Fundamental Analytics Team

Starting this month, our Commodity News Roundup series will be published on a weekly basis. This is a curated newsletter featuring concise summaries of key developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s energy topics include:

- LNG: U.S. drilling activity ticks higher for the first time in three weeks, but rig counts remain well below last year’s levels even as LNG exports hit record highs.

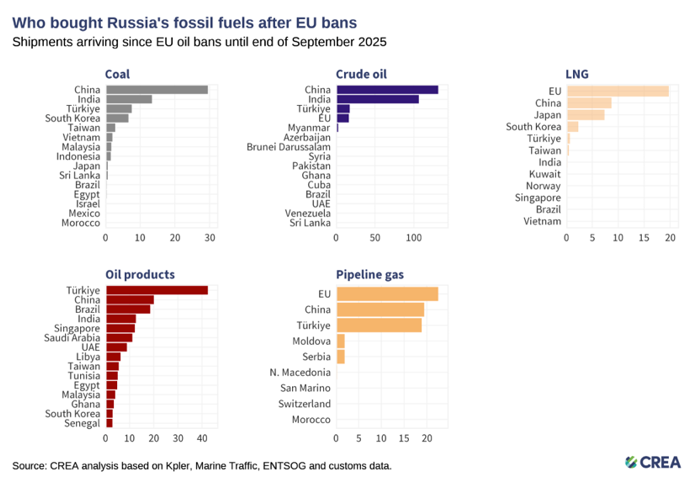

- Crude: Japan increases reliance on Russian crude as Middle East supply risks rise, highlighting the strategic premium on non‑Hormuz barrels.

- Gasoline: Russia expands its gasoline export ban through July amid infrastructure disruptions and rising global prices.

- Wild Card: Uranium Energy Corp. faces widening losses and accelerating dilution despite firmer uranium prices, keeping near‑term equity risk elevated.

Let’s begin.

LNG

Source: Fundamental Analytics

Source: Fundamental Analytics

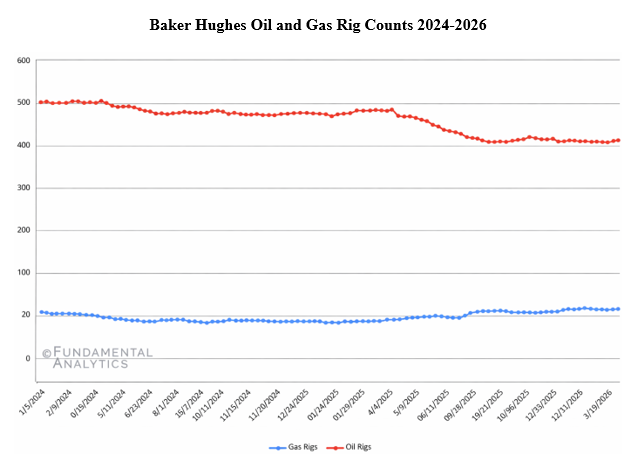

US drillers add oil and gas rigs for first time in three weeks, Baker Hughes says

Anmol Choubey, Reuters

U.S. energy firms increased drilling activity for the first time in three weeks, with the oil and gas rig count rising by five to 548 as of April 2, though it remains 42 rigs (7.1%) below year-ago levels, reflecting a multi-year trend of reduced drilling, including declines of about 7% in 2025, 5% in 2024, and 20% in 2023. Oil rigs rose by two to 411 and gas rigs by three to 130, as higher oil prices driven by Middle East supply disruptions begin to incentivize production growth. The Energy Information Administration projects U.S. crude output to average 13.61 million barrels per day in 2026 and 13.83 million in 2027, while natural gas production is expected to rise from a record 107.7 billion cubic feet per day in 2025 to 109.5 bcfpd in 2026, with Henry Hub prices forecast to increase about 7%. Meanwhile, LNG exports hit a record high in March as facilities operated above capacity, even as recent severe winter weather temporarily reduced domestic oil output earlier this year.

Crude Oil

Source: Fundamental Analytics

Source: Fundamental Analytics

Source: Ministry of Economy, Trade, and Industry

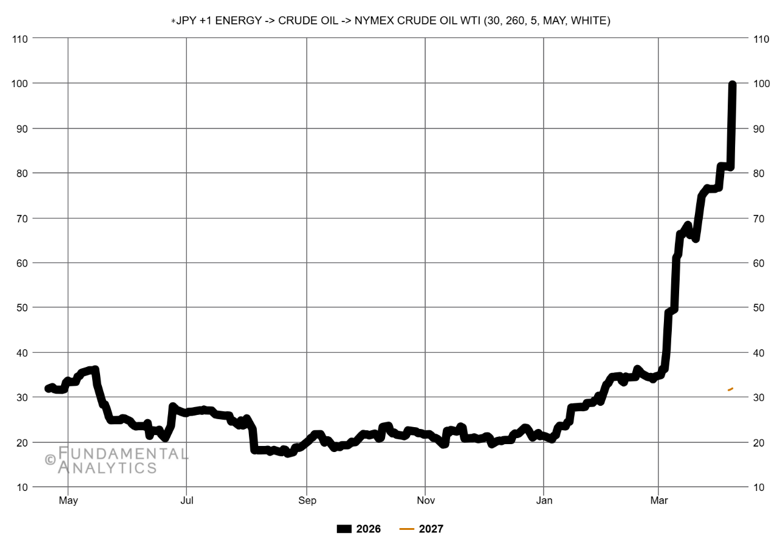

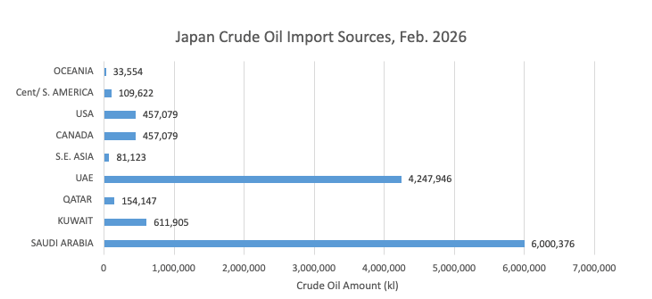

Japan sees Russian oil as ‘extremely important’ for energy security

Takeo Kumagai, S&P Global

Japan is signaling that Russian crude oil remains strategically important as Middle East supply risks rise, with 94% of its oil imports in 2025 coming from the region and 93% of that passing through the vulnerable Strait of Hormuz. Economy Minister Ryosei Akazawa emphasized the need to balance energy security with coordination among G7 partners and broader geopolitical considerations, particularly regarding Ukraine. Recent U.S. policy has temporarily allowed Russian oil transactions through April 11, while Japan has already resumed limited imports, including Sakhalin Blend crude tied to the Sakhalin-2 LNG project, which supplies about 10% of the country’s LNG. At the same time, Russia’s expanded gasoline export bans are tightening refined product availability globally, contributing to upward pressure on gasoline prices. Together, these moves highlight Japan’s pragmatic approach to securing stable energy supplies amid a market environment where geopolitical shocks are increasingly translating into sharp price swings.

Gasoline

Source: Fundamental Analytics

Source: Centre for Research on Energy and Clean Air

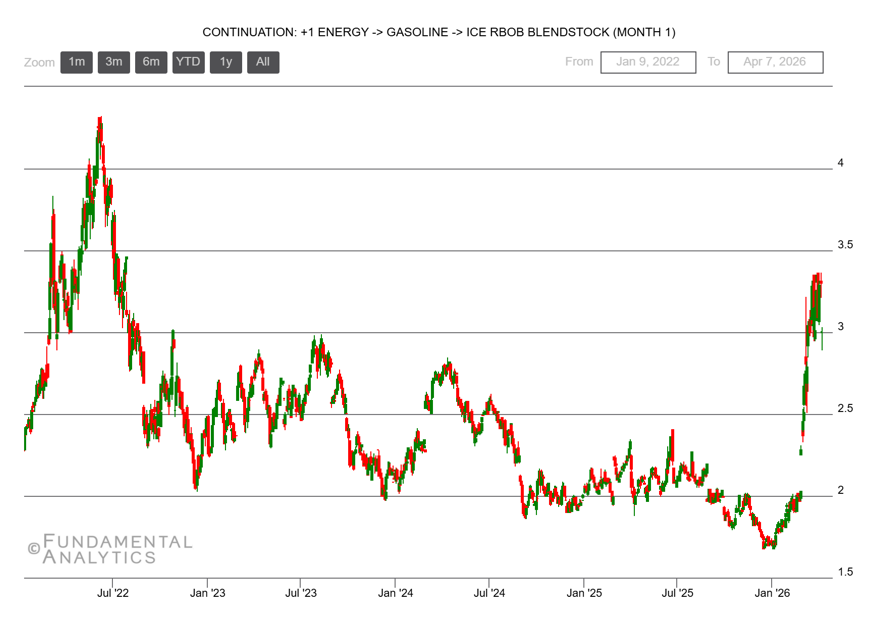

40% of Russia’s Baltic Oil Export Capacity Offline as Gasoline Ban Widens

Charles Kennedy, OilPrice.com

Russia has expanded its gasoline export ban to include producers through July 31 to stabilize domestic fuel supplies amid rising global oil prices and seasonal demand, while still allowing limited shipments under bilateral agreements such as with Mongolia. The move comes as the Middle East war drives higher prices and Ukrainian drone strikes disrupt Russia’s export infrastructure, with attacks on Baltic Sea ports forcing suspensions and knocking out as much as 40% of the country’s oil export capacity. Although Russian officials say domestic fuel reserves are sufficient and supply remains stable, these disruptions are limiting Russia’s ability to capitalize on higher oil prices and renewed demand from key buyers like India.

Wild Card

Source: Trading Economics

Commodity Prices Improve But Uranium Energy’s Dilution Problems Continue to Mount

Jason Ditz, Seeking Alpha

Uranium Energy Corp. continues to benefit from modestly improving uranium prices in FY2026 compared to 2025, but remains unprofitable with worsening operating losses and limited revenue growth due to low production volumes. The company’s biggest issue is persistent and accelerating share dilution, with outstanding shares rising from about 346 million in 2022 to over 490 million currently, as it relies heavily on equity issuance to fund operations and capital expenditures rather than generating positive cash flow. While this has created the appearance of a strong balance sheet, it masks underlying weaknesses, including ongoing negative cash flow and unclear timelines to profitability, which is not expected until around 2027 at the earliest. Despite valuable assets and long-term potential as a low-cost producer, the combination of weak execution, reliance on dilution, and lack of production scale makes the stock high risk in the near term.

Trading Implications

Tightening global supply signals and rising geopolitical risk continue to support a bullish bias across energy markets. U.S. drilling activity has ticked up but remains well below last year’s levels, keeping domestic supply growth constrained even as LNG exports run at record highs. Japan’s renewed reliance on Russian crude and Russia’s expanded gasoline export ban both reinforce upward pressure on refined products and non‑Middle‑East crude grades. Meanwhile, uranium equities remain high‑beta and volatile as companies like Uranium Energy Corp. struggle with losses and dilution despite firmer prices. Traders may find the best risk‑reward in maintaining a long bias in crude and gasoline spreads while favoring broad uranium ETFs over single‑name exposure until production fundamentals improve.