Grains stayed capped by WASDE and large South American crops; Russian exports and Ukraine’s corridor eased risk; U.S. sales helped, ethanol softened; soybean crush and rising soyoil stocks limited rallies.

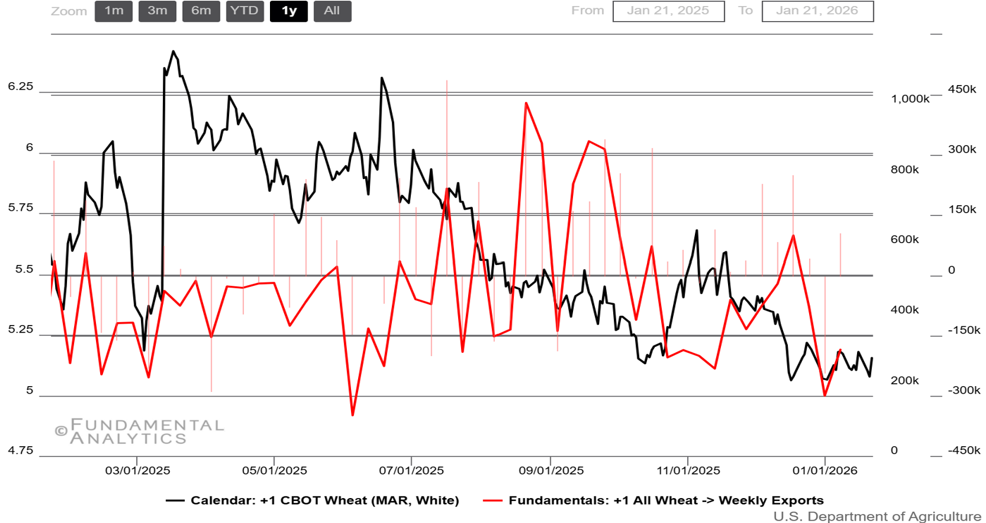

Wheat

Improved exports keep momentum for prices, but ending stocks are considerably high

- Stocks over supply: USDA’s January outlook lifted global wheat production to a new record and raised 2025/26 ending stocks to a 5-year high, trimming the U.S. farm price and capping rallies.

- Russia opened the taps: Moscow reset the wheat export duty to zero and extended it; the 2026 grain export quota was set at 20 MMT, adding FOB pressure from Black Sea origins.

- Flows kept moving: Ukraine’s maritime corridor reached 100 MMT of grain since launch, while Algeria issued a March-shipment wheat tender—demand channeled largely toward non-U.S. suppliers.

- Freeze scare, limited bite: A U.S./Russia cold snap injected a brief weather risk premium, but coverage noted widespread snow cover likely limited winterkill.

- Export pulse improved: Weekly U.S. wheat export sales jumped to 303,284 MT (week ended Jan 8), offering near-term support without altering the heavier global balance.

Corn

Corn futures at 3-month low on softened exports

- USDA raised the cushion: Jan WASDE lifted U.S. 2025/26 corn production and ending stocks (feed use up, exports steady), keeping Mar ’26 rallies contained.

- South America’s production picture remains robust: CONAB’s corn outlook eased only slightly, and Argentina reported broadly good early-corn conditions; export competition into mid-2026 is expected to stay strong.

- Exports supportive, not explosive: Mid-January FAS data showed sizeable U.S. sales/shipments led by Mexico, Japan, and South Korea—helpful for basis, but not enough to tighten the balance.

- Domestic demand steady-to-softer: Weekly EIA showed ethanol output easing from early-January highs, tempering corn grind momentum.

- Black Sea logistics improved flow, limiting risk premia: Ukraine’s maritime corridor surpassed 100 MMT moved, keeping global feed-grain availability comfortable.

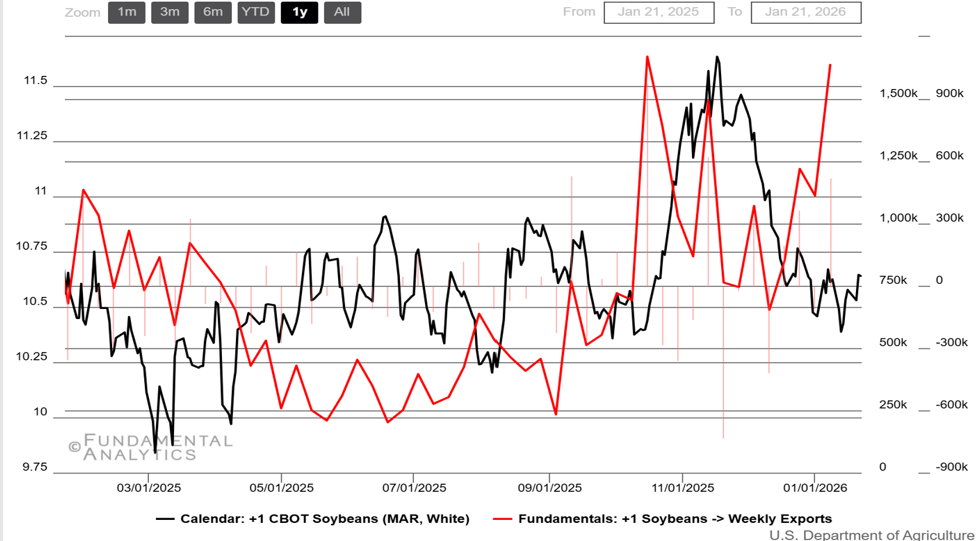

Soybeans

Soybeans exports hit mid-year high, providing support to futures

- WASDE/ERS tilted the balance heavier: Global soybean output and ending stocks rose; U.S. crush was raised, exports trimmed, and biofuel soyoil use cut, capping Mar ’26 rallies.

- South America stayed big despite tweaks: Brazil’s 2025/26 crop still projects at/near a record; Argentina planting passed 96% with some excess-moisture delays, keeping export competition intense.

- China demand is supportive but state-led: Record 2025 imports and state buying fulfilled the 12-MMT U.S. pledge, while private crushers kept favoring cheaper South American origin.

- U.S. sales pulse improved: Mid-January weekly export sales hit a marketing-year high, brightening near-term demand optics without offsetting heavier global supplies.

- Crush strong, oil stocks heavier: NOPA’s December crush hit nearly 225 mbu (new December high), while soyoil stocks climbed—supporting meal but tempering the oil leg.