|

CBOT grains sagged as ample U.S. crops, record Brazilian output, limited Chinese demand, and trade restrictions outweighed brief weather hiccups and occasional export spikes, suppressing wheat, corn, and soybean futures. |

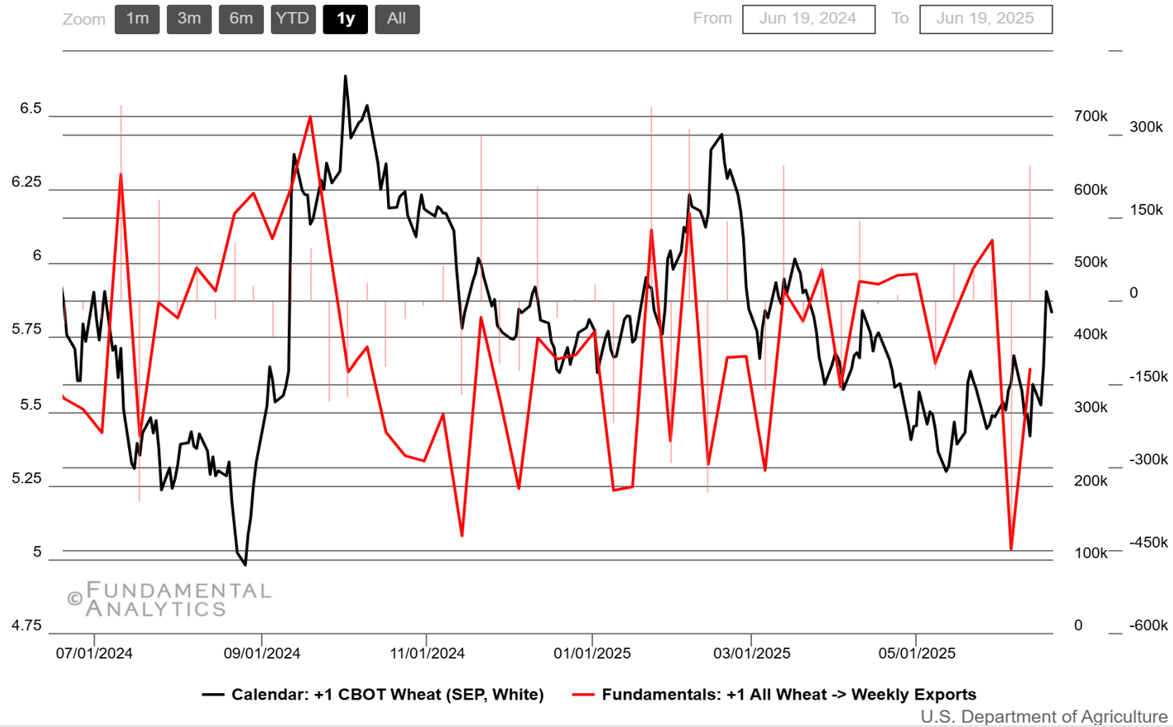

Wheat |

|

September futures settle just below $590 mark |

|

|

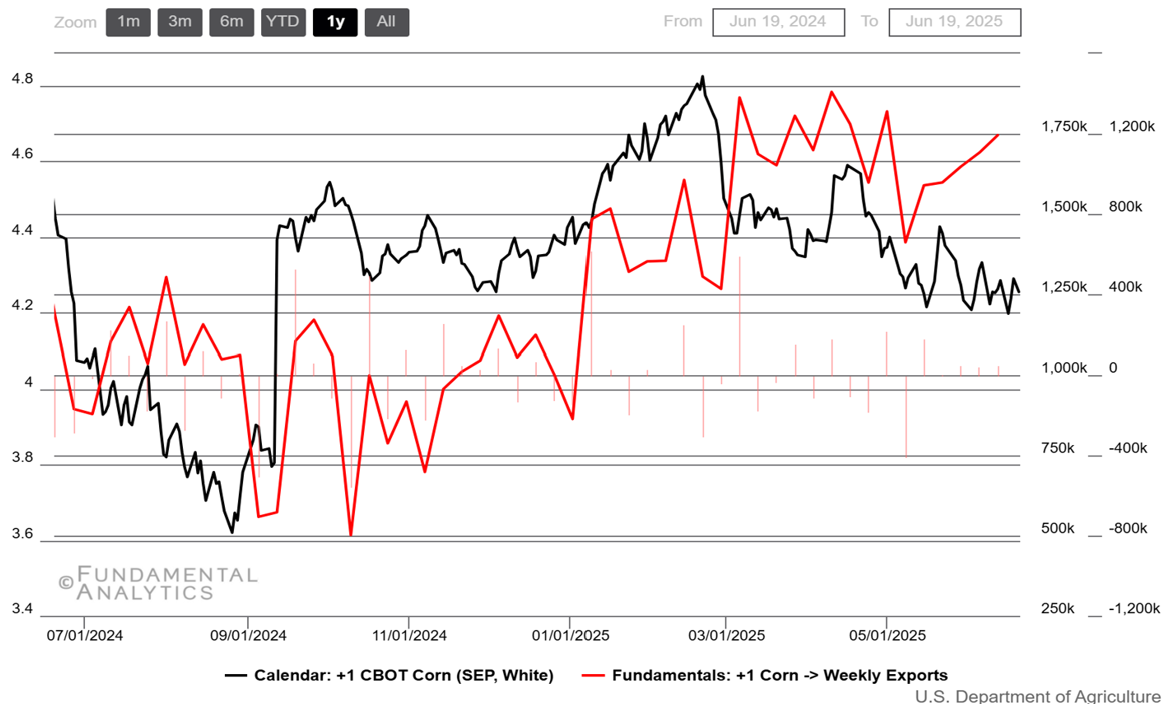

Corn |

|

Corn prices struggle to find a pattern despite increased exports |

|

|

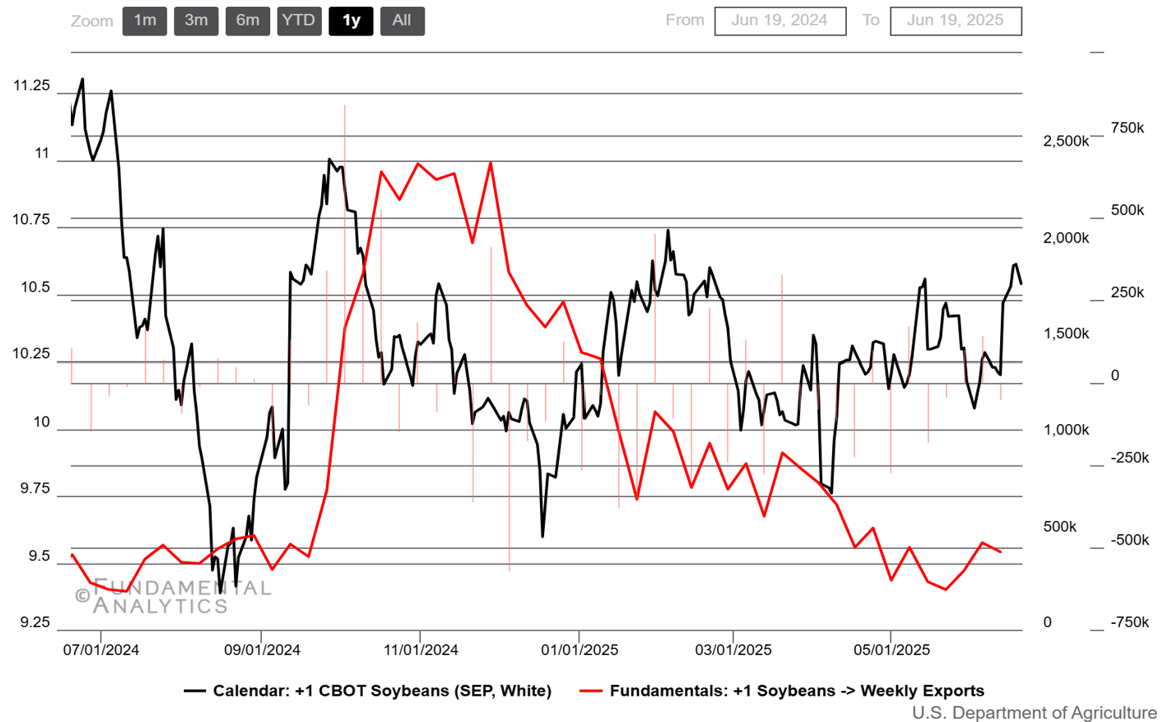

Soybeans |

|

Soybean futures reach $10.5 |

|

|