|

The global soybean market faces a complex landscape of competing pressures as the 2025 growing season unfolds. While U.S. farmers have achieved strong planting progress with 84% of acres seeded by mid-May—seven percentage points ahead of last year’s pace—the market remains dominated by South American production powerhouses Brazil and Argentina, which together control over half of global soybean trade. Despite improved U.S. yield projections and a partial easing of trade tensions with China through reduced tariffs, American soybean exports continue to lose market share to more competitively priced Brazilian supplies. With breakeven prices for U.S. farmers hovering above current futures levels and weather uncertainties looming across key growing regions, the soybean sector finds itself navigating between promising production fundamentals and persistent profitability challenges in an increasingly competitive global marketplace.

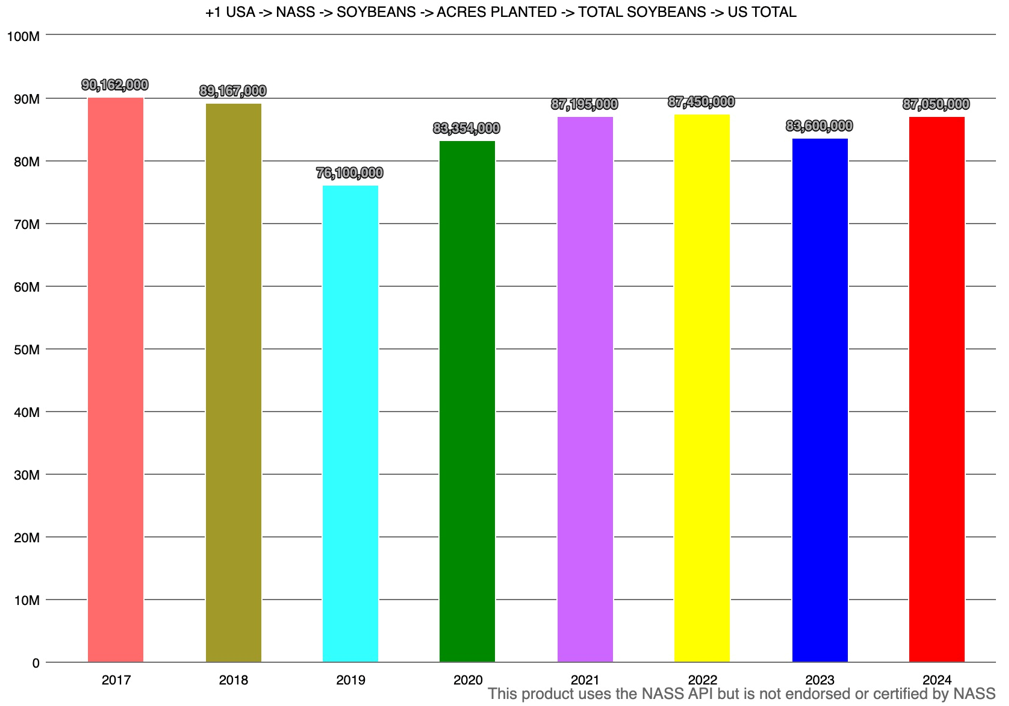

U.S. Soybean Planting ProgressAs of May 19, 2025, the USDA reported that 84% of soybean acres had been planted, ahead of last year’s total by 7%. Early planting typically boosts yield potential. According to the May World Agricultural Supply and Demand Estimates (WASDE) report, 2025/26 soybean yields are projected to rise from 50.7 bushels per acre to 52.5 bushels per acre. However, demand continues to outpace production. Soybean stocks are expected to rise by just 1.2 million metric tons (MMT). Despite reduced acreage of 83.5 million acres (down 4% YoY), total U.S. soybean production is forecast to reach 4.4 billion bushels, up from 4.366 billion bushels in the prior growing season. |

|

|

Acres Devoted to Soybean Production in the US: 2017-2024 Source: Fundamental Analytics

South American Soybean ProductionBrazil’s soybean production is set to hit 169 MMT, according to Brazilian Agribusiness consultancy AgRural, reinforcing Brazil’s export dominance. Brazil and Argentina of collectively command 52% the global soybean trade, with Brazil alone accounting for 40%. Chinese investment exceeding $500 million in Brazilian infrastructure, particularly at the Port of Santos, has solidified this partnership. Brazil’s exports to China have soared 45% from 2.5 billion bushels in 2017 to an expected 3.9 billion in 2025.

Argentina, recovering from last year’s severe drought, was forecast to double soybean output to 50 MMT in 2025. However, mid-May flooding brought up to 400 mm (15.75 inches) of rain to key growing regions, delaying harvests and threatening yields. The heavy rainfall saturated fields, raising risks of disease, seed pod damage, and livestock losses. As the top global exporter of soybean oil and meal, Argentina’s disrupted harvest adds uncertainty to an already volatile market. Despite South American surpluses, weather remains a key risk to final volumes. Argentina recently signed a $900 million non-binding agreement with China for soybeans, corn, and vegetable oil shipments.

Trade Dynamics and Market Share ShiftsA 90-day U.S.-China trade truce reduced tariffs from 125% to 10% on Chinese duties for U.S. goods, but structural pressures remain. U.S. soybean exports to China have fallen from 60% market share in 2017 to around 50% today, despite $12.84 billion in imports in 2024. Even with substantial tariff cuts, U.S. soybean exports are weakening in competitiveness relative to South American exports. Still, U.S. exporters benefit from better overall logistics infrastructure than South American exporters. China imported just 6.08 million metric tons of soybeans in April—a 29.1% year-over-year drop, the lowest monthly total since 2015—due to customs delays and late Brazilian shipments, which also drove January–April imports down 14.6% to 23.19 million tons. These disruptions led to longer delivery times to crushers, from 7–10 days to 20–25 days, forced shutdowns at several northern plants, and tight soymeal supplies. However, China’s imports of soybeans rebounded with a record 13.9 million tons of soybeans in May—more than double April’s volume—sourcing mostly from Brazil as it shifts away from U.S. suppliers to hedge against potential trade war–driven price hikes.

Farmer Economics – SoybeansAccording to the University of Illinois’s Farmdoc Daily, breakeven prices in Illinois range from $10.87–$11.26 for soybeans. With forecasts cast below these levels, profitability hinges on trendline yields. Farmers are shifting acreage, with corn expected to increase 5% to 95.3 million acres while soybean plantings decline to 83.5 million acres.

Weather OutlookAn active weather pattern—driven by a decaying tropical system and several storm fronts—is forecast across much of the U.S. through early June. The Midwest and Central Plains are expected to receive beneficial rainfall, although regions from Oklahoma to the Ohio Valley may face excessive moisture. Meanwhile, the Northern Plains, western Gulf, and Mid-Atlantic could remain dry, raising localized drought concerns. Delays in hot, dry conditions offer short-term crop development support, but uncertainty persists.

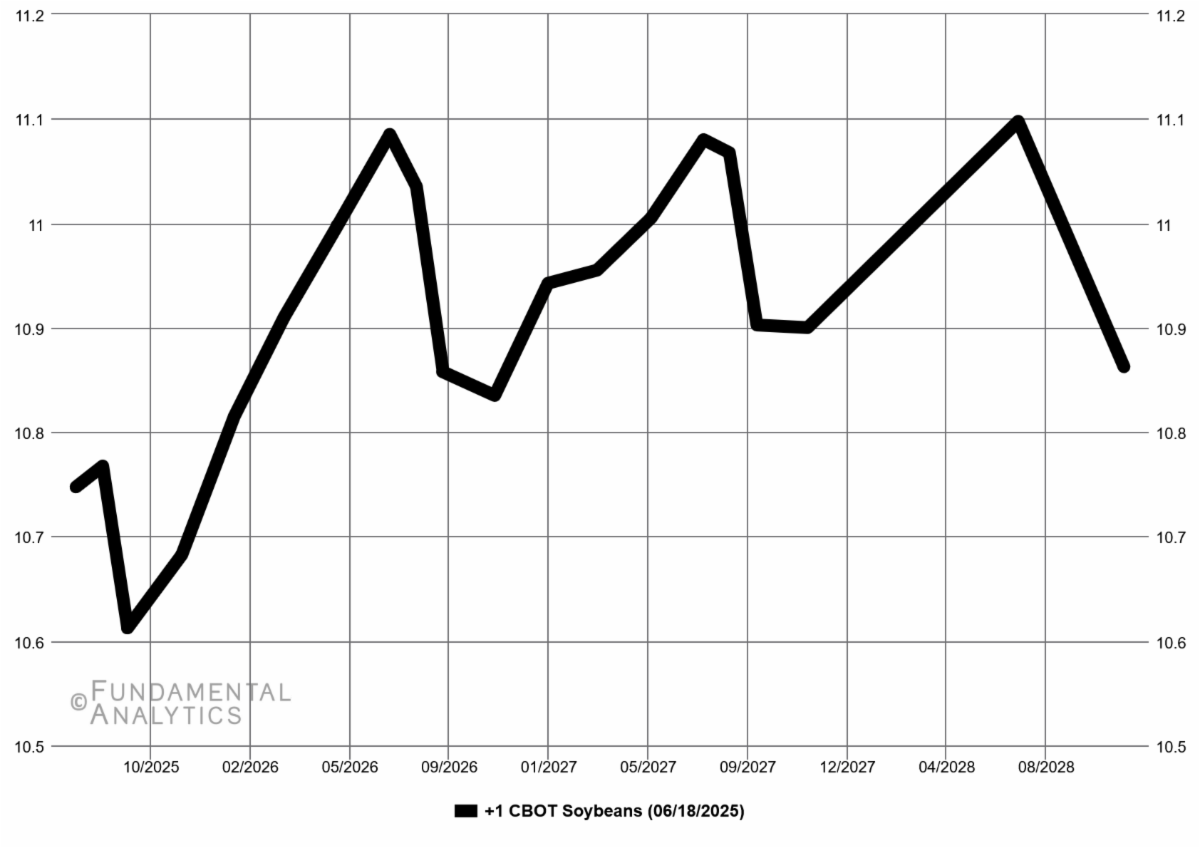

Soybean Price OutlookAccording to the May WASDE, soybeans are forecasted at $10.25/bushel, up from $9.95 in 2024/25. U.S. ending stocks are projected at 460 million bushels (+20% YoY). Futures data as of June 5 suggest limited price volatility for soybeans over the next year, with expected fluctuations under $0.50 per bushel unless supply shocks emerge. China’s demand remains massive at 109 MMTs expected for 2024-25, but the country sources roughly 70% from tariff-free Brazilian supplies, providing little incentive to return to pricier but higher quality U.S. beans. |

|

|

CBOT Soybeans Futures Source: Fundamental Analytics |