|

Energy prices wrestled with mixed signals: sharp U.S. crude draws and holiday travel demand collided with looming OPEC+ supply hikes, refinery outages, ballooning gasoline stocks, LNG maintenance, and well-supplied European storage. |

|

|

|

Crude Oil

De-escalation in the Middle East and expectations of lower demand slash WTI prices following recent rally |

|

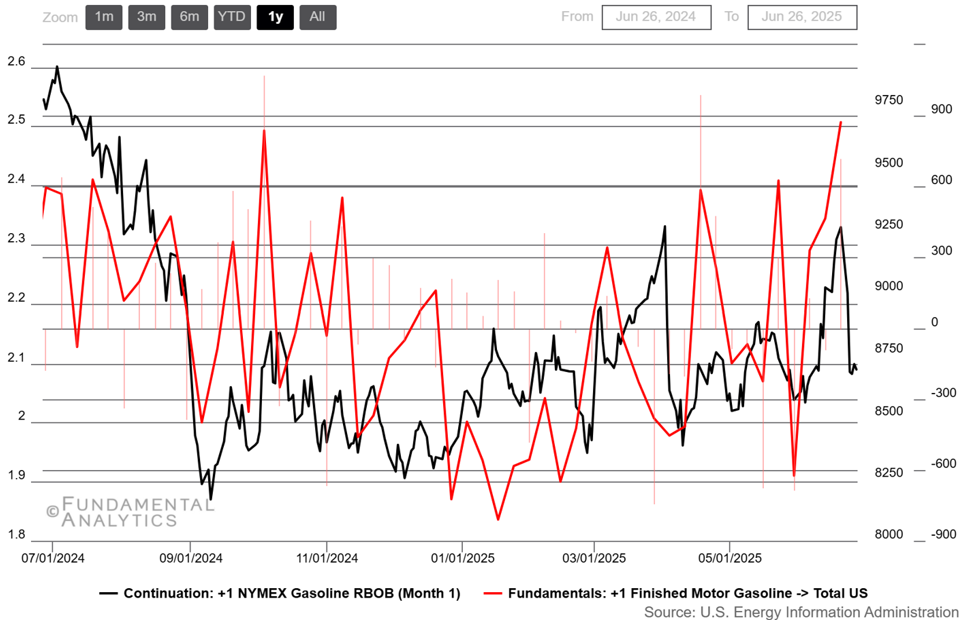

Gasoline Gasoline prices revert as production soars more than expected |

|

Natural Gas Natural gas futures partially rebound |

|

|