Dr. Ken Rietz

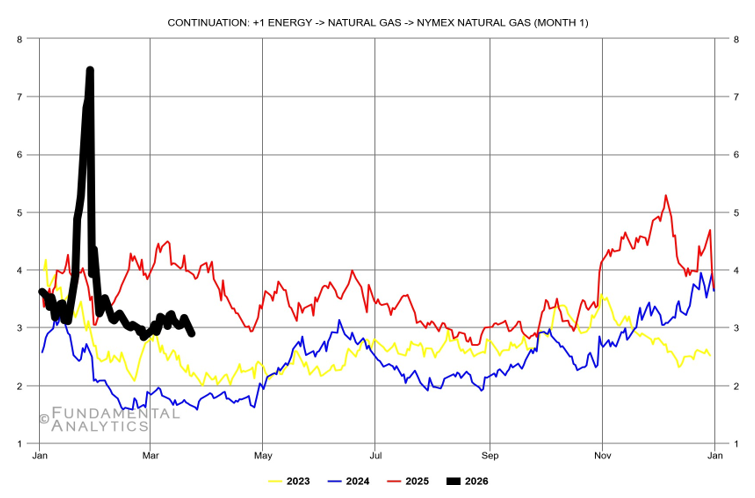

Wouldn’t you expect that Texas, the center of US refineries and LNG production, would be celebrating the price increases due to Iran’s blockade of the Strait of Hormuz? That would be incorrect. You may expect that West Texas Intermediate natural gas (that comes up with the crude oil) would be running cheap. But would you expect that the price is currently negative, and it has been negative more often than not since the beginning of the year? Bonkers, indeed. This week’s commentary will try to make sense out of these oddities. But first, here is the chart of the front-month futures on NYMEX natural gas.

Figure 1: Front-month futures for NYMEX natural gas

You can see the spike in price due to the Iranian war. But the price does not drop below zero, which I stated earlier. That is because the prices on the graph are for NYMEX natural gas (essentially the same at expiration as the price at Henry Hub), but the spot prices at the Waha gas trading hub in the Permian Basin were the ones that turned negative.

Let’s first dig into the reasons that Texas was not celebrating higher global crude oil prices. While gasoline prices are much cheaper in Texas than the US average, they are still up 30 percent over last year, so they are being felt. Despite the opportunity for more profit, US oil companies are not planning on any expanded drilling. The war has raised prices, but the extended duration of the war is not clear enough to justify changes in hiring right now. That means that the economy in the area is not going to benefit much. So, most of Texas is only going to see higher gasoline prices and no jump for the economy. Cancel the celebration.

The more intriguing fact is that the price of natural gas at the Waha hub keeps going negative. The wells that bring up WTI crude oil from the Permian also bring up natural gas at the same time. There are extensive pipelines to carry away the crude oil, but the pipelines for carrying the natural gas have much less capacity. That leaves an abundance of natural gas to deal with. When there is more natural gas than can be handled, the price can drop below zero, meaning that the oil producer would have to pay to have it removed. In that case, the easier solution is to flare it off. There are problems with that, too, mainly with the environmentalists. The satellite named MethaneSAT, launched by the Environmental Defense Fund, Harvard University, and others, watches for methane (that is, natural gas) emissions. The Permian Basin has been producing methane emissions (from incompletely flared natural gas) well beyond what the EPA estimates. Senator Whitehouse (D-RI) has demanded that this be investigated, citing eight oil-producing companies and requesting that they hand over documentation regarding their methane emissions. Seven of the eight companies belong to the Oil and Gas Methane Partnership 2.0, a global emissions-reduction program for oil and gas companies overseen by the United Nations Environment Programme. The senator asserts that methane emissions can be reduced “at little to no cost.” There is considerable disagreement between different sides of this issue.

How do you trade these puzzles? The fact that the US is not planning on increasing hiring to increase production means that the supplies of crude oil and natural gas are going to continue to drop as time goes on. The success of Trump’s proposed security coalition could change the status of crude oil and natural gas global supplies. This is another wild card that needs to be considered. Depending on how successful you expect the coalition to be, investing either in calls (if the coalition collapses) or puts (if the coalition succeeds) on crude oil and natural gas futures would be reasonable. The stock market in general now appears to lean in the direction of the coalition collapsing. That, however, is subject to change.