Brent stayed war-premium led as Hormuz constraints and low OPEC output outweighed emergency releases. RBOB tightened on inventory draws and export drains. Natgas softened on healthy injections and LNG maintenance.

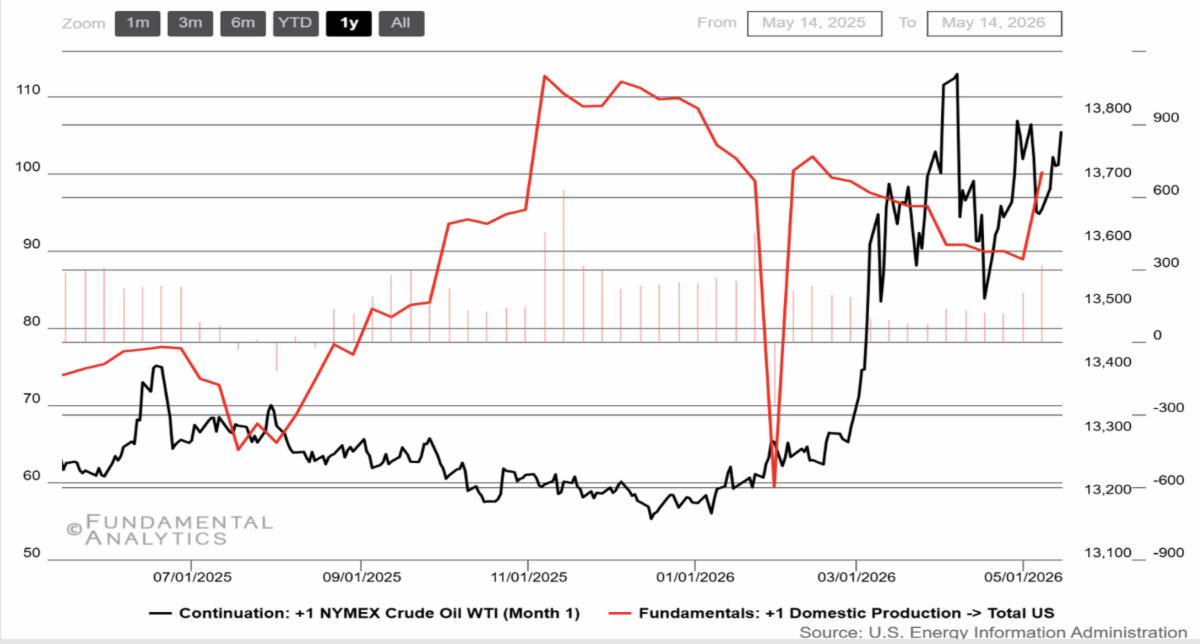

Crude Oil

US Drilling Companies Accumulate Crude Oil

Source: U.S. Energy Information Administration

- Hormuz constraint kept Brent structurally bid: With the Strait still largely shut/restricted and ceasefire language repeatedly downgraded, the front month carried a persistent “physical availability” premium.

- Supply-loss estimates moved higher, reinforcing backwardation: U.S. EIA and IEA assessments pointed to deeper-than-expected Middle East supply disruption (multi-million bpd), keeping prompt barrels scarce even when futures dipped on diplomacy headlines.

- OPEC barrels were missing in practice: A Reuters survey put OPEC output at a multi-decade low as export disruption hit members, tightening seaborne supply that benchmarks off Brent.

- Emergency stock releases acted as a circuit breaker, not a cure: The IEA’s coordinated 400mb release ramped (material volumes already flowing), damping runaway spikes but not fully offsetting the disruption narrative.

- Diplomacy + sanctions drove day-to-day reversals: Pauses in strike plans and talk of negotiations periodically deflated the risk bid, while new sanctions/ship targeting kept escalation risk alive—producing sharp two-way trade in the front month.

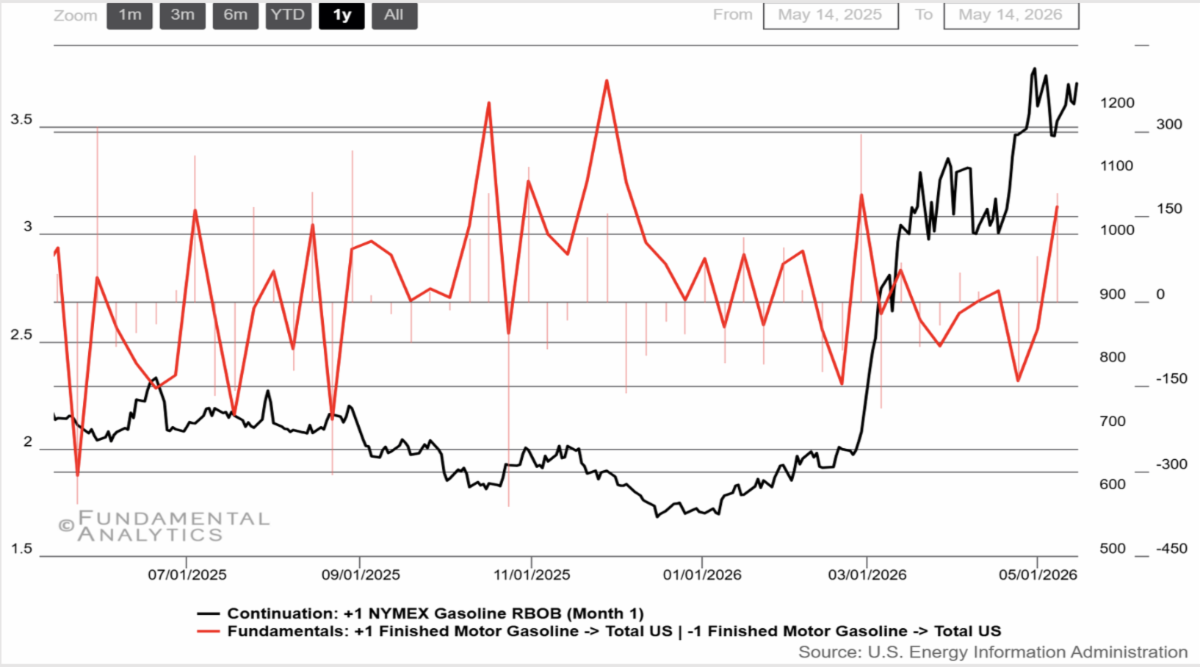

Gasoline

Net Gasoline Demand Hits 2 Month High As Prices Soar

Source: U.S. Energy Information Administration

- Inventory drawdown deepened into driving season: Total motor gasoline stocks fell ~4.1 mb and sat ~5% below the 5-year average; blending components tightened even as finished gasoline edged up.

- Exports drained the domestic pool: Gasoline exports jumped to about 1.05 mb/d as global buyers leaned on U.S. barrels amid war-disrupted trade flows, supporting the prompt RBOB bid.

- Demand didn’t fully validate the rally: Implied gasoline consumption was ~8.75 mb/d, and the 4-week product-supplied gauge for gasoline ran down ~0.8% y/y—price strength was more “availability premium” than demand boom.

- Refiners ran hard but couldn’t rebuild cushion fast: Utilization climbed to ~91.7% with gasoline output around ~9.8 mb/d, yet inventory draws persisted—keeping cracks supported but also raising “how long can runs hold?” risk.

- California boutique-blend stress became a headline driver: India’s LPG crunch cut alkylate output/exports (a key clean gasoline blendstock), tightening California’s additive supply and reviving talk of spec waivers as pump prices stayed above $6/gal.

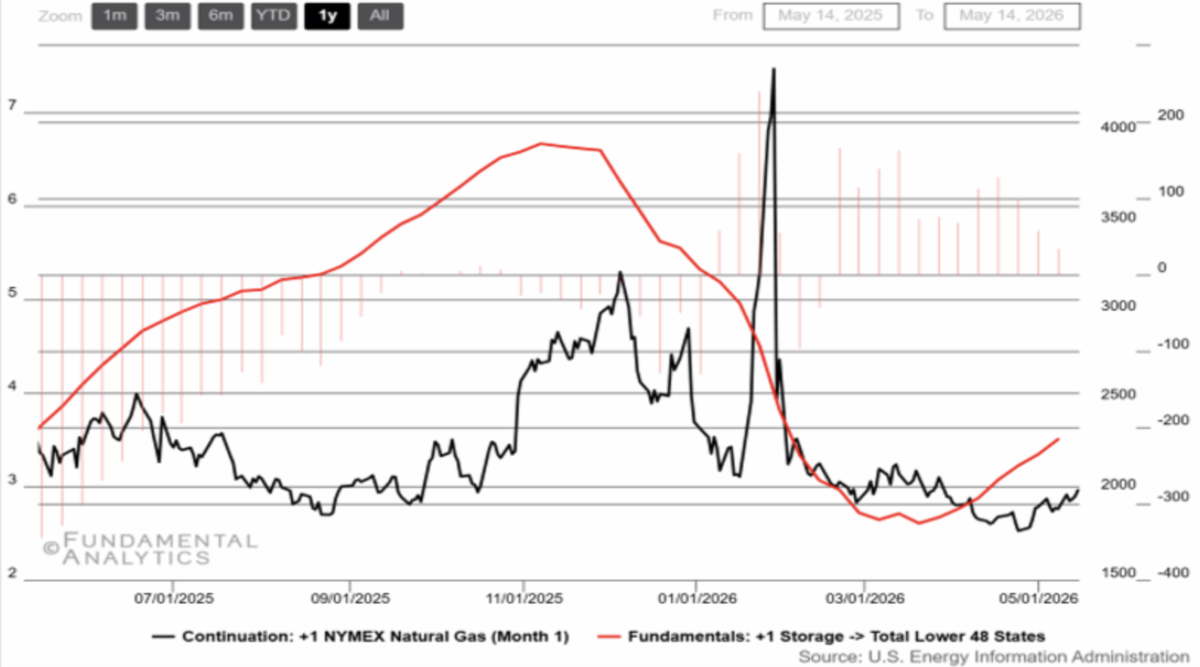

Natural Gas

Natural Gas Struggles To Surpass $3 Mark, Storage Strengthens

Source: U.S. Energy Information Administration

- Storage stayed “too comfortable” for bulls: A near-normal +85 Bcf injection lifted working gas to ~2,290 Bcf, keeping inventories well above the 5-year seasonal level and leaning the front month lower.

- Demand was shoulder-season soft, with only a late uplift from heat: Mild spring consumption kept injections healthy, while warmer forecasts only modestly improved the power-burn outlook.

- The supply ceiling was reinforced by the STEO: EIA projected record U.S. production in 2026 (and higher again in 2027) even as 2026 consumption dips, anchoring expectations of a persistently loose domestic balance.

- LNG demand temporarily eased on maintenance—bearish for prompt: Feedgas to major U.S. LNG plants slid to a 16-week low as facilities (including Golden Pass/Freeport) ran maintenance or outages, removing a key marginal bid.

- Geopolitics supported global LNG prices, but only indirectly lifted Henry Hub: Middle East disruption kept Europe/Asia LNG prices elevated, and a handful of U.S. cargoes headed to China, yet the U.S. market remained largely supply-led in the near term.