WTI firmed on U.S. draws but OPEC+ adds capped gains; RBOB tightened despite soft demand and outages; natural gas pressured by inventories, strong output, weaker LNG intake, and minimal weather premium.

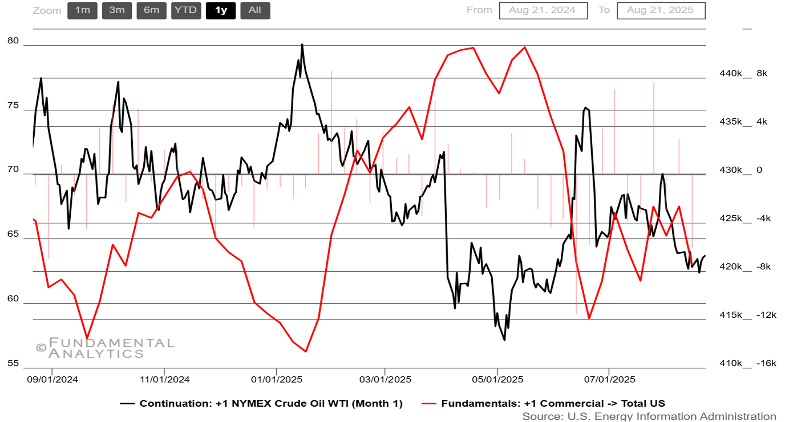

Crude Oil

Crude oil remains below $65 mark, Stockpiles weakened

- U.S. balances tightened, but gasoline demand lagged. The mid-month EIA report showed a 6 mb crude draw, stocks ~6% below the 5-yr norm, refinery runs at 96.6%, and gasoline stocks down 2.7 mb—factors that lend support to near-term WTI pricing, despite four-week gasoline supply figures trailing year-ago levels.

- Forthcoming OPEC+ barrels capped rallies. The alliance confirmed a ~547 kb/d production increase for September, reinforcing expectations of additional supply into late Q3 and curbing upside in futures despite tighter U.S. inventories.

- Shale signals stayed muted. Baker Hughes reported the U.S. rig count steady near 539 with ~412 oil rigs mid-period, slipping to 411 into the week’s end—insufficient to imply a rapid output surge.

- Geopolitics added a modest risk bid. Washington unveiled new Iran-related sanctions on shippers and tankers, while maritime advisories flagged electronic interference around the Red Sea/Hormuz corridors, keeping a security premium in focus.

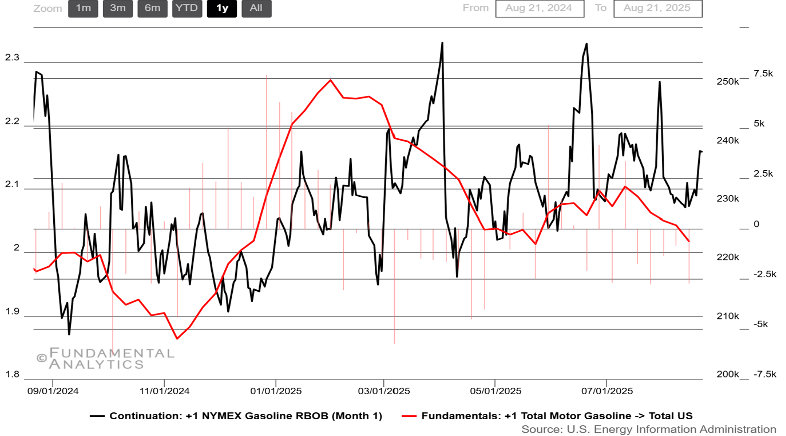

Gasoline

Futures soar on tightened inventories

- Inventories tightened, while demand fell short of last year’s levels. Consecutive weekly EIA reports showed U.S. gasoline stocks falling by ~3.5 mb in total, leaving inventories ~1% below the five-year norm, while the 4-week “product supplied” average hovered near 9.0 mb/d, ~1–1.5% y/y lower.

- High runs, but outages pinched regional supply. Refinery utilization held near 96–97%, yet a fire cut output at Phillips 66’s Bayway (NJ) and flooding disrupted BP’s Whiting (IN), lending support to NYH-linked RBOB differentials.

- Imports and blending flows cushioned the East Coast. Mid-month EIA data showed gasoline (and components) imports around 0.63–0.66 mb/d, helping offset outages and steadying overall supply despite firmer draws.

- Hurricane watch added headline risk, not a premium. With peak season approaching, forecasters and trade press flagged potential Gulf disruptions; AAA noted pump prices steady, limiting futures’ upside absent a landfall threat.

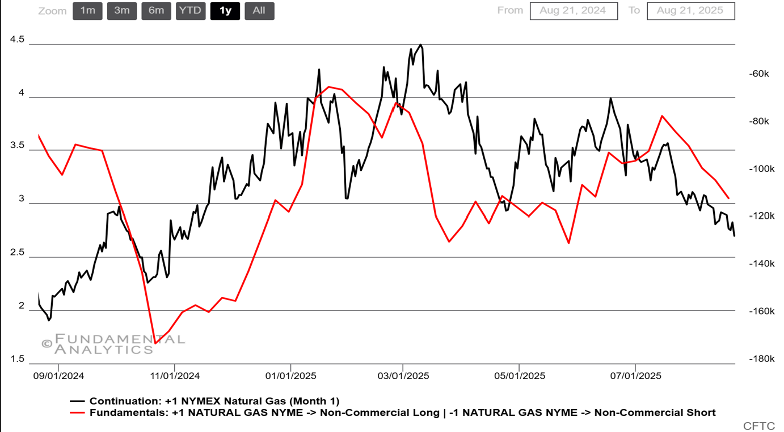

Natural Gas

Speculators’ funds send natural gas prices to 8-month low

- Inventories stayed above average despite a light build. The EIA reported a 13 Bcf injection and total stocks at 3,199 Bcf (~6% over the 5-yr norm)—supportive near term, but still a comfortable cushion for bears.

- Supply remained robust while LNG pull softened. Dry output averaged ~107 Bcf/d and gas-directed rigs held near 122, but LNG pipeline receipts dipped to 15.5 Bcf/d (-1.3 Bcf/d w/w) and pipeline exports to Mexico eased, loosening balances.

- Power burn firmed only marginally. Heat pockets lifted gas-for-power about 1% w/w, yet the overall demand uptick was modest versus supply and storage, muting follow-through in NYMEX rallies.

- Weather/geopolitics added headline risk, not a premium. NOAA kept an above-normal Atlantic season outlook, and Hurricane Erin churned offshore, reminding traders of Gulf disruption risk even as immediate impacts on U.S. gas flows were limited.