Dr. Ken Rietz

Twice a month, we’ll be sharing a new curated newsletter featuring concise summaries of key articles in the agriculture and energy commodities markets—along with direct links to the full pieces— as well as related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest developments and hopefully spark your interest to dive deeper into the full articles.

This week, we take a look at the latest developments in the major agricultural markets.

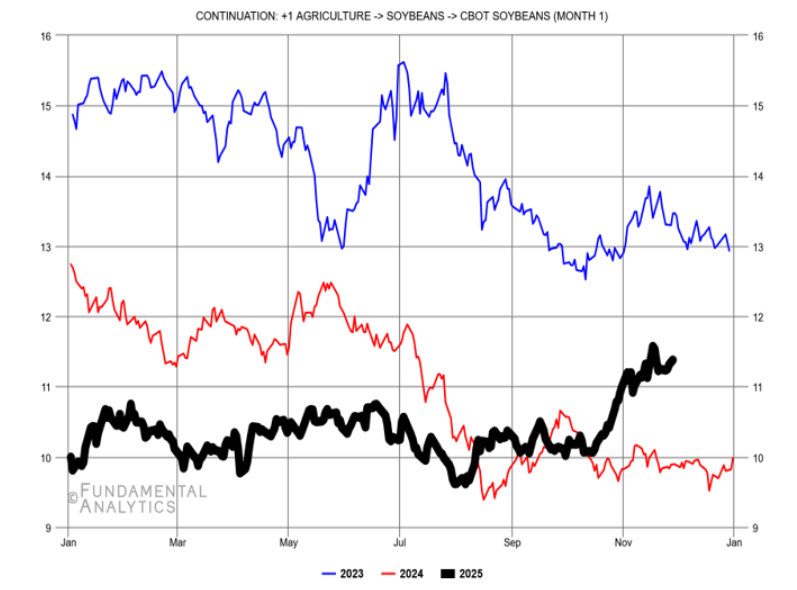

Soybeans

Figure 1: Front-month futures of CBOT soybeans

USDA Confirms More Soybean Exports to China and First Wheat Sale

By Michael Hirtzer and Erin Ailworth, Bloomberg

The USDA records show that China has ordered 462,000 tons of soybeans, bringing the total ordered since October 30 to 1.8 million tons. This is working on the 12 million tons they promised earlier this year. China has ordered 132,000 tons of white wheat, the first time they have ever bought it. China also committed to purchase 87,000,000 tons of soybeans over the next several years. However, as the US dollar gets stronger, there is a chance that this will be renegotiated, according to Hightower Report.

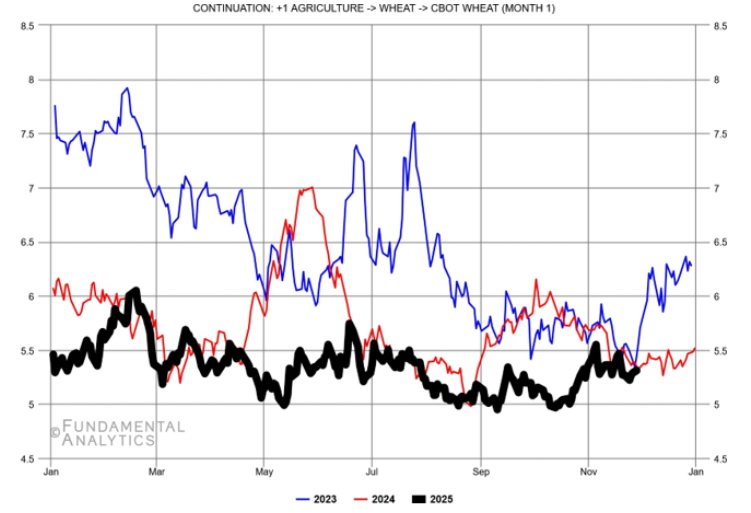

Wheat

Figure 2: Front-month futures for CBOT wheat

The price of wheat can’t seem to go up. That, of course, is a problem for farmers since it is a direct cut in their incomes. But the price might not continue its stagnation. The following article gives five different reasons for the price to start going up.

The 5 Fundamentals That Could Still Rally Wheat Prices

Tyne Morgan, AgWeb

The five factors are:

- Whether it rains in Argentina so farmers can plant their winter wheat crop.

- Whether El Niño reduces the Australian crop.

- Whether the weather stays dry in the U.S. spring wheat belt.

- How dry Russia’s spring wheat belt stays.

- Weather for Canada’s spring wheat belt.

Note that all of them are weather-related. The global weather will be changing due to the development of La Niña in the Pacific. Some of these might happen in that case. The last article in this commentary provides some additional insights.

Corn

Figure 3: Front-month futures for CBOT corn

Thailand opens door to U.S. corn under its zero-tariff pledge

FarmProgress, Bloomberg

Due to trade negotiations, Thailand will increase its import limit of US corn from 54,700 tons to one million tons. It will also cut its import levy from 20% to 0. All of this is to be able to import more US corn. The cut in tariffs on corn will make US corn competitive with corn grown in neighboring countries. All this was done in conjunction with US tariff reductions on Thai imports. And the US imports will be timed carefully to avoid competition with Thai corn farmers.

The biggest single factor that holds for all agriculture is the weather, and the single most important factor of the weather is the alternation between El Niño and La Niña, combined into El Niño Southern Oscillation (ENSO). The El Niño was in place from May 2023 to June 2024; since then, the weather has been neutral, until recently. Now we see La Niña taking form. That implies cooler and wetter weather in the north of the US, and warmer and drier weather in the south of the US.

Weather

La Niña emerges raising drought risks for California and Brazil

Farm Progress, Bloomberg

During the past few months, La Niña has been forming in the Pacific Ocean, and its effects will be felt in the Americas and, to a lesser degree, Europe. The effects on California and southern Brazil, and Argentina will make droughts more likely, with obvious consequences for these primary agricultural regions.

La Niña is significantly more likely than El Niño since 1980, with neutral periods between. The current La Niña is expected to be fairly weak, so the effects will likely be less dramatic than usual. The degree that ENSO affects long-term global weather patterns is complex and is actively being studied now.

Trading Implications

The La Niña will make predictions difficult, since the effect on crops will not be clear for a while. For soybeans, the market expects more orders from China, but it does look like a stretch for them to complete their order for 12 million tons of soybeans. In that case, soybean futures will drop some. For wheat, it is possible that at least one of the factors will actually happen, and the price of wheat would climb slowly. For corn, the total Thai trade is not likely to move the needle very much, at least this year.