The Fundamental Analytics Team

The global energy transition, anchored in widespread electrification and rapid renewable deployment, is fundamentally reshaping two intertwined markets. Part I of this commentary examined how moving generation from fossil fuels to electricity (from EV adoption to hydropower storage) transforms cost structures, environmental footprints, and grid resilience. In today’s commentary, we focus on exploring how demand-side erosion, policy levers, and underinvestment on the supply side are creating a regime of lower average prices but with higher volatility for the crude oil market.

The energy transition is reshaping crude oil pricing through two countervailing dynamics: slowing demand growth on one side, and looming supply shortfalls on the other.

Electric vehicle (EV) adoption underscores the demand shift. Global EV sales climbed 25% in 2024 to over 17 million units, boosting market share above 20%, with another 35% surge in Q1 2025. Policy action continues to pressure fossil fuel consumption. The EU’s Carbon Border Adjustment Mechanism (CBAM), phasing into full implementation by 2035, adds structural cost to carbon-intensive imports. Average summer carbon permit prices of €70/t further weigh on industrial and aviation fuel margins. Hydrogen mandates and electrification targets compound the drag. Reflecting this, the IEA projects oil demand to plateau near 105 mb/d before 2030, with post-2027 growth slowing to just 0.4 mb/d. The EIA sees Brent averaging $68.90/barrel in 2025 and softening to $58 in 2026, citing inventory builds. OPEC maintains a more bullish long-term view, but its baseline shows contraction among OECD consumers.

Supply, however, tells a different story. Upstream investment remains subdued. Although 2024 capex rose 7% to $570 billion, it remains nearly 25% below the 2014 peak. Wood Mackenzie warns that if current spending trends persist, Brent could breach $100/barrel by the decade’s end, with a 30% uplift in capex needed to prevent deficits. Near-term, IEA commentary on tightening conditions helped fuel a 3% Brent rally this month alone.

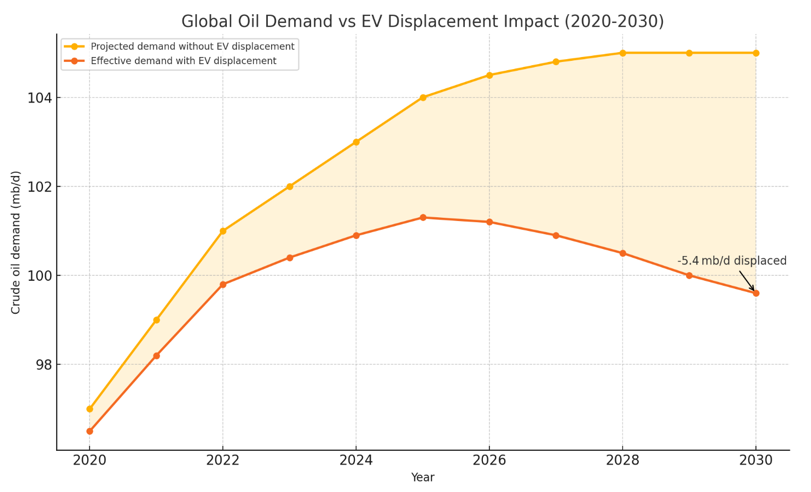

Renewables reinforce the shift. Wind and solar—already making up nearly all new global power capacity—are projected to provide over half of electricity generation by 2050 in most scenarios. As their share increases, oil-fired generation and even some natural gas demand are displaced. Transport is pivotal: EV penetration alone could displace 5–5.4 mb/d of crude demand by 2030 (Figure 1).

Figure 1. Crude Oil Displacement | Source: IEA & Bloomberg LP

Cost trends support this transition: from 2010 to 2019, onshore wind costs fell 38%, solar PV dropped 82%—and further declines continue. Coupled with cheaper batteries and permitting reforms such as REPowerEU, renewables erode oil’s competitive edge.

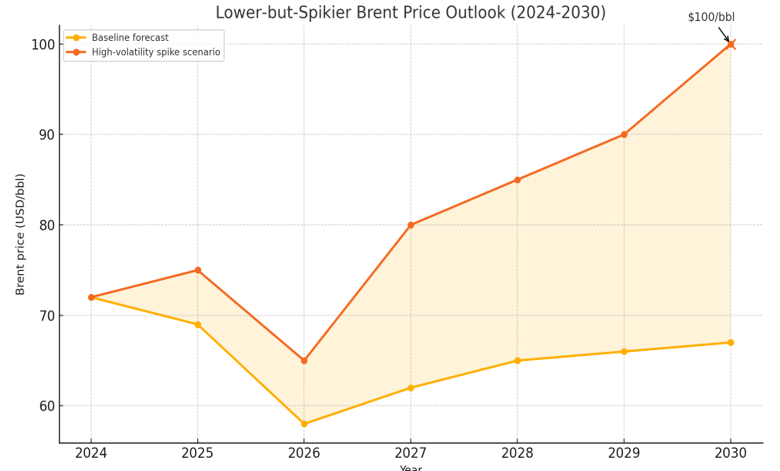

Taken together, a “lower but spikier” pricing regime emerges as the base case (Figure 2). Demand-side factors, electrification, and policy constraints point to Brent stabilizing in the $60–70/barrel range. But persistent underinvestment shortens supply elasticity, leaving prices vulnerable to geopolitical shocks and weather volatility. Risk managers should model both steady deceleration and spike scenarios—not assume a smooth glidepath.

Figure 2. Base-Case scenario | Source: IEA & Bloomberg LP