Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s energy topics include:

- Corn: European corn prices hit a nine-month high, driven by stronger CBOT futures, elevated freight rates, and supply quality concerns out of Ukraine.

- Soybeans: CBOT soybean oil futures surged to their highest level since November 2022 as Southeast Asian biodiesel mandates tighten palm oil availability.

- Wheat: Grain markets sold off sharply alongside crude oil on Middle East peace talk headlines, unwinding war risk premium and triggering technical resistance across Chicago and Kansas City contracts

- Wild Card: Indian rice exporters face mounting cost pressure from diesel shortages and potential domestic fuel price hikes, compounding an already weak demand environment that has pushed parboiled rice prices to a multiyear low.

Let’s begin.

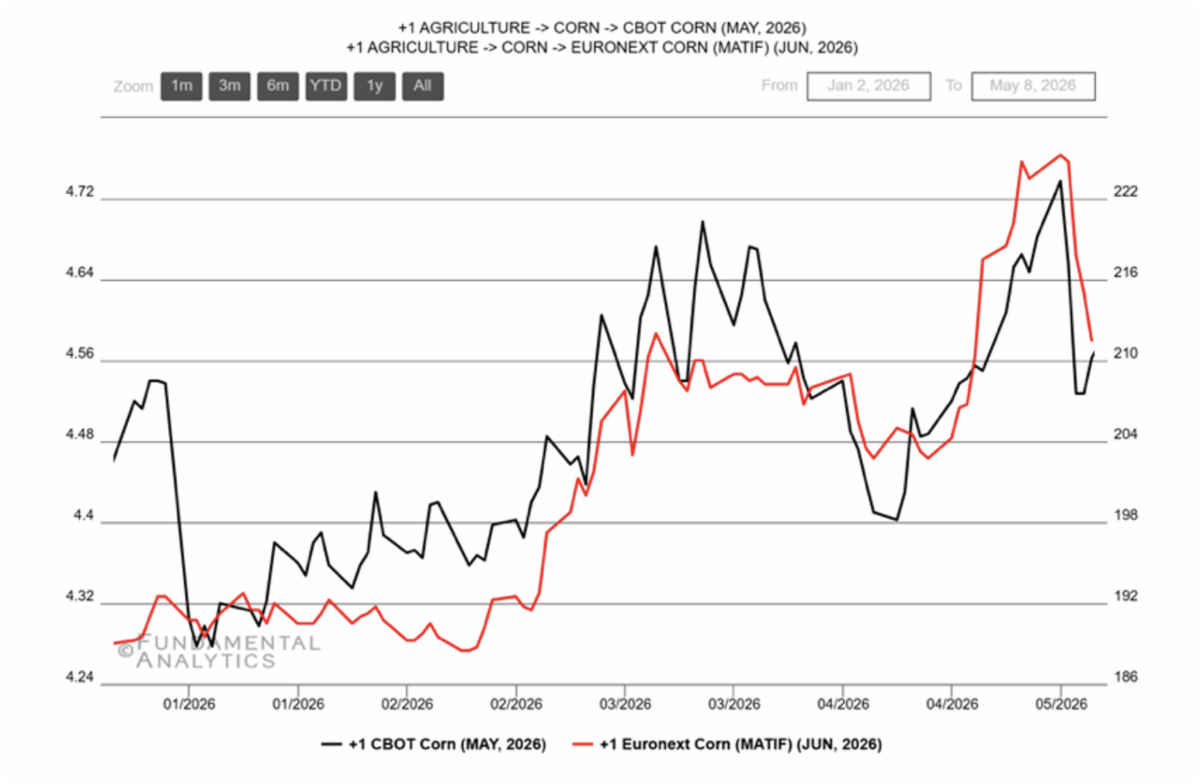

Corn

Source: Fundamental Analytics

European Corn Prices Hit 9-Month High on Increased Costs, Stronger CBOT Futures

Nanditha Kinavoor Madathil, S&P Global

European corn prices rallied to a nine-month high on May 5, driven by higher origin costs, elevated freight rates, and strengthening CBOT futures. Platts assessed ex-works Tarragona corn at €230.50/mt — the highest since late July 2025 — with offers ranging up to €234/mt. Market participants cited strong U.S. domestic and export demand as the primary CBOT driver. A notable supply quality concern emerged from Ukraine, where some unharvested corn reportedly deteriorated due to frost, prompting Dutch buyers to increasingly favor French corn despite a €7–8/mt premium. Across Spain, Italy, and the Netherlands, buyers remained cautious and were largely holding back purchases unless urgent, even as stock levels tightened.

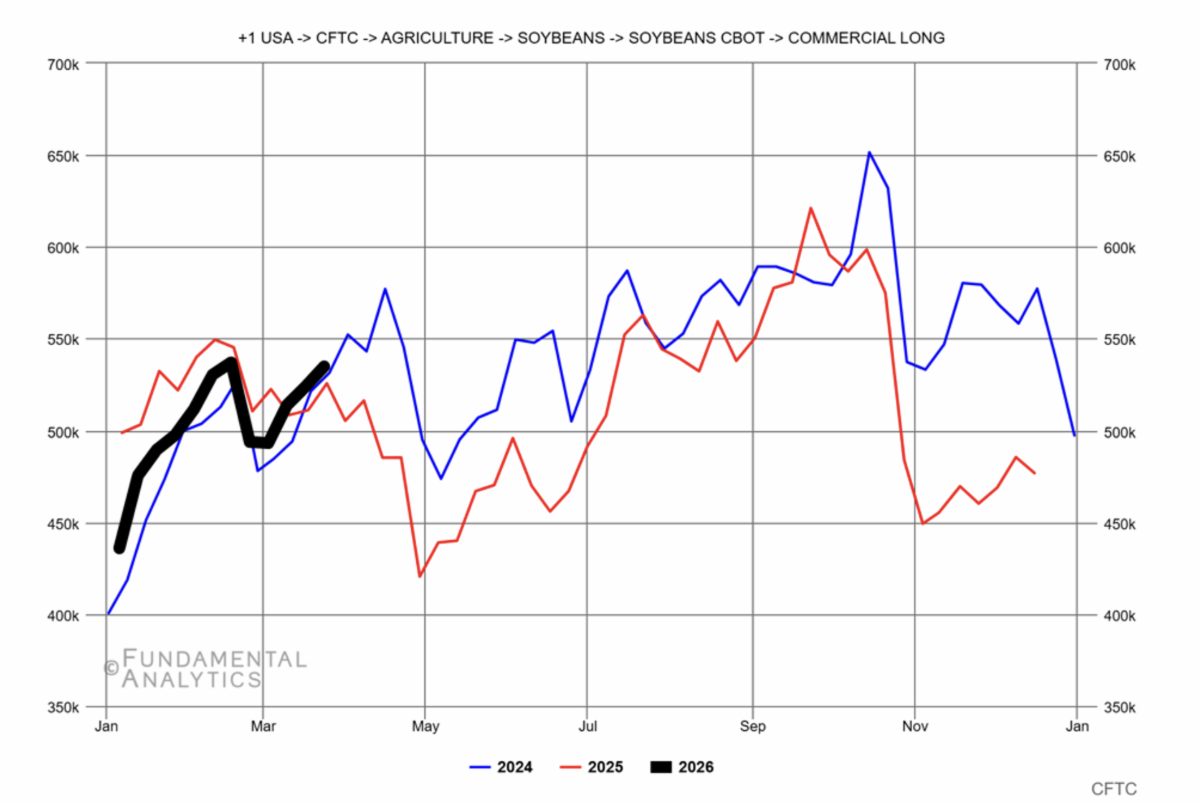

Soybeans

Source: Fundamental Analytics

South American Soybean Oil Gains Competitiveness into Asia

Phillip Herring, S&P Global

Global vegetable oil markets have tightened considerably, with CBOT July soybean oil futures surging above 76 cents/pound in early May, the highest since November 2022. This growth is driven by rising crude oil prices and expanding biofuel demand. Managed money funds held a net-long position of roughly 165,000 contracts in CBOT soybean oil as of late April, reflecting strong speculative interest. A key structural driver is Southeast Asia’s accelerating biodiesel ambitions: Indonesia’s B50 mandate takes effect July 1, while Malaysia is pushing blending rates beyond its current B10 program. These policy shifts are tightening palm oil export availability and strengthening the broader vegetable oil complex. Despite soybean oil’s improved flat-price competitiveness, large-scale arbitrage into Asia remains constrained by freight rates reported near $130/mt on key export routes. On the supply side, record South American crushing activity is keeping physical markets under pressure. Argentina’s FOB Up River June basis was assessed at minus 2,370 points to CBOT July futures on May 5, and Brazil’s Paranaguá at minus 2,250 points. Brazil’s soybean oil biodiesel feedstock use reached 573,000 mt in March, accounting for 72% of total biodiesel feedstock — the highest share since August 2025 — while April vegetable oil exports ran roughly 61% above year-earlier levels. CFTC commercial long positioning in 2026 (shown in black on the chart) is tracking closely with prior-year levels through mid-March before edging higher, consistent with the market’s bullish tilt heading into the spring.

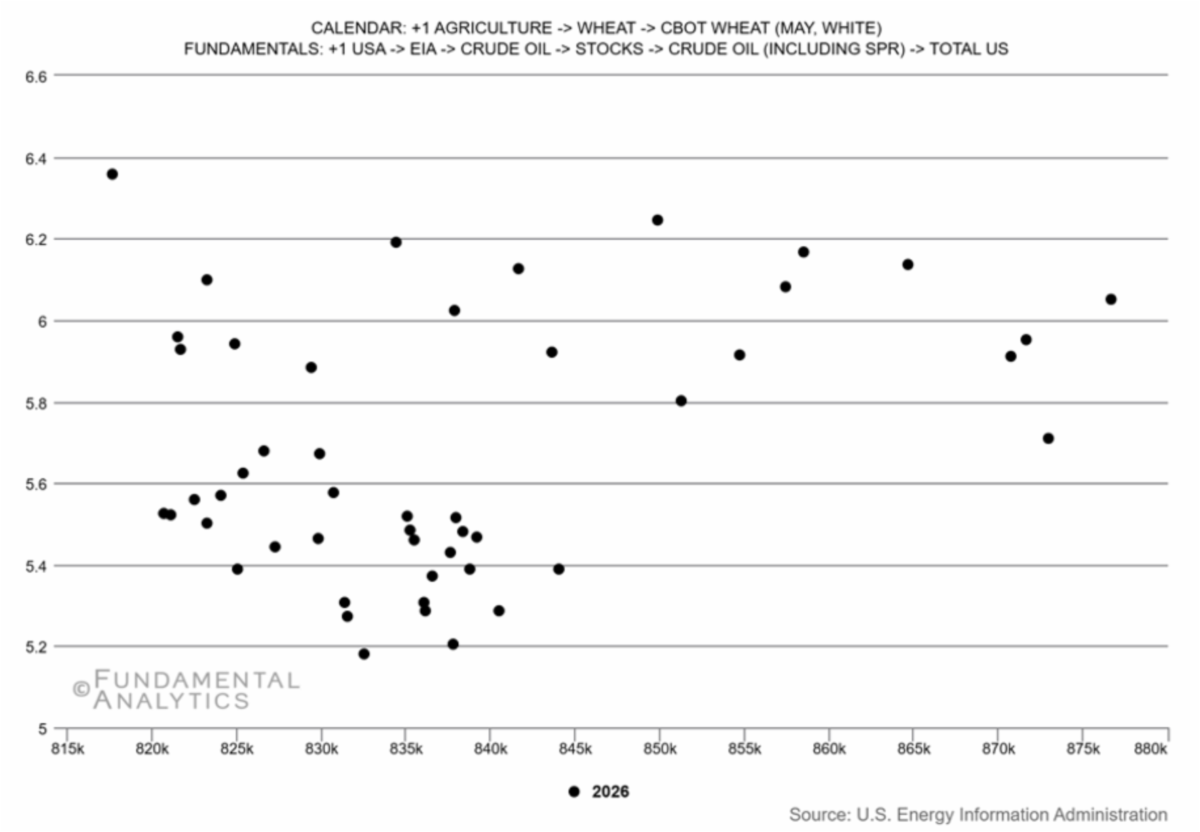

Wheat

Source: Fundamental Analytics

Grains Plunge with Oil, Peace Talks: Is the Rally Over?

Michelle Rook, AgWeb Farm Journal

Wheat markets sold off alongside crude oil after headlines emerged around Middle East peace talks and a potential reopening of the Strait of Hormuz, unwinding the war risk premium that had been supporting grain prices. Oliver Sloup of Blue Line Futures noted that while grains had been attempting to trade on their own fundamentals in recent weeks, they snapped back to trading in lockstep with energy markets on the news. The Chicago wheat contract faces key technical support at the $6.10–$6.16 range — the 20- and 50-day moving averages — with a close below that level potentially opening another 30 cents of downside. Kansas City wheat’s line in the sand is $6.60, the prior breakout point, and holding above it would keep the bullish structure of higher highs and higher lows intact. Despite the near-term weakness, Sloup does not view the broader grain rally as finished, citing ongoing uncertainties around acreage, yield, and fertilizer costs as reasons managed money will continue finding reasons to buy on dips. The scatter chart plots CBOT May wheat futures prices against total U.S. crude oil stocks, including the SPR, throughout 2026, illustrating the energy-grain relationship at the core of this week’s selloff — wheat prices have generally clustered between $5.20 and $6.40 across a crude stock range of 815k–880k barrels, with no dominant directional trend, suggesting the correlation is episodic rather than structural.

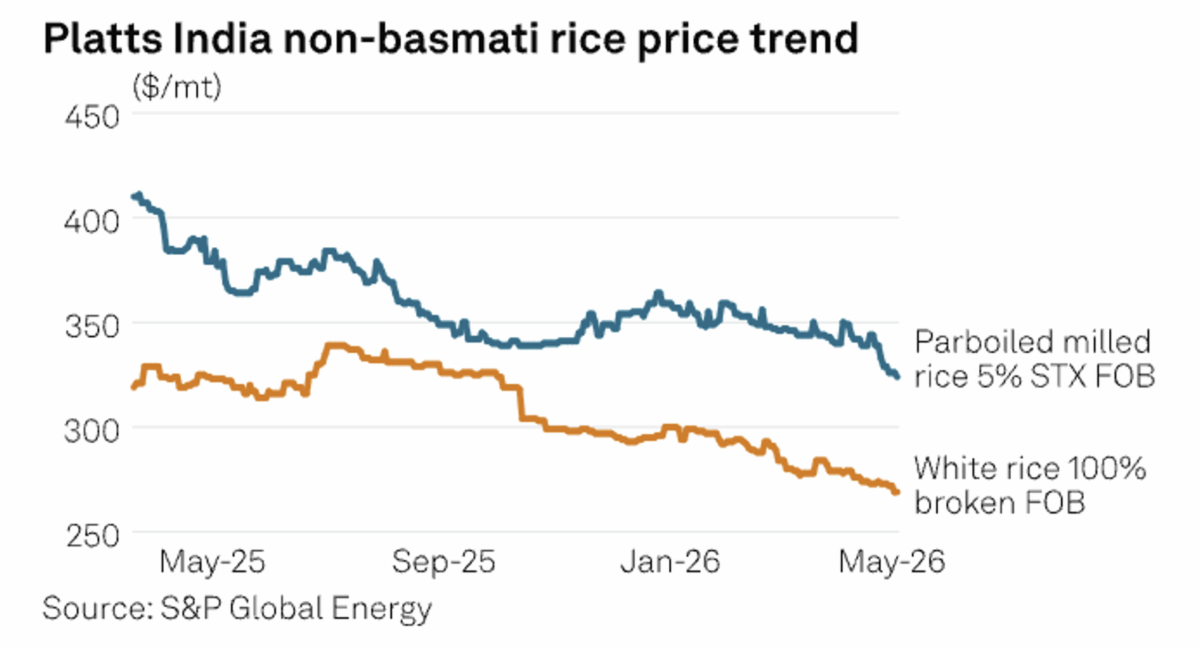

Wild Card

Source: S&P Global

Indian Rice Exporters Fear Cost Surge from Potential Domestic Fuel Hike

Namarita Kathait, S&P Global

Indian rice exporters are facing a compounding set of logistical pressures as potential domestic fuel price hikes threaten to worsen already strained trucking conditions. Prime Minister Modi’s May 10 call for economic self-reliance and reduced imported fuel consumption has fueled market expectations of an imminent diesel price increase, with one Madhya Pradesh-based exporter noting a hike could come “any time soon.” Trucking rates have already risen across most factory-to-port routes due to ongoing diesel shortages and a pan-India dearth of trucks, squeezing margins on lower-value commodities like rice, where logistics constitute a significant share of landed cost. The pressure is not confined to origin ports — a Kribhco Agri Business official noted that cargo sitting in bonded warehouses at destination ports is also stranded, as local trucks cannot access sufficient diesel to move goods to customers. These supply-side cost pressures are colliding with weak international demand, leaving millers and exporters likely to absorb any further cost increases rather than pass them through to buyers. Platts assessed Indian parboiled 5% rice at $324/mt FOB on May 11, down $20/mt month over month and at a multiyear low, underscoring the difficult pricing environment. The Rice Exporters Association of Chhattisgarh has already petitioned APEDA and state authorities to extend logistics subsidies through the inland container depot Raipur, as exporters seek relief from the mounting cost burden.

Trading Implications

Energy market volatility and biofuel policy dominated this week’s agricultural complex. Crude oil’s sell-off on Middle East peace talk headlines dragged grains lower in tandem, though constructive managed money positioning and uncertainties around acreage, fertilizer, and the May 14–15 U.S.-China trade talks should keep dip-buying interest alive in new crop contracts. Soybean oil’s multi-year highs reflect a genuine demand shift from Southeast Asian biodiesel mandates, but elevated freight rates continue to cap arbitrage flows into Asia. Indian rice exporters face a compounding margin squeeze from weak global demand and rising logistics costs, with FOB values at multiyear lows and no quick resolution in sight.