Dr. Ken Rietz

This commentary attempts to look at the global wheat market by considering how its four biggest exporters are doing, followed by a detailed analysis of the movements of CBOT wheat futures, and then an evaluation of the global prospects for wheat on the basis of what we find. The four biggest exporters by volume are, in order, Russia, Australia, Canada, and the US. The same countries are the largest by export value of wheat, but the order changes some. Together, they account for 48% of exported wheat by volume, and so will be a determining factor in the global market. But first, we look at the chart of annual wheat exports for the US over the past several years.

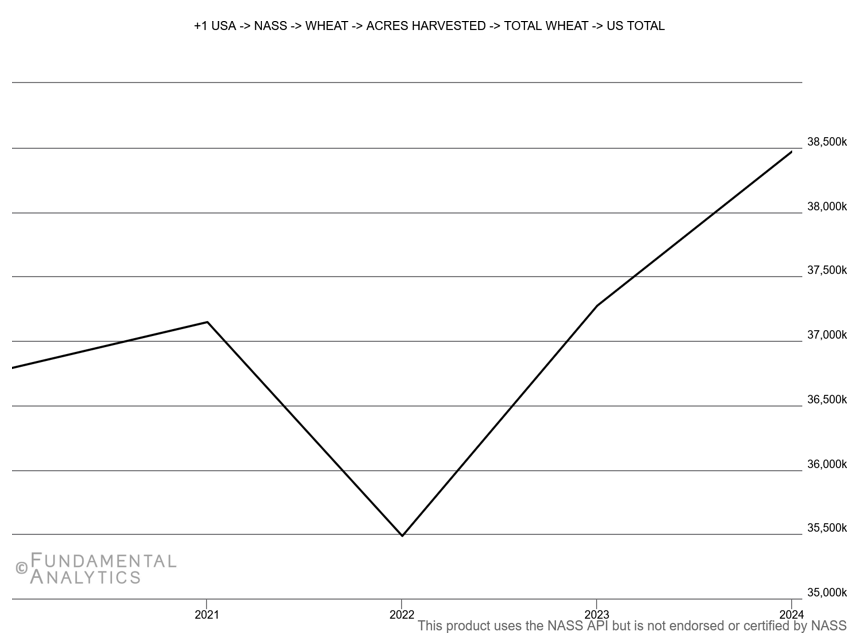

Figure 1: Amount of wheat harvested annually in the US

Our analysis will go country by country, in order of export volume. We begin, therefore, with Russia. The USDA has said that the Russian drought has diminished the amount of wheat harvested from 85 million tonnes to 83.5 million tonnes (-1.8%) and the amount exported from 46 million tonnes to 45 million tonnes (-2.2%) for this annual season. Additionally, Russia is nearly tripling its export duty on wheat, raising it to 495.9 RUB/t starting September 17th from 168.6 RUB/t earlier. The net effect of this price rise will dent the amount of wheat Russia exports, but the total drop is not yet clear. However, it has already increased the CBOT wheat futures. Clearly, the Russian contribution to exported wheat will be negative.

Australia, on the other hand, is doing very well this year. After starting the year with a forecast of lower harvest levels, rainfall increased estimated production significantly. This is particularly remarkable since Australia is the driest inhabited country, and the wheat-growing regions have soil that more resembles a beach than the usual dark, loamy soil of the US. The result of intense work on growing wheat there has produced remarkable results, which are showing a surplus wheat harvest this year. Even though China is the global leader for wheat production, it still has to import wheat to feed its people. China has purchased 4 or 5 shipments of 55,000 tons of wheat from Australia in just July and August. Australia is clearly adding to the global supply of wheat.

Canada is the other main source of wheat for China, though the amount of wheat China imports has been dropping since 2023. This year, Reuters described Canadian wheat as a “mixed bag.” Some parts of Canada have received abundant rain and are doing very well, while other parts have been in a drought. The northern plains have been particularly dry, but have very recently gotten a healthy amount of rain. Whether that will be good enough to revive the wheat crop is not yet clear. Overall, Canada’s addition to the global wheat crop is unclear; neutral is most likely.

Finally, we look at the US. The USDA reports are the framework on which the markets gauge their reactions. The report last Friday was so unclear that the market whipsawed. Neither algorithms nor human experts could determine what was going on. And yet, the overall trend for US exports is up 25 million bushels to 900 million bushels (+2.9%). Ending stocks of wheat are down slightly, and the average price per bushel dropped 25 cents to $5.10 (-4.7%). It looks as though the US will increase global production.

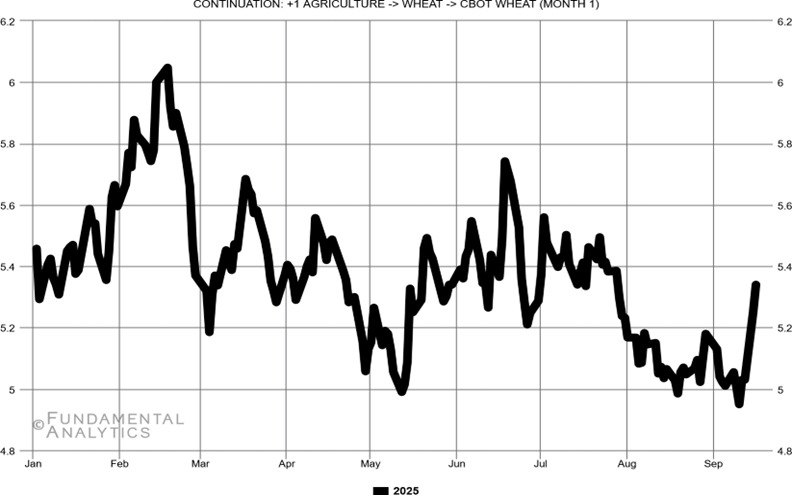

Now we take a much closer look at the price movement of CBOT wheat futures since the beginning of the year:

Figure 2: Amount of wheat harvested annually in the US

There are two major features to take note of. There was a spike in prices in mid-February, and then a slow drift downward to the present. The spike in prices in mid-February had several causes: weather, geopolitical risk, and aggressive exports. Specifically, there was extremely cold weather over much of the US, and also in the Black Sea area, causing concern about “winterkill” in the wheat. Then a drought settled into the Southern parts of the wheat-growing area. Additionally, Russia launched heavy attacks against Ukrainian energy, creating concern about Black Sea wheat deliveries. All of these combined drove the wheat futures up. But why did the futures price of wheat enter a long, slow decline up to the present? Partly, the concerns listed above turned out not to be as serious as initially thought, and it was determined that sufficient supply was available.

The weather moderated enough to calm fears. The Black Sea grain exports grew aggressively, and put pressure on US wheat prices. Finally, a strong dollar tends to put pressure on the price of futures. All these combined explain the general movement of CBOT wheat futures since the beginning of the year.

The global situation looks good. The global production of wheat last year increased by 2 million tons to 793 million tons (+0.25%). The market has already priced in the places that are underproducing due mainly to drought, so the prices are not as likely to continue going up. On the other hand, rain relief in those areas will cause the price to go way down. So, a speculative trader might consider selling wheat futures, but this is more of a gamble than usual, so keep the position light.