WTI pressured by U.S. builds and surplus outlook; RBOB range-bound on ample stocks, slower shoulder-season demand; natural gas capped by above-average storage, robust production, easing LNG feed-gas.

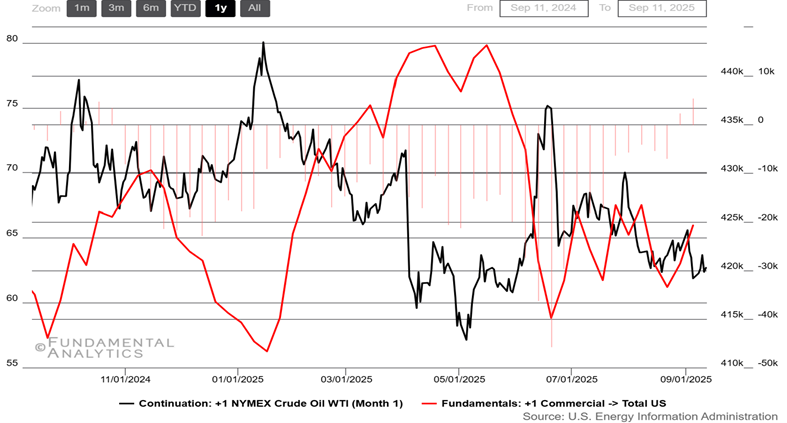

Crude Oil

Biggest build-up since late October 2024

- U.S. balances loosened. EIA’s latest two reports showed back-to-back crude builds (+2.4 mb, then +3.9 mb), refinery runs near 95%, gasoline demand soft on a 4-week basis, and sizable distillate builds—pressuring WTI.

- Global supply outlook tilted bearish. The IEA said supply growth—helped by OPEC+ unwinding cuts and robust non-OPEC output—should outpace demand, pointing to a growing surplus and capping rallies.

- U.S. shale signals a slow, steady capacity to respond. Baker Hughes reported a small uptick in the oil-rig count (close to 416), hinting at incremental future supply rather than a rapid surge.

- Geopolitics added noise but limited net disruption. Washington tightened sanctions on Iran-linked oil shipping networks, while G7 partners moved to tighten Russian price-cap enforcement; flows persisted via “shadow fleet” workarounds, muting risk premia.

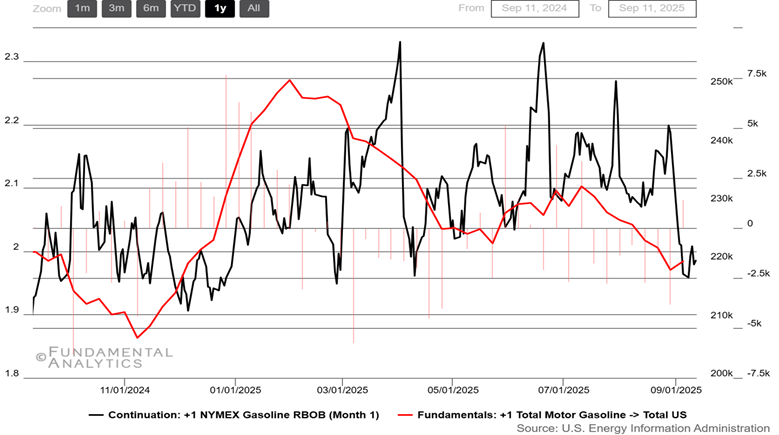

Gasoline

Consecutive draws came to an end, futures squeezed

- Stocks fluctuated but stayed ample. EIA reported a sizeable gasoline draw followed by a +1.5 mb build, with the 4-week motor-gasoline supplied ~8.9–9.1 mb/d (≈flat to −1% y/y) and refineries near 94–95%—a setup that limited RBOB upside.

- Seasonal demand decelerated. AAA flagged softer post-summer driving and a national retail average near $3.19/gal, while EIA’s September outlook pointed to easing prices into 2026—both consistent with weaker shoulder-season pull on futures.

- Imports cushioned the East Coast. Gasoline (and components) arrivals rose to ~0.68 mb/d after ~0.58 mb/d the prior week, helping balance regional supply even as domestic production eased—another headwind for sustained rallies.

- Limited weather/geopolitical premium. Despite peak hurricane season and occasional risk headlines, the Atlantic stayed unusually quiet and crude softened on oversupply/weak U.S. demand concerns, keeping RBOB largely range-bound.

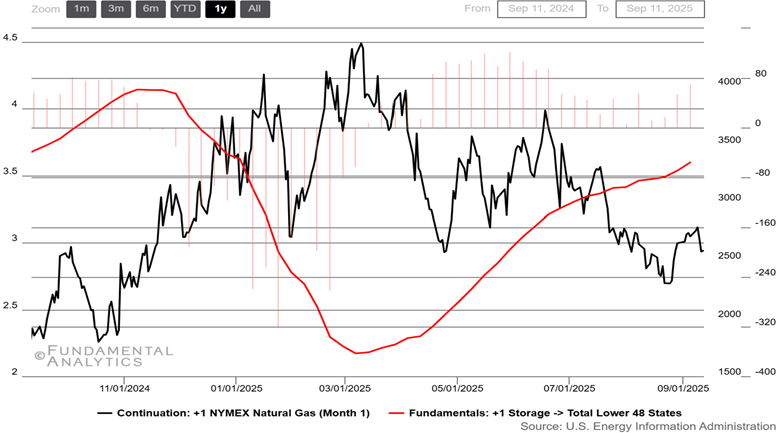

Natural Gas

Larger than average buildups pressure natural gas prices

- Storage remained a headwind. EIA reported a larger-than-average +71 Bcf injection, lifting inventories to 3.343 Tcf (≈6% above the 5-yr norm)—a surplus that limited upside in NYMEX gas.

- Supply steady; LNG pull softer. Dry output averaged around 107 Bcf/d and LNG pipeline receipts hovered near 16 Bcf/d, while early-September feed-gas slid toward 15.5 Bcf/d, modestly loosening balances.

- Cooling curbed power burn. With milder temperatures across key regions, gas-fired generation fell nearly 4% w/w, offsetting heat-related demand pockets and dampening follow-through on rallies.

- External demand signals stayed muted. Europe’s well-stocked storage and calm market tone reduced urgency for additional U.S. LNG cargoes, keeping export-led support limited.