Commodity News Update

June 13, 2018

The goal of this report is to provide our readers with some important fundamental and technical trends in commodity markets this week.

Energy Market Update:

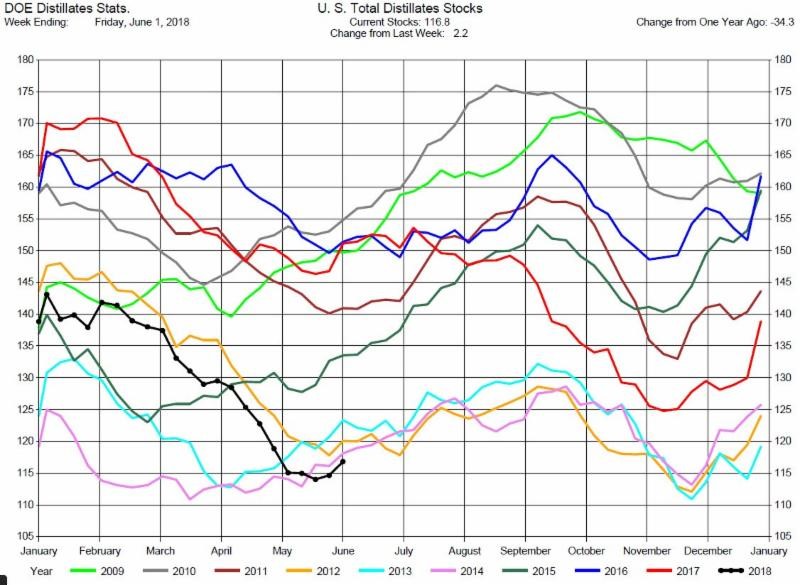

Total Distillate Stocks at record lows

Despite high production rates and reduced Demand, Total Distillate Stocks remain at record lows for this time of year as demonstrated in the chart below, where the black line represents 2018.

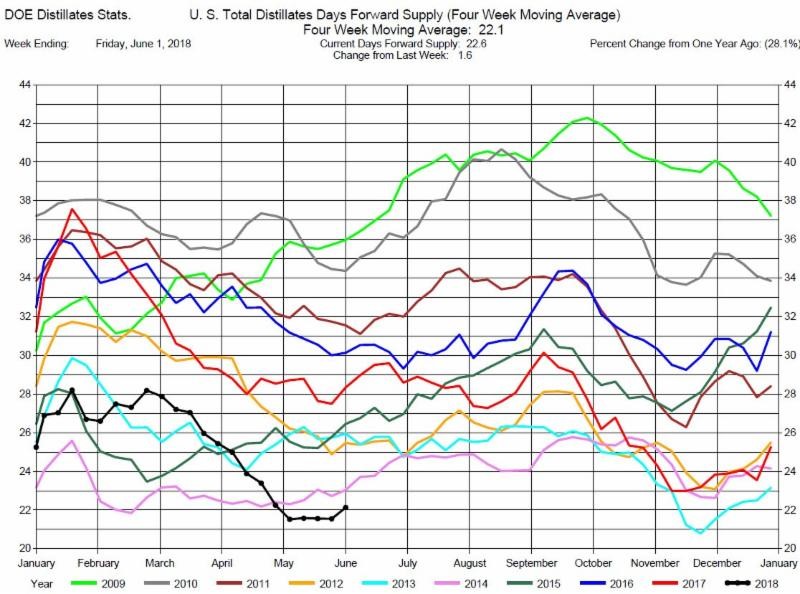

The ratio of the Demand to Stocks to the Days Forward Supply, a measure that adjusts for Stocks and Demand, is also at historic lows as shown in the chart below where the black line represents 2018.

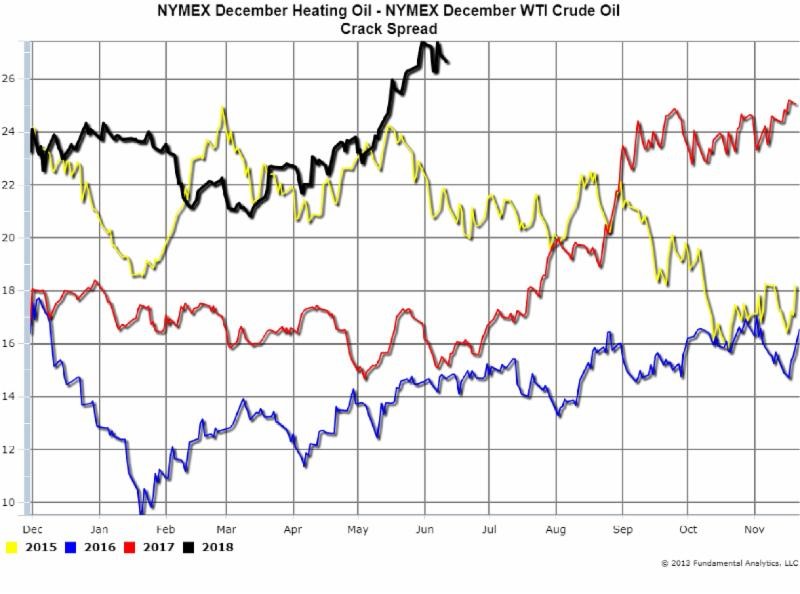

As a result, Heating Oil prices have dropped less than Crude Oil prices have dropped since May 29. Therefore the refiner’s margin – i.e. the Crack Spread, which is the difference between the raw material cost, Crude Oil, and the finished product price, Heating Oil – has widened. This is clearly illustrated in the December Heating Oil Crack Spread chart below, where the black line represents 2018. This is valuable to refiners’ margins and if this situation continues traders may consider going long the December or January Crack Spread.

Agriculture Market Update: USDA World Agricultural Supply and Demand Report

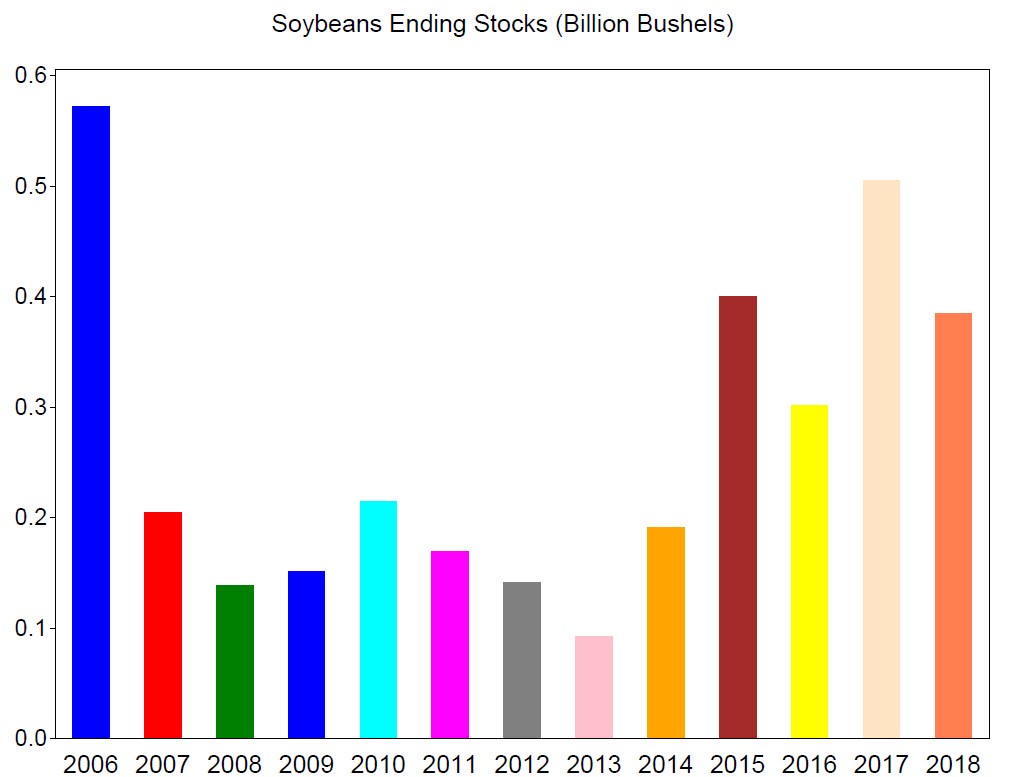

Soybeans:

The June USDA WASDE Report today indicated that US Soybean supplies will likely fall in the upcoming marketing year due to high domestic demand and strong exports. The value of the July futures contract for Soybeans jumped by 5 cents per bushel after the report was released but fell back during the trading day. We will need to view the longer term implications on price. However, if Ending Stocks estimates continue to reduce a trader may consider going long November Soybeans and a producer may consider putting on a hedge.

The USDA estimated Soybeans ending stocks for 2017/18 at 505 million bushels, far below Reuters analysts’ estimate of 522 million bushels. The USDA estimate for 2018/19 was 385 million bushels, also far below analysts’ estimate for of 417 million bushels. The chart below shows Soybean Ending Stocks back to 2006/07.

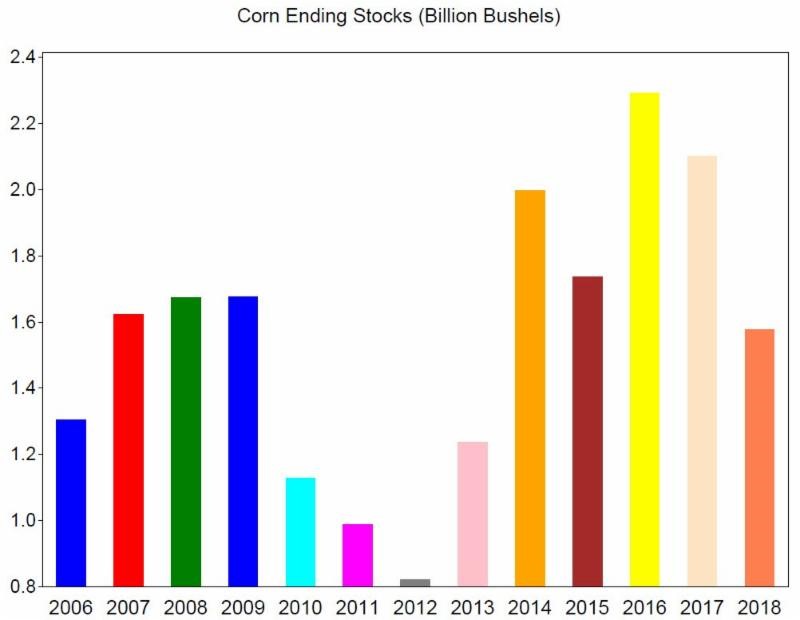

Corn:

Corn futures also jumped after the report was released since the June numbers were below Reuters analysts’ estimates. The July Corn futures contract jumped by 4 cents per bushel. Corn continued to rally throughout the trading day. We will watch to see if this rally is sustained. Should the Ending Stocks projections continue to decline a trader may consider going long outrights or bull spreads and producers may consider hedging their production.

Ending stocks of Corn at 2.102 billion bushels for 2017/18 were below Reuters analysts estimates of 2.166 billion bushels, and 1.577 billion bushels for 2018/19 were below analysts estimates of 1.663 billion bushels. The chart below shows Corn Ending Stocks back to 2006/07.

Wheat:

The July Wheat contract jumped from by 9 cents per bushel after the report was released, even though the June numbers were in line with Reuters analysts’ estimates. Wheat rallied even stronger than Corn throughout the trading day. If Wheat continues to outperform Corn a producer may consider a Wheat to Corn hedge play to protect production.

Ending stocks of Wheat at 1.080 billion bushels for 2017/18 were in line with Reuters analysts’ estimates of 1.079. For 2018/19, ending stocks at .946 billion bushels were slightly below estimates of .958 billion bushels. The chart below shows Wheat ending stocks back to 2006/07.