Grain futures held steady under pressure, facing a confluence of record U.S. corn acreage, abundant soybean and wheat yields, intensifying competition from Brazil, persistent Chinese import demand, and continued Black Sea export activity. Tariffs and GMO restrictions further reshaped global trade flows, adding friction to an already complex landscape.

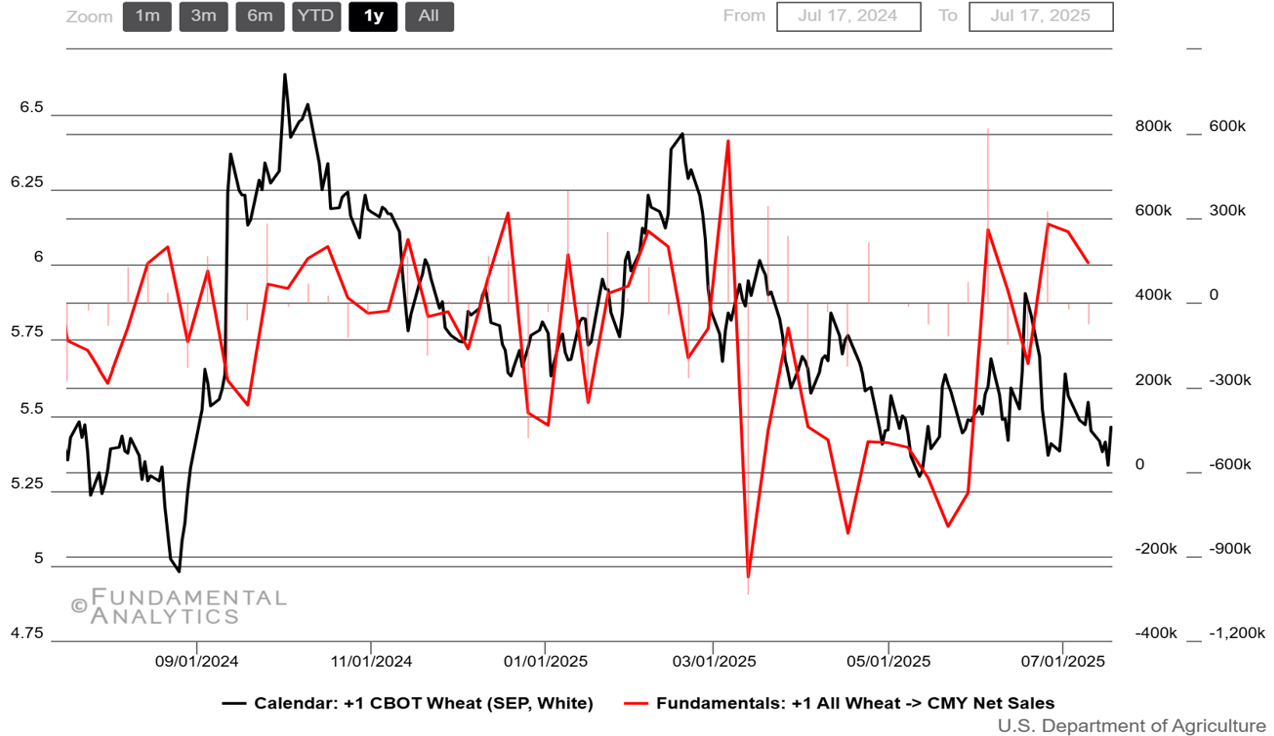

Wheat

Depleted sales and new Russian strategy pressures Sep contracts

- Early‑season export business stayed brisk yet price tension lingered. Net sales of 494 kt for the week to July 10 kept cumulative bookings ahead of the prior four‑week average, and USDA raised hard‑red winter export projections; nevertheless, buyers continued to compare U.S. offers with cheaper Black‑Sea quotes, tempering futures gains.

- USDA’s mid‑July updates reinforced a well‑supplied U.S. balance sheet.The July Crop Production cut winter‑wheat output 3 % from June but the Wheat Outlook nudged total production to 1.93 bn bushel and lifted 2025/26 export and ending‑stock forecasts

- Black‑Sea policy shifts leaned bearish.Moscow’s decision to drop the wheat export tax to 0% and instruct ministries to accelerate shipments signaled an aggressive marketing campaign just as Russian harvest delays briefly tightened nearby supply—adding fresh downward pressure to Chicago spreads.

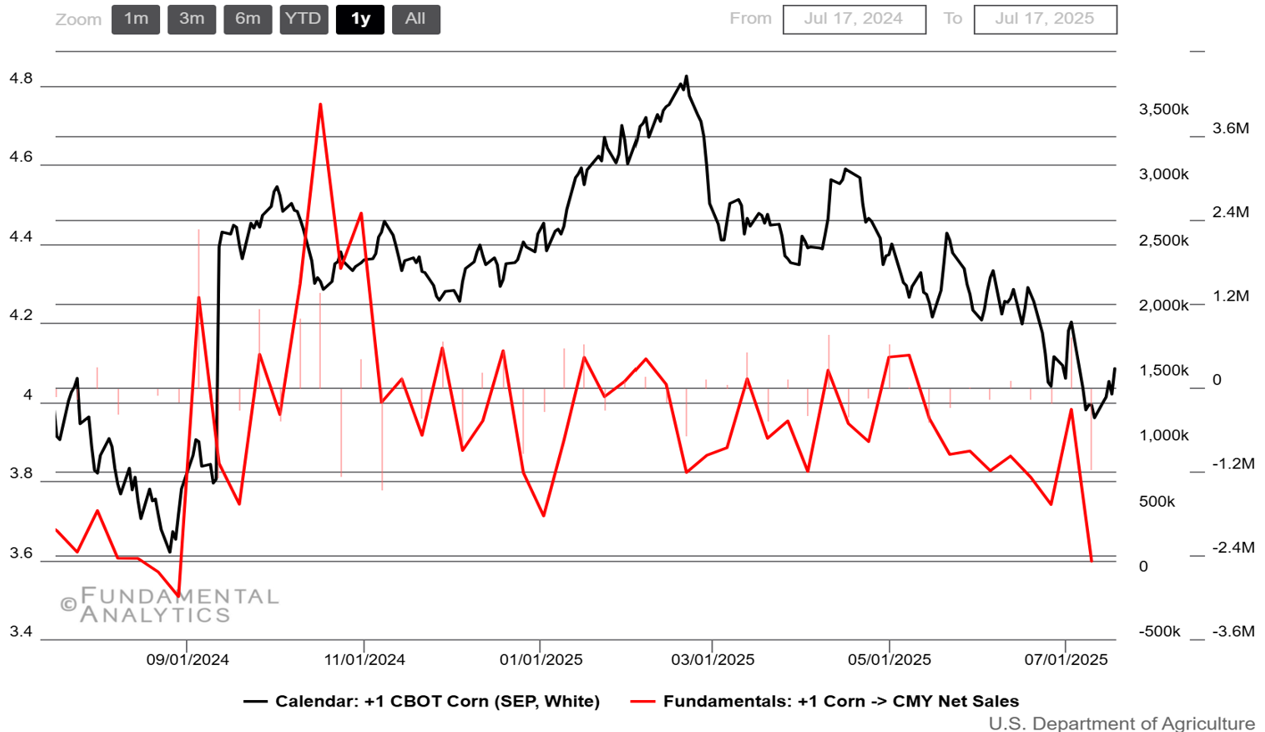

Corn

Diminished corn sales driven by strong harvests in Brazil and oversupply concerns

- Export momentum sagged as Brazil and others undercut U.S. offers. Net old‑crop sales collapsed to a marketing‑year‑low 97.6 kt, while Brazil’s near‑record safrinha harvest and cheaper FOB Santos values, coupled with China’s shift toward Brazilian and Ukrainian corn, diverted demand away from the Gulf.

- Ethanol metrics offered limited price support. Plant output hovered around 1.08 m bbl ⁄ day, but fuel‑ethanol stocks rose to 23.6 m bbl—the highest mid‑July level in four years—signaling ample domestic cover even as driving season peaks.

- Record acreage and top‑tier crop ratings sustain a heavy supply tone. USDA’s July WASDE trimmed 2025/26 U.S. corn ending stocks, yet 95.2 M planted acres (+5 % y/y) and a 74 % good/excellent rating keep talk of trend‑beating yields and hold CBOT futures near contract lows.

- Policy moves overseas reinforce a bearish narrative. The EU’s reinstated tariff‑rate quota caps duty‑free Ukrainian corn at just 650 kt for the rest of 2025, while Mexico’s constitutional ban on planting GM corn keeps trade friction with Washington alive—both shifts likely to reroute competitively priced grain and weigh on U.S. export prospects.

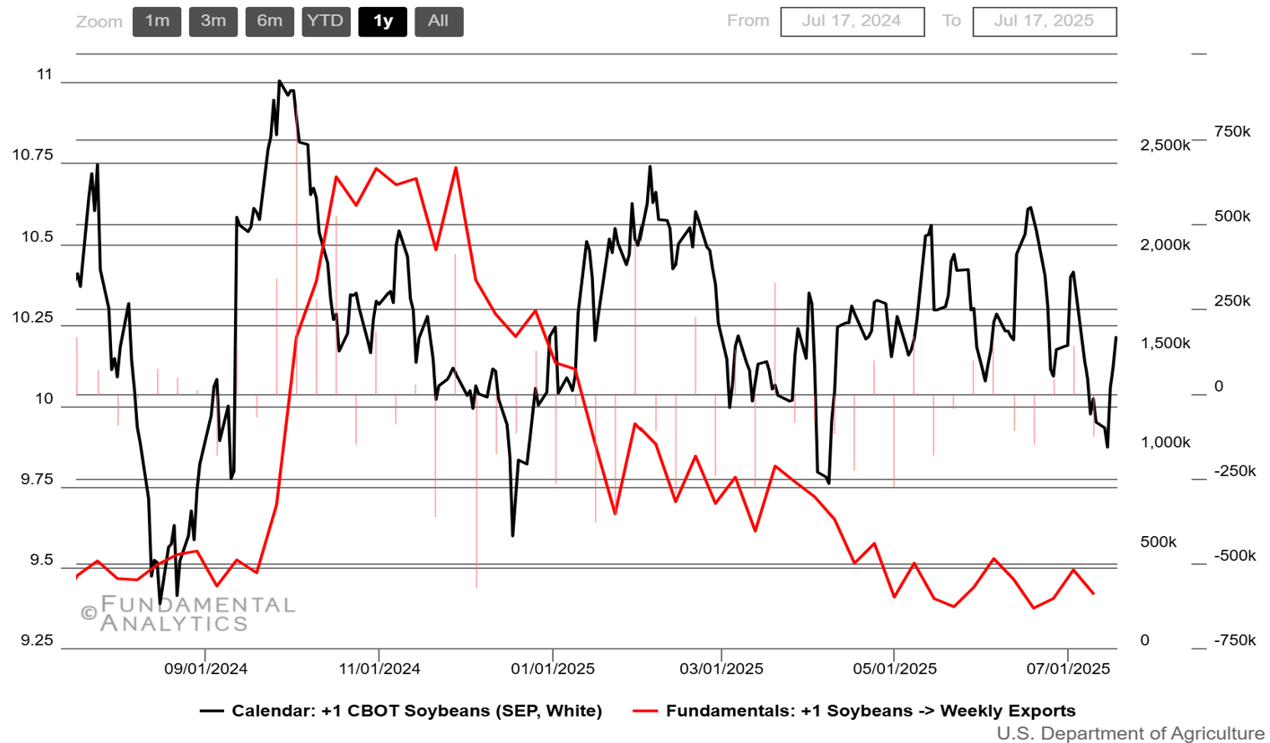

Soybeans

Mixed signals from exports and field conditions

- U.S. export pace cooled. The most recent FAS report showed light old-crop sales and dispersed new-crop business; with major Chinese buying scarce and cheaper Brazilian barrels competing, board rallies struggled to gain traction.

- Brazilian supply and loadings undercut U.S. values. CONAB reaffirmed a record ~197 MMT crop while exporter line-ups pointed to roughly 11–13 MMT of July shipments, reinforcing aggressive FOB offers that analysts say are chipping away at U.S. share and pressuring CBOT spreads.

- USDA’s July balance sheet turned modestly heavier, but fields remain broadly sound. The latest WASDE trimmed harvested area, held yield steady, lifted crush, pared exports and nudged 2025/26 U.S. soybean ending stocks to ~310million bushel; national Crop Progress kept condition near 70% good/excellent, muting weather premium.

- China’s diversification and feed-ration policies temper long-run import growth. Beijing’s push to lower soymeal inclusion rates, alongside new approval for Ethiopian soymeal imports, signals incremental demand shifts that cap bullish enthusiasm for U.S. beans.