WTI trended lower on surplus expectations, fading risk, and slow-shale response. RBOB dipped as inventories rebuilt after outages, despite crack-driven volatility. Henry Hub swung with weather, production, and LNG demand.

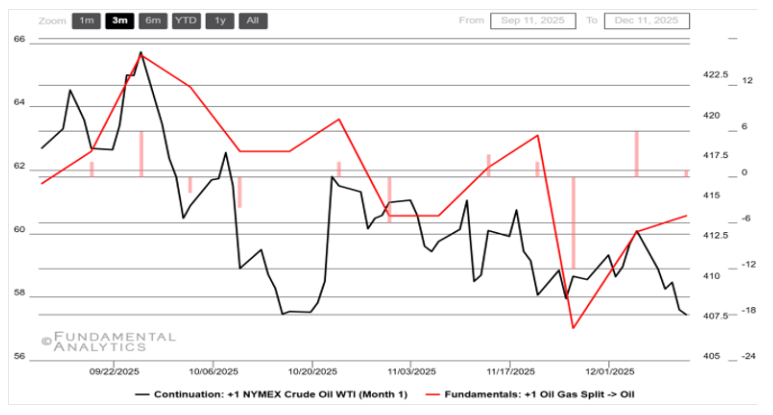

Crude Oil

WTI at 2-month low, Supply fears can’t support bullish movement

- Macro tone turned bearish: Prices mostly drifted lower because the market increasingly priced a global supply surplus (IEA-style “more barrels than demand”) while demand signals looked patchy—especially around Asia/China, where imports ran ahead of refining needs (more crude heading into storage rather than immediate consumption).

- OPEC+ put a floor—but not a trend reversal: Periodic support came when OPEC+ leaned into “manage the taper” (pausing/slowing planned output increases), yet rallies tended to fade because the broader balance still looked loose.

- U.S. shale sent mixed signals: Rig counts slid to multi-year lows (a forward-looking bullish cue), but near-term supply didn’t tighten fast enough to lift front-month prices—productivity and existing output kept barrels flowing, so the rig drop read more like future constraint than immediate scarcity.

- Geopolitics didn’t “stick” as a bid: Headlines (Russia-Ukraine diplomacy and Venezuela flow disruptions) moved prices intraday, but the risk premium generally compressed because traders judged that ample supply/surplus expectations outweighed disruption risk—so geopolitics became a volatility driver, not a sustained uptrend catalyst.

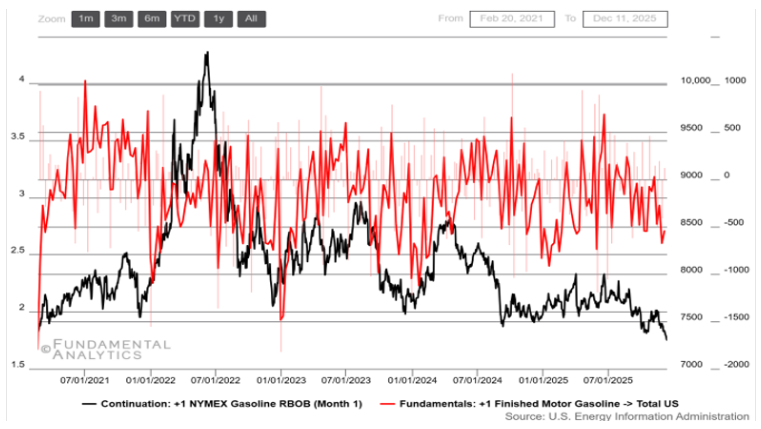

Gasoline

Gasoline prices plummet to 3-year low, Production diminishes, Demand softens

- Post-summer tightness, brief strength: RBOB caught early support from unexpected gasoline stock draws and refinery outages that constrained prompt supply, widening gasoline’s “tightness” versus crude and creating upside bursts.

- Autumn grinds lower on balance easing: As the market moved into the shoulder season, refinery maintenance and softer implied consumption shifted the narrative toward inventory rebuilding/looser prompt supply, pulling RBOB back in line with a generally weaker energy tape.

- Choppy tape driven by cracks and runs: Even while outright prices leaned down, refining margins and gasoline cracks stayed elevated at points (outages/maintenance and Russia-linked constraints), producing intermittent rebounds rather than a straight-line selloff.

- Early-winter pressure: Demand flat + supply comfortable + geopolitics de-risked: RBOB softened toward multi-year lows as demand stayed sluggish/flat, maintenance concluded (more supply), and crude’s oversupply and Russia-Ukraine peace-talk optimism compressed the risk premium that can spill into products.

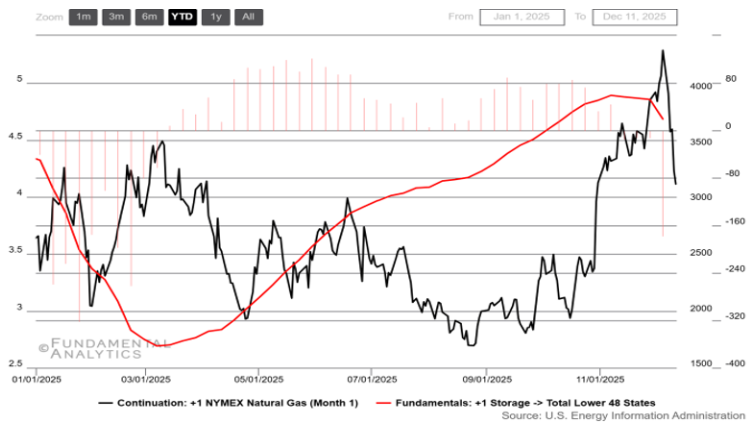

Natural Gas

Natural Gas abruptly falls on above-average temperatures in US along with ample production

- Shoulder-season softness kept a lid on prices: NYMEX Henry Hub traded with a bearish tilt early in the window as comfortable inventories (storage sitting modestly above the 5-year average) and record/near-record U.S. output made the market highly sensitive to any warm-leaning forecast revisions.

- Weather drove the biggest swings: When forecasts flipped colder, prices jumped hard on heating-load repricing and larger storage withdrawals—but the rally quality depended on how long cold risks persisted in the models.

- LNG exports became the marginal demand lever: Record LNG feedgas/exports repeatedly tightened the balance and amplified upside moves—especially with Europe absorbing a dominant share of U.S. LNG flows during the last 3 months.

- Late-window givebacks came from “supply still ample and global de-risking”: Each warm-up reset triggered quick selloffs because production stayed high and storage remained within/above-normal range; meanwhile, softer European pricing/Ukraine peace optimism narrowed spreads, raising periodic concern that LNG economics could curb export pull (a downside feedback into Henry Hub).