|

Source: Bloomberg

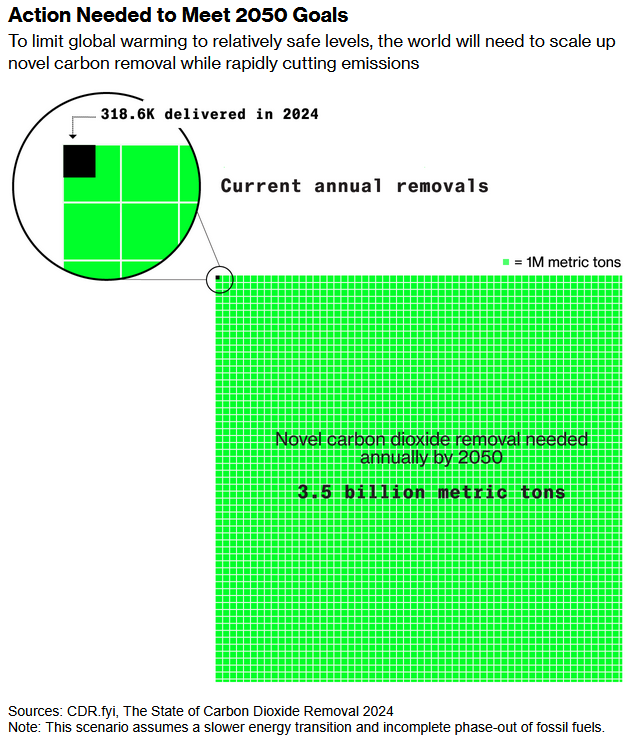

However, this growth is not immune to challenges, particularly as federal support for clean energy initiatives hangs in the balance. The overwhelming reliance on direct air capture (DAC) and bioenergy with carbon capture and storage (BECCS) in carbon removal investment reflects a narrow focus that risks excluding alternative technologies that could offer greater potential.

One of the critical issues with this investment strategy is the disproportionate emphasis on DAC and BECCS, which have garnered substantial financial backing due to federal tax credits and their perceived scalability. These methods dominate despite concerns about their efficiency, high energy use, and problematic carbon accounting. Enhanced weathering and ocean alkalinity processes, for instance, remain underfunded despite their promise of durability and scalability in capturing and storing CO₂. Critics argue that reliance on DAC, buoyed by the oil and gas industry’s influence, limits innovation and undermines efforts to diversify the carbon removal landscape.

The lack of diversity among buyers of carbon removal credits further compounds the issue, with companies like Microsoft responsible for the majority of purchases to date. This concentration risks stunting the industry’s growth and the scaling of novel technologies beyond pilot projects. Moreover, carbon removal should primarily target legacy emissions and the unavoidable emissions from sectors like aviation and agriculture. Using captured CO₂ for purposes such as extracting fossil fuels is not only counterproductive but must be rapidly curtailed to ensure the industry’s integrity and effectiveness.

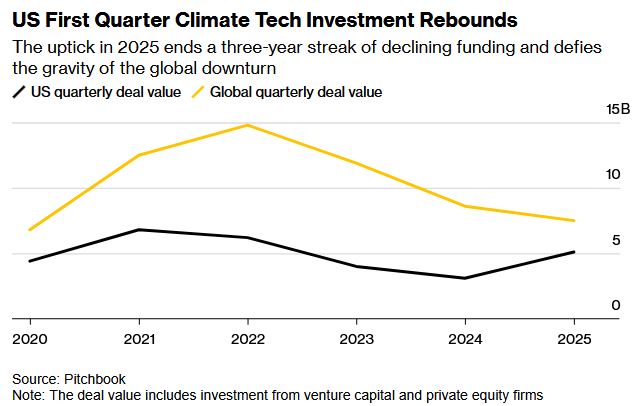

Political uncertainty adds another layer of complexity, especially for the U.S. climate tech sector. The Trump administration’s potential rollback of the Inflation Reduction Act and its moratorium on certain clean energy funding programs create an unstable environment for startups relying on government support. Green hydrogen and direct air capture projects are particularly vulnerable, with private equity unlikely to bridge the funding gap left by reduced federal involvement. Stable and consistent policy frameworks are essential to maintain momentum in decarbonization efforts and provide confidence to investors and entrepreneurs alike.

In response to these challenges, climate tech companies are adapting their strategies, including rebranding efforts to align with the administration’s rhetoric. This shift illustrates the sector’s resilience and innovation, as companies find ways to navigate turbulent political landscapes while continuing to contribute to climate goals. However, true progress in climate tech and carbon removal requires a unified effort to diversify investments, prioritize scalable and verifiable technologies, and address immediate emissions reductions alongside legacy emissions. |