Brent eased as peace hopes offset Hormuz risk; gasoline softened on inventory builds despite tight stocks; natural gas stayed capped by storage surplus and LNG maintenance, with heat limiting downside.

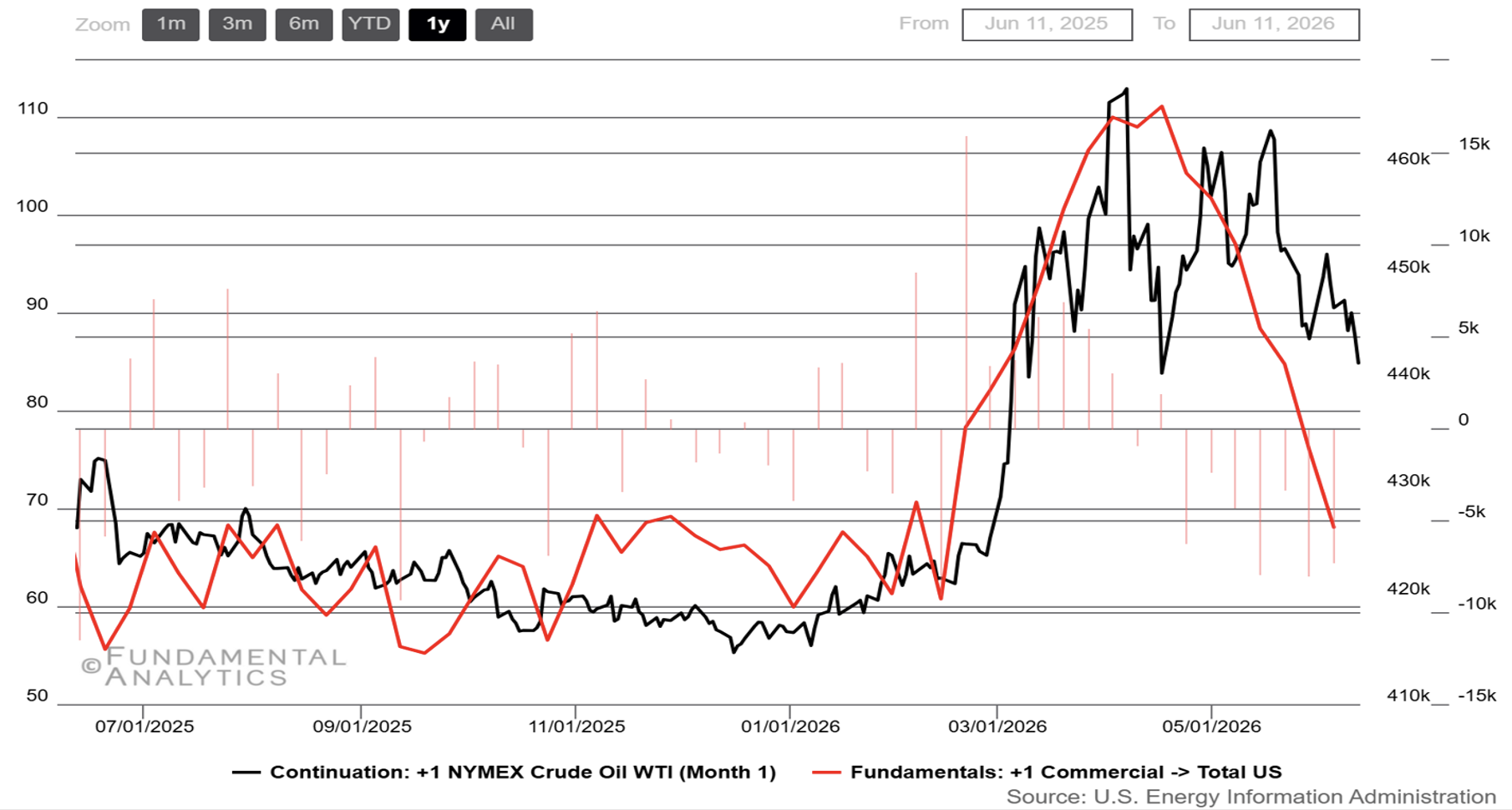

Crude Oil

Peace talks send Crude Oil Prices to month low, below $85 mark

- Peace-deal optimism deflated the war premium: Brent slid to its lowest level since early March as traders priced rising confidence that a U.S.–Iran memorandum could reopen Hormuz and normalize Gulf exports.

- Hormuz risk did not disappear: traffic through the Strait remained highly restricted, keeping a residual supply-risk premium in the curve despite headlines pointing toward diplomacy and de-escalation.

- U.S. inventory draws reinforced physical tightness: a sharp crude stock decline and very high refinery utilization signaled that Atlantic Basin barrels were still being pulled hard to offset disrupted Middle East flows.

- Demand destruction capped the upside: elevated prices, weaker China and Western Europe consumption, and OPEC’s lower 2026 demand-growth forecast limited how aggressively traders chased supply-risk rallies.

- Non-Gulf supply helped absorb the shock, but only partially: stronger output from the Americas and other non-Middle East producers softened the deficit narrative, yet OPEC+ output remained constrained by the effective Hormuz disruption.

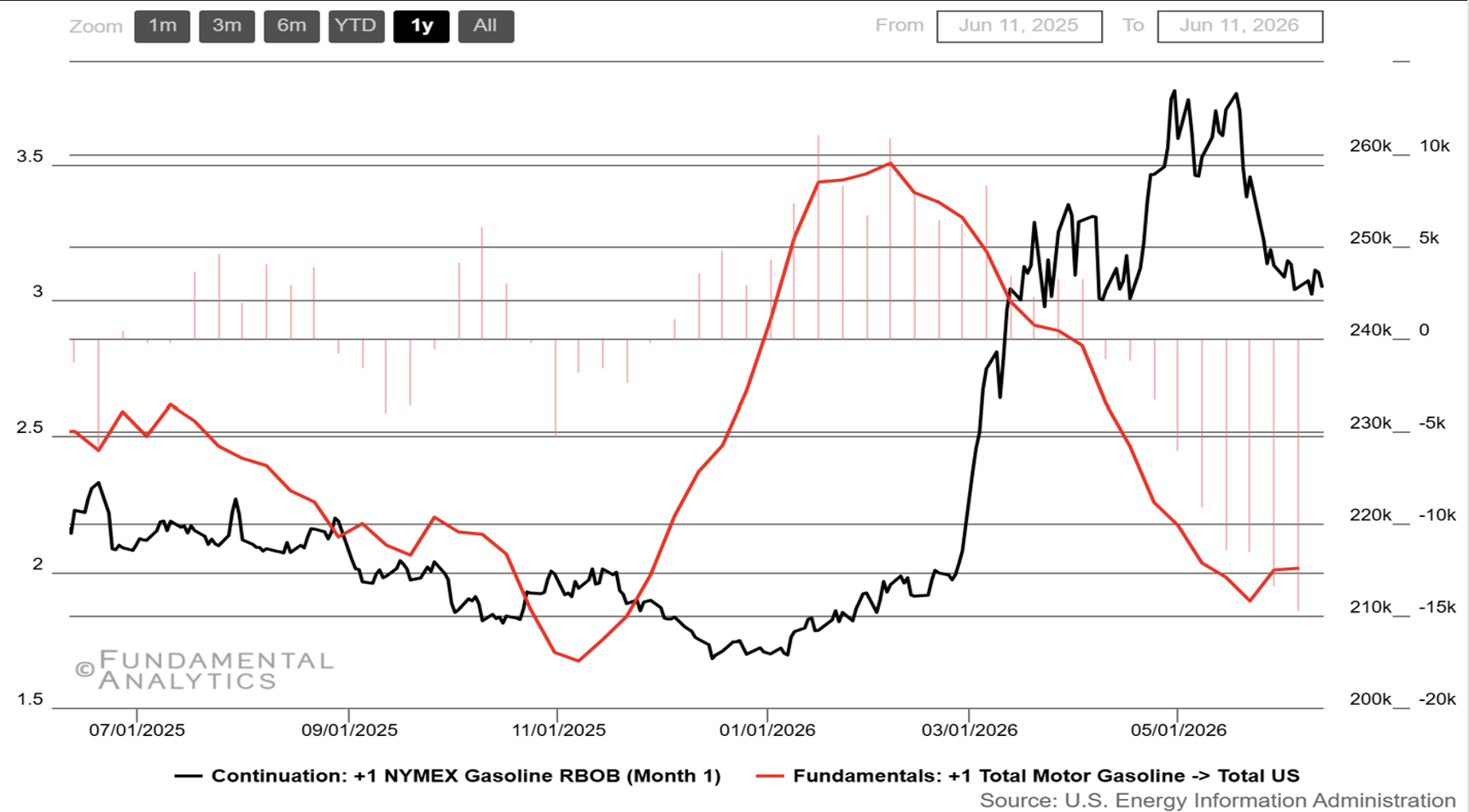

Gasoline

Gasoline Prices stay above $3, as demand strengthens

- Gasoline stocks rebuilt, but from a thin cushion: after a near-record run of inventory draws, two consecutive weekly builds eased immediate scarcity fears, though U.S. gasoline inventories remained materially below seasonal norms.

- Refinery runs surged into summer demand, adding supply-side relief: utilization moved into the mid-90% area as refiners lifted throughput to replenish depleted product stocks and offset disrupted global fuel flows.

- Demand was supportive, but price-sensitive: implied gasoline consumption improved into the summer driving season, yet remained soft versus last year, suggesting high pump prices were starting to restrain end-user demand.

- Geopolitics kept a risk premium under the market: the Iran war and restricted Strait of Hormuz flows continued to distort crude and refined-product logistics, keeping RBOB sensitive to any renewed escalation headline.

- Prompt prices eased as product builds met peace-deal optimism: RBOB softened as inventory relief, weaker post-holiday demand signals and expectations of a potential Gulf de-escalation reduced the urgency to chase front-month length.

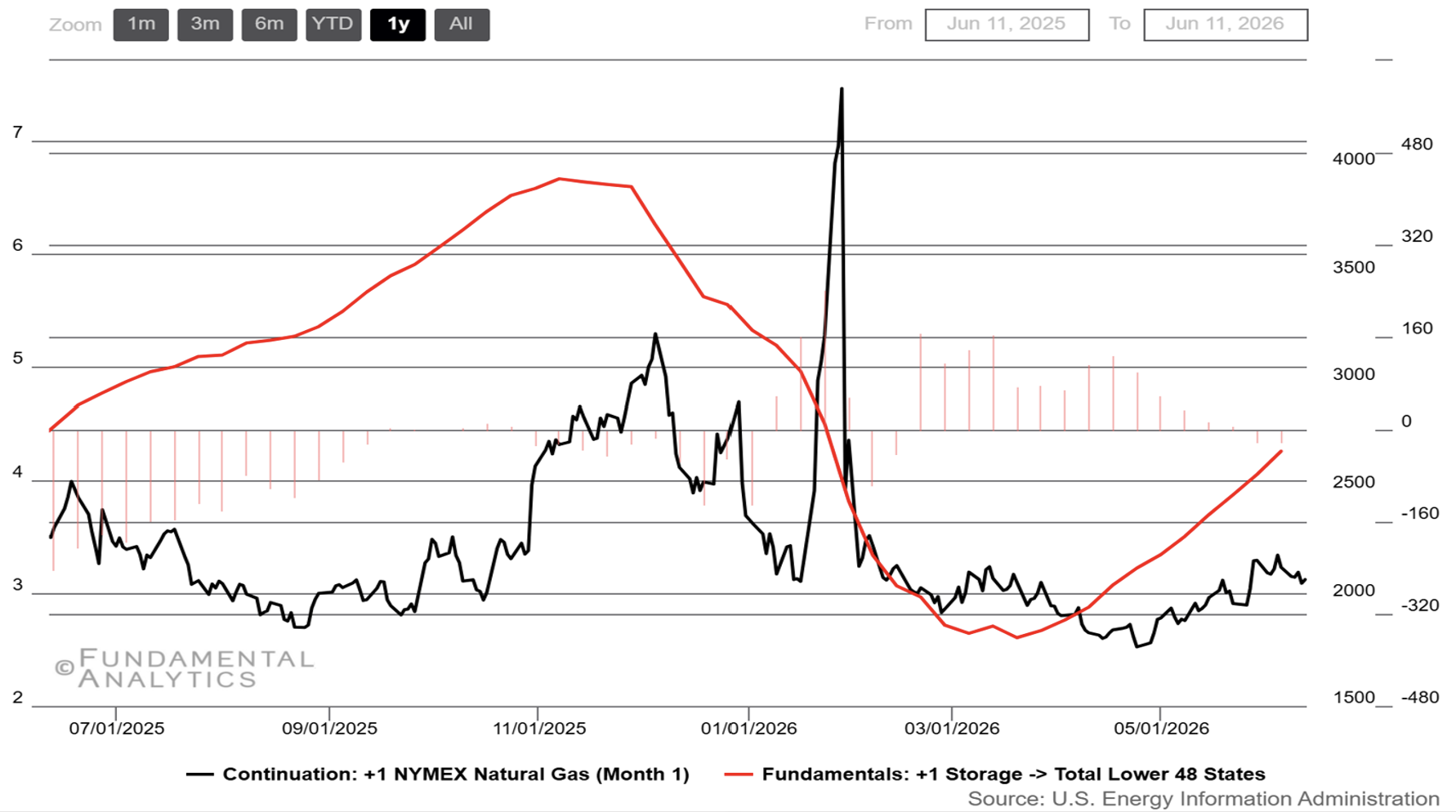

Natural Gas

Natural Gas Prices struggle due to Storage surplus

- Storage surplus reasserted bearish pressure: another triple-digit injection kept inventories comfortably above the five-year average, limiting the front month’s ability to sustain weather-led rallies.

- LNG maintenance weakened the marginal export bid: feedgas flows to U.S. LNG plants slipped from May levels as spring maintenance hit key facilities, briefly removing one of the strongest demand supports.

- Warmer forecasts brought back a power-burn floor: hotter-than-normal outlooks into late June lifted expectations for gas-fired generation, helping the contract recover after earlier weakness.

- Output softened, but not enough to flip the balance tight: Lower-48 production eased from record levels, narrowing the storage surplus, while EIA’s updated outlook still points to record 2026 supply.

- Global LNG geopolitics supported sentiment, not the domestic balance: Hormuz-related LNG disruption and stronger Asian buying kept international gas risk premia elevated, but U.S. prices stayed anchored by ample storage and maintenance-hit exports.