|

Grain futures softened overall as ample Northern Hemisphere harvests, USDA acreage shifts, heat-induced yield risks, and uneven export demand—tempered by logistical hiccups—kept markets range-bound ahead of July holidays, denting trade. |

|

|

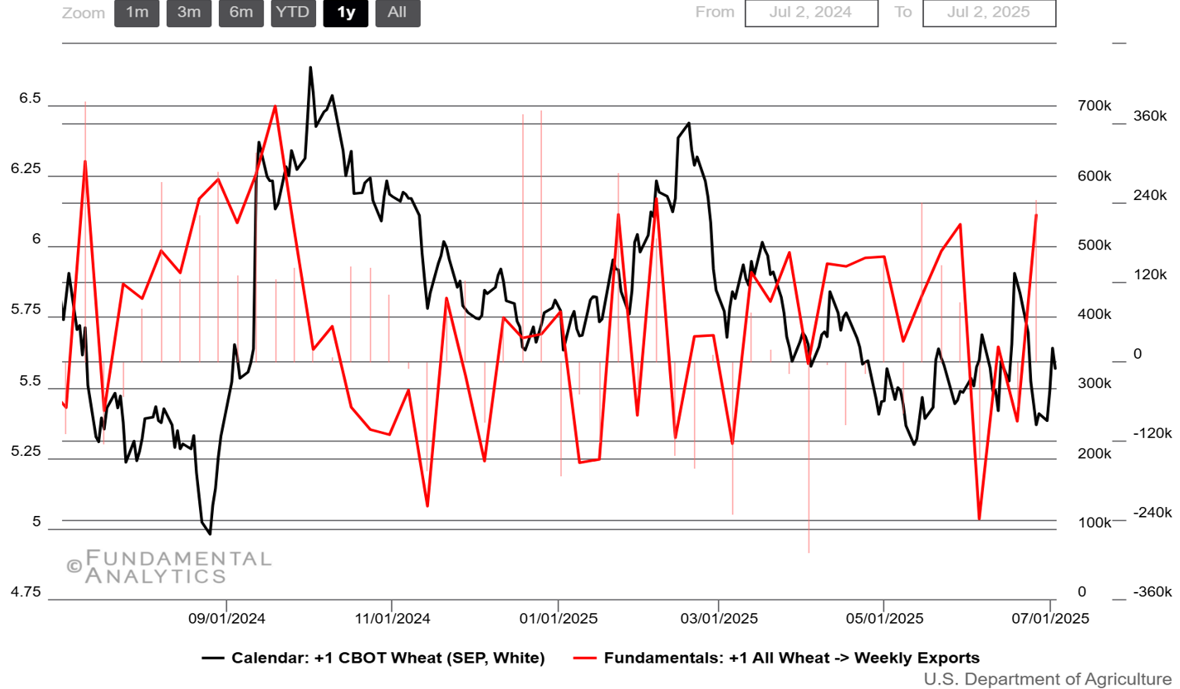

Wheat |

|

Wheat prices near two-week high, driven by advancing US winter harvests |

|

|

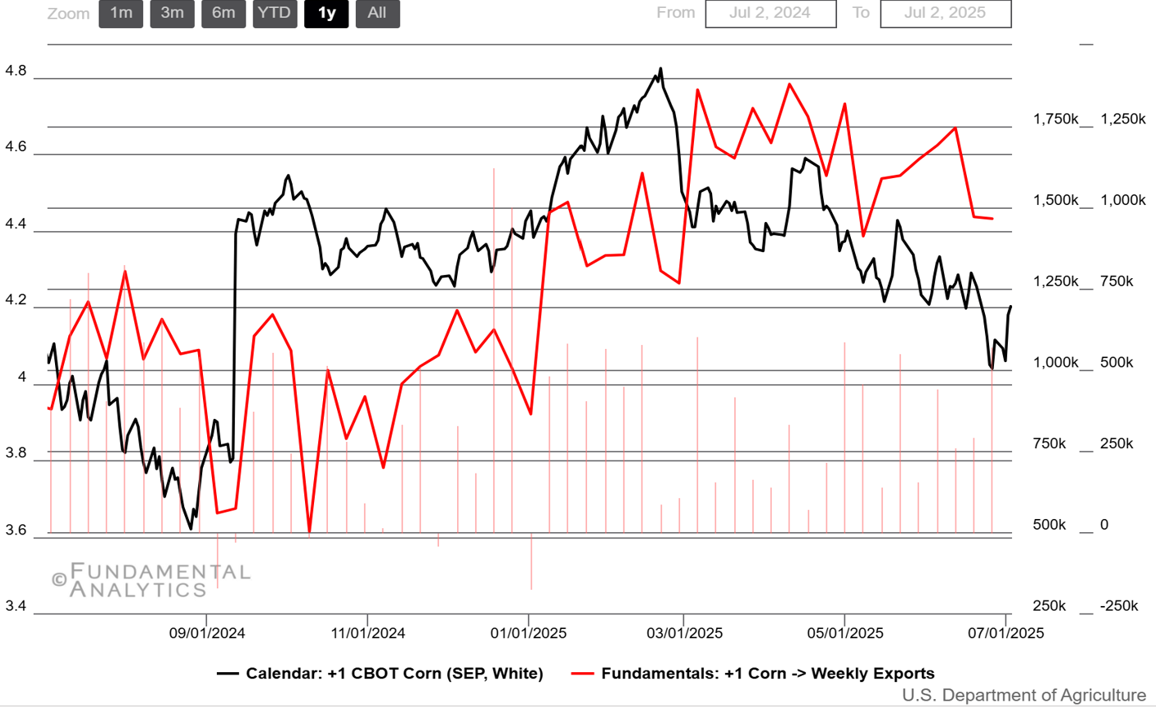

Corn |

|

Corn futures climbed above the $4.20 mark, recovering from six-month lows as tightening supplies converged with resilient demand |

|

|

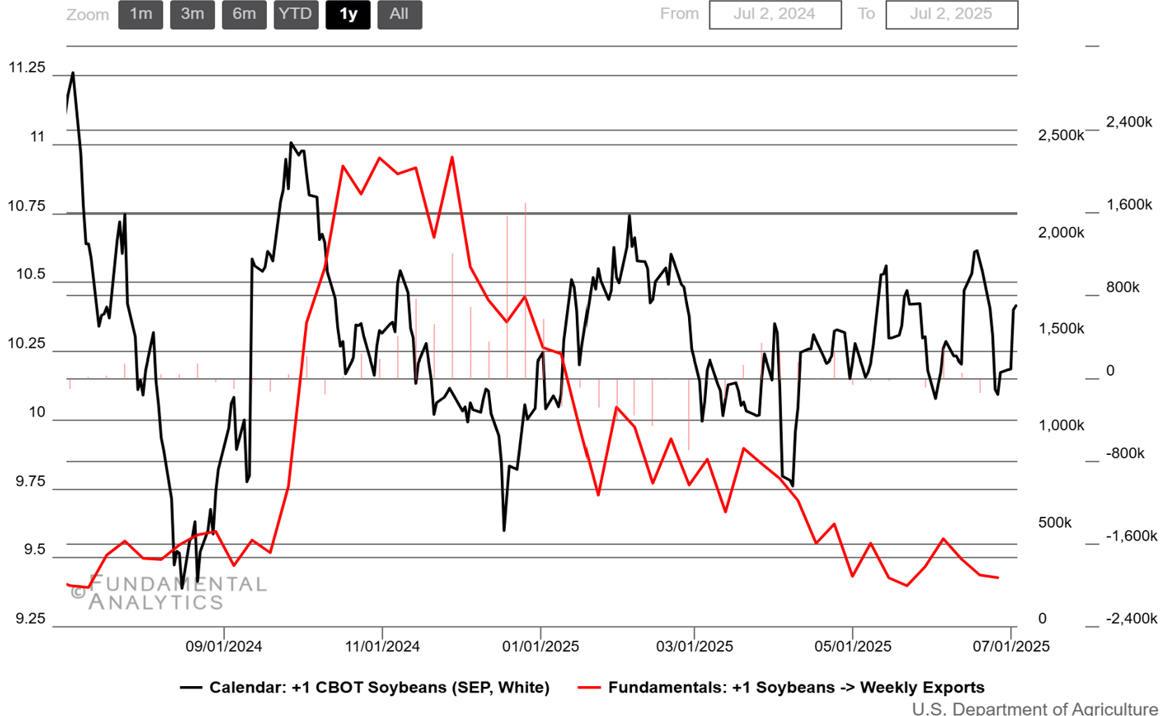

Soybeans |

|

Soybeans gained 2.2% w/w, supported by short covering and pre-holiday positioning |

|

|