Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s energy topics include:

- LNG: The Iran conflict has fractured global natural gas markets, creating simultaneous LNG shortages overseas and severe oversupply in the United States, where export bottlenecks are driving domestic prices to multi month lows despite soaring global demand.

- Crude Oil: The UAE’s decision to leave OPEC amid the Iran conflict signals growing fractures within the global oil alliance, reinforcing bullish crude oil sentiment as supply disruptions and uncertainty over future production coordination continue to tighten markets.

- Gasoline: Escalating Middle East conflict and refinery disruptions are driving a sharp surge in U.S. gasoline prices, tightening fuel supplies, and adding renewed inflationary pressure across the broader economy.

- Wild Card: The Iran conflict has created a widening disconnect between collapsing U.S. natural gas prices and soaring international LNG prices as export bottlenecks trap excess supply in West Texas while overseas markets face acute shortages.

Let’s begin.

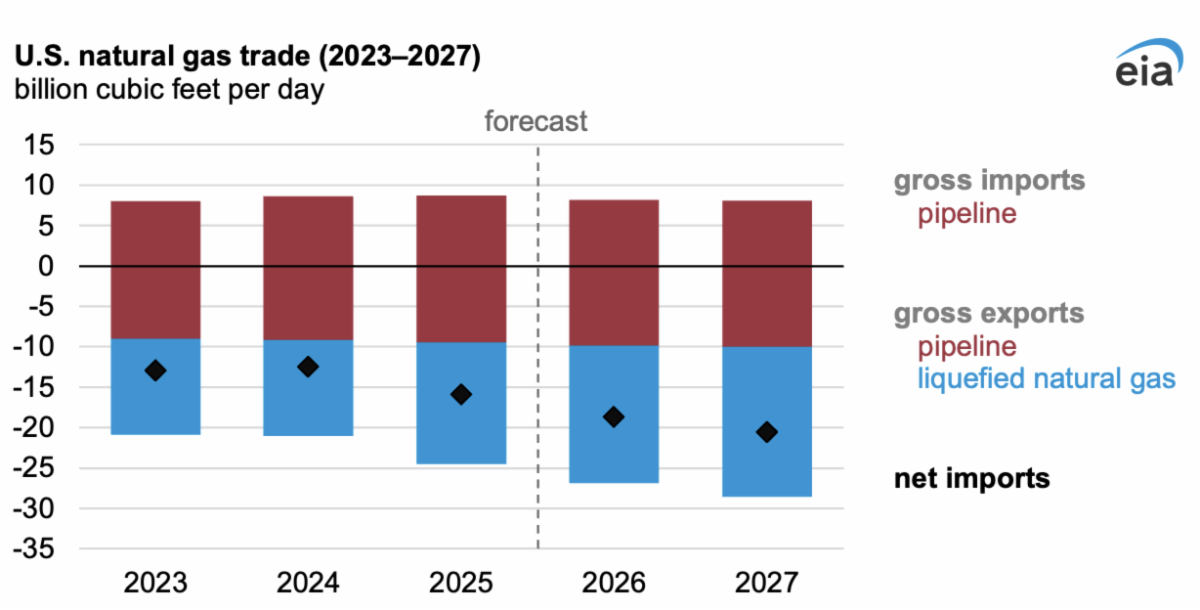

LNG

Source: U.S. Energy Information Administration, Short-Term Energy Outlook (STEO)

While Asia and Europe scramble for natural gas, the US glut has nowhere to go

Scott Disavino and Curtis Williams, Reuters

The war with Iran has sharply disrupted global natural gas markets by knocking out about 20% of liquefied natural gas (LNG) supply from the Gulf, sending prices soaring in Europe and Asia while leaving the United States awash in cheap gas. Iranian attacks and threats have damaged Qatari LNG facilities and blocked tanker traffic through the Strait of Hormuz, forcing import‑dependent regions to scramble for scarce supplies. In contrast, U.S. gas prices have fallen to 17‑month lows because domestic production is at record levels and export infrastructure—pipelines and LNG plants—is already full, preventing additional gas from reaching overseas buyers. This bottleneck is so severe in places like the Permian Basin that some producers must pay to have gas taken away. While LNG sellers with spare cargoes have benefited from the price dislocation, most U.S. gas producers are stuck selling at low domestic prices, prompting some to cut output until demand and export capacity grow later in the decade.

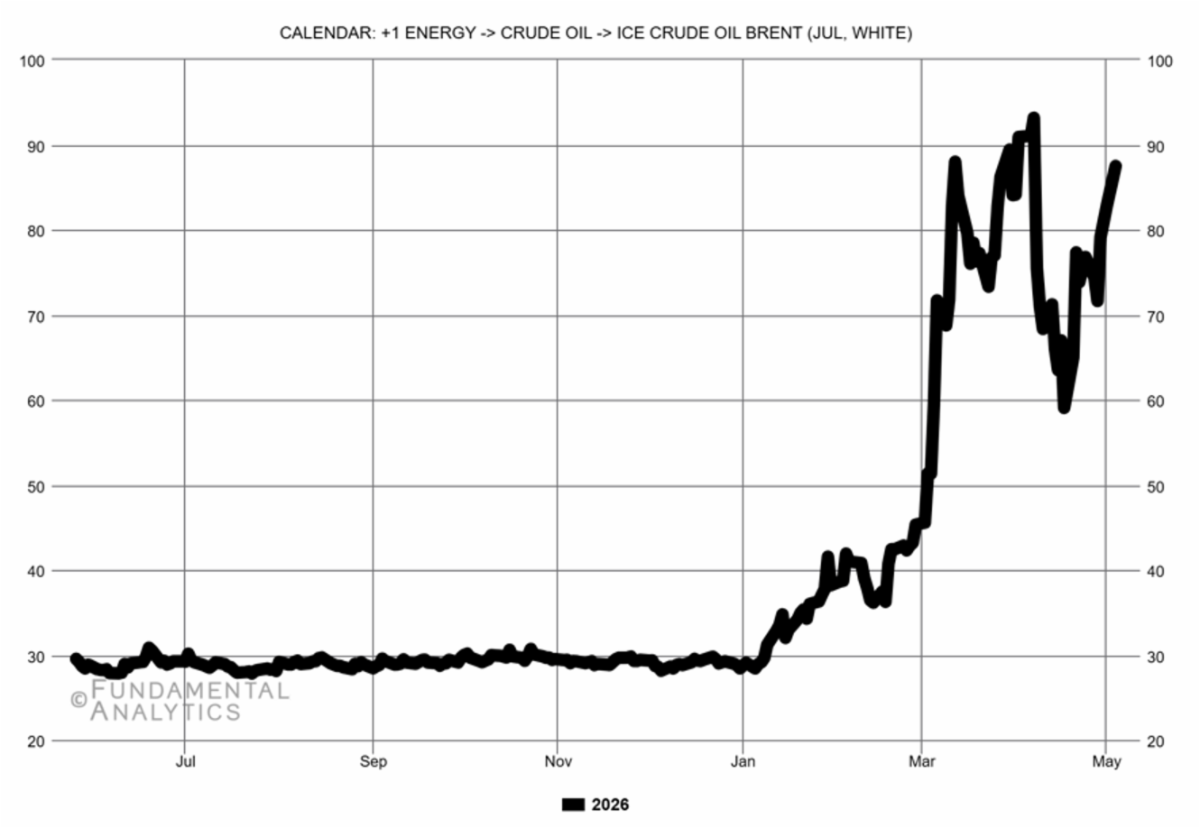

Crude Oil

Source: Fundamental Analytics

UAE Quits OPEC as War Upends Oil Markets and Gulf Tensions Rise

Sam Dagher, Grant Smith, Joumanna Bercetche, Bloomberg

The United Arab Emirates announced it will leave OPEC on May 1, marking a major shift in global crude oil markets amid ongoing supply disruptions tied to the Iran war and the near closure of the Strait of Hormuz. The UAE, previously OPEC’s third largest producer accounting for roughly 12% of group supply, argued that an undersupplied market requires greater production flexibility outside the group’s quota system, especially as the conflict has removed significant volumes from global markets and pushed oil futures near $111 per barrel. Analysts view the move as a long-term weakening of OPEC cohesion and Saudi Arabia’s ability to act as the market’s primary stabilizer, particularly because the UAE holds substantial spare production capacity and may eventually increase output independently. In the near term, however, the impact on supply is expected to remain limited as Persian Gulf exports continue to face severe disruptions, with some traders estimating that roughly one billion barrels of supply losses are now effectively locked into the market and could take years to fully replace. In the chart below, you can see the sharp increase following the Gulf conflict and additional spikes after the UAE’s withdrawal.

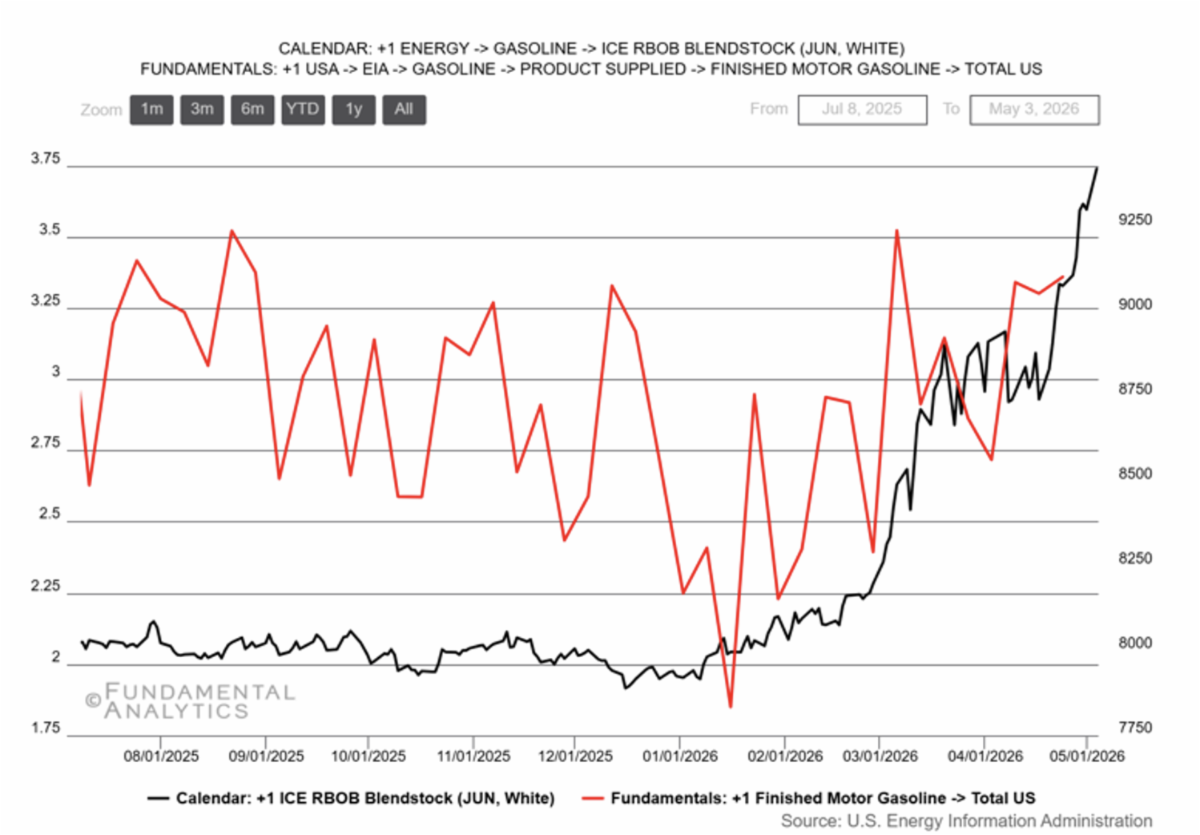

Gasoline

Source: Fundamental Analytics

U.S. Gasoline Prices Spike as Trump Tries to Calm Markets

Daniel Graeber, IIR News Intelligence

U.S. gasoline prices are surging toward $4 per gallon nationwide—and nearing $5 in parts of the Midwest and $6 in California—driven by refinery outages, elevated crude oil prices, and a geopolitical risk premium linked to the war in the Middle East. Recent disruptions at major Midwest refineries in Indiana and Illinois have tightened regional fuel supplies, while wholesale gasoline prices have nearly doubled in the past three months. At the same time, oil prices have climbed above $100 a barrel amid conflict-related shutdowns affecting more than 12 million barrels per day of global crude supply. The price spike is rippling through the broader economy, intensifying inflation pressures, according to the World Bank. Although the Trump administration is exploring deregulation to encourage more domestic drilling, U.S. producers remain cautious, with surveys showing limited confidence that higher prices will persist long enough to justify increased investment.

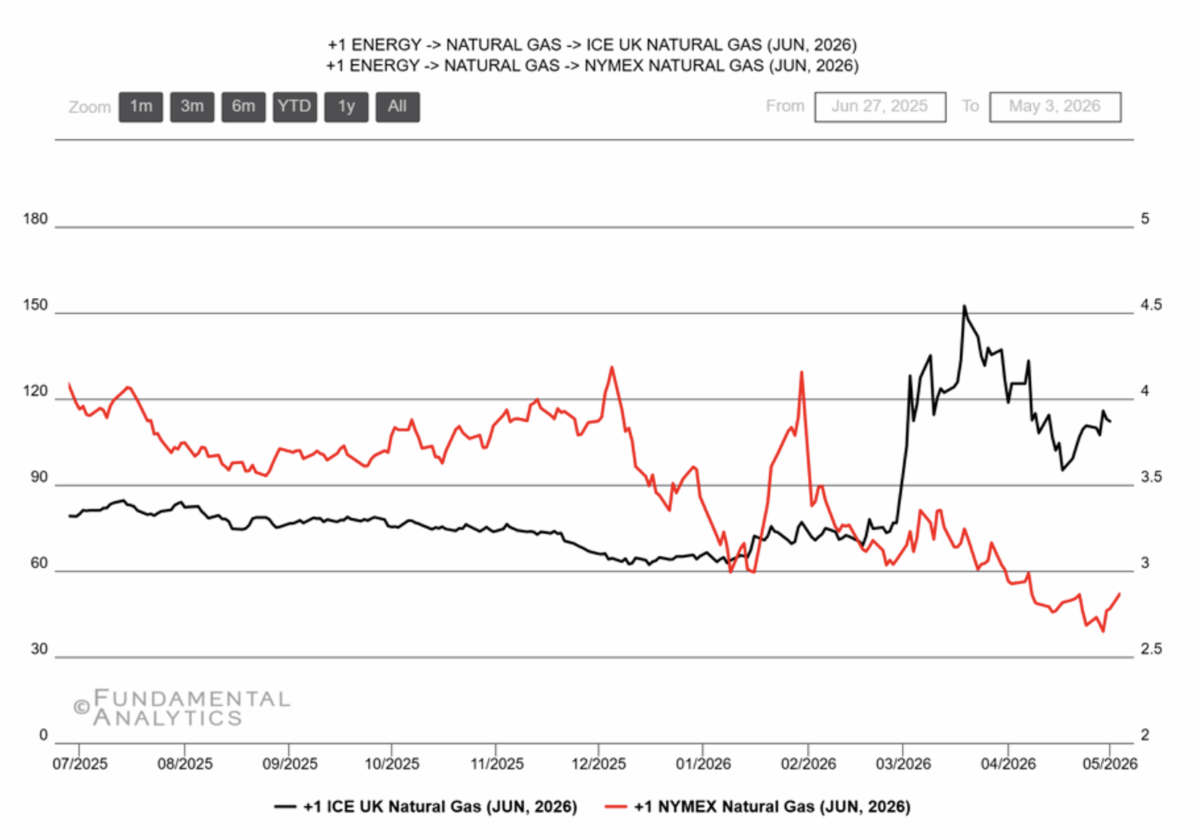

Wild Card

Source: Fundamental Analytics

Negative West Texas Gas Prices Reveal Mismatch in Global Energy

Bloomberg

A growing dislocation in global energy markets is highlighting major infrastructure bottlenecks as West Texas natural gas prices collapse into negative territory even while global LNG prices surge due to disruptions tied to the Iran war. In the Permian Basin, where oil and gas are produced together, strong crude prices near $100 per barrel are encouraging continued drilling, but insufficient pipeline capacity has left producers unable to move excess gas to export markets, pushing Waha hub prices as low as negative $9.75 per million British thermal units. As a result, producers are increasingly flaring excess gas rather than shutting in profitable oil production, with flaring activity reaching its highest seasonal levels in at least five years. Meanwhile, overseas gas markets are tightening sharply following attacks on major LNG infrastructure in Qatar, underscoring how logistical constraints and damaged supply chains can create simultaneous oversupply in one region and acute shortages in another. The sharp difference in values below beginning in February have one increased in their margins. This is supported by the demand dislocation highlighted in the Bloomberg article on West Texas natural gas.

Trading Implications

Trading implications across energy markets remain highly divergence driven, with geopolitical disruptions creating simultaneously bullish crude oil and international LNG conditions while depressing domestic US natural gas prices. Crude oil markets are likely to remain structurally supported as supply losses tied to the Iran conflict and the UAE’s withdrawal from OPEC reinforce expectations of tighter global supply and elevated volatility. At the same time, constrained US export infrastructure continues to pressure domestic gas markets, particularly in the Permian Basin, where oversupply and negative pricing conditions may persist despite soaring overseas LNG demand. Refining outages and higher transportation fuel costs also suggest continued upside risk for gasoline and diesel prices, sustaining inflationary pressure and potentially supporting refining margins. Widening regional spreads and infrastructure bottlenecks may create additional opportunities in basis and dislocation trades.