit their export dependence. This comes as a part of a broader shift in African development as countries are pushing to enhance domestic food production in response to multiple global supply shocks. Wheat demand is rising fast, with imports up nearly 57% over the past four years. Simultaneously, Ukraine has shifted its own export strategy and is expanding into new markets. The proposal was discussed between Ghana’s Agriculture Minister, Eric Opoku and Ukraine’s Deputy Minister, Denys Bashlyk. This agreement would solidify Ghana as a central hub for Ukrainian agricultural products across West Africa. Ukraine is one of the world’s largest wheat exporters, having exported over 20 million tons of wheat in 2024 despite the Russia-Ukraine war. Kyiv hopes to deepen its ties with African economies through its “Food from Ukraine” initiative, which in this case works in parallel with Ghana’s “Feed Ghana Program” focusing on domestic development and reduced reliance on imports. In comparison to common core periphery disadvantageous terms of trade, Ukraine is building domestic production capacity within the African country, rather than perpetuating import reliance.

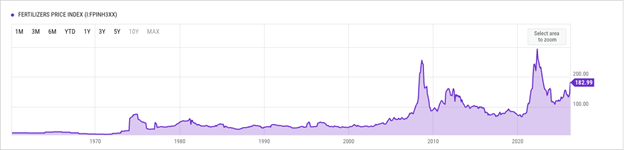

Wild Card

Source:YCharts

Iran war’s impact on fertilizer and fuel

Sharon Kits Kimathi, Reuters

Fertilizer spike adds up to $35/acre for US corn as Iran crisis deepens

Elaine Watson, Ag Funder News

The effective closure of the Strait of Hormuz amid the Iran conflict has triggered a global fertilizer shock, tightened an already constrained market and is pushing prices sharply higher, with urea rising roughly $80 per ton from around $470 and European prices up about 40% for urea, 15 to 20% for nitrates, and 12% for ammonia. The disruption is particularly acute given that roughly one third of global fertilizer trade and as much as 30% of urea, 27% of ammonia, 24% of phosphates, and 48% of sulfur exports transit the corridor, while production remains highly energy intensive with natural gas accounting for up to 70% of costs. Nitrogen markets are the most exposed, with urea accounting for over 50% of global nitrogen fertilizer use, driving significant cost pressures at the farm level including increases of up to $35 per acre for US corn. In response, farmers globally are reducing application rates and shifting toward less input intensive crops, with US producers cutting corn acreage in favor of soybeans and Australian growers pivoting toward barley, raising risks of lower yields and broader “demand destruction.” Trade flows are beginning to realign, with North African suppliers such as Egypt, Algeria, and Morocco gaining influence and Nigeria expanding exports to Atlantic markets, while Brazil, which imports roughly 90% of its fertilizer, and South Asia remain highly exposed to prolonged disruptions. Although China’s coal-based production provides some insulation, export restrictions may further tighten global supply, leaving the 2026 outlook characterized by sustained pressure on farm economics, potential declines in crop production, and increased volatility in global food prices.

Trading Implications

Rising fertilizer costs are driving a global shift toward lower input crops like soybeans, creating a divergence where corn demand remains strong, but supply growth is constrained by weak farm profitability, while soybeans face increasing risk of oversupply and price pressure at harvest. The combination of input-driven acreage shifts, volatile fertilizer markets, and strong but uneven demand suggests tighter margins and higher price volatility across major crops into 2026.