CBOT grains flattened as U.S. wheat harvest/planting advanced, soybeans balanced heavier, and record corn output loomed.

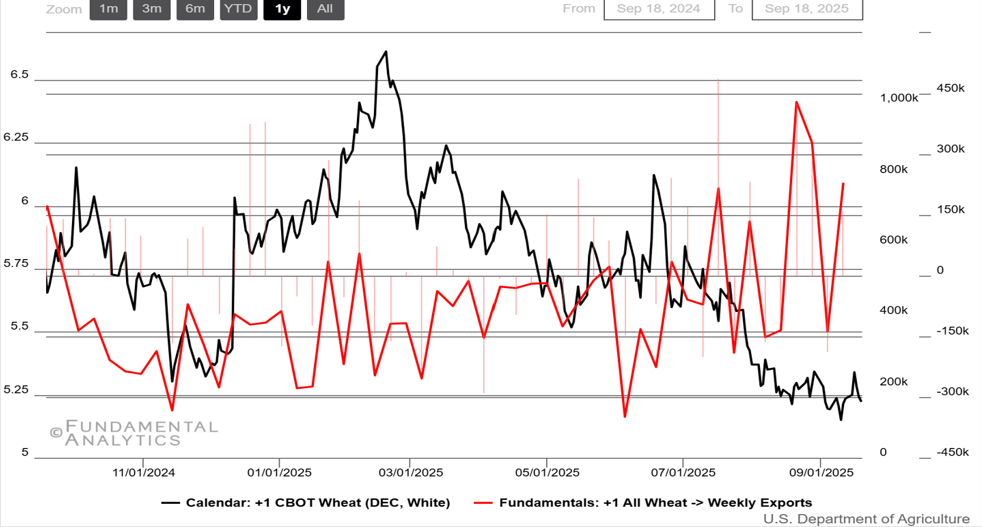

Wheat

Wheat futures struggle, despite steady exports

- U.S. harvest/planting kept nearby supply comfortable. Crop Progress showed spring-wheat cutting advancing from the mid-80s to the mid-90s percent range while 2026 winter-wheat seeding ramped up, limiting carry in December spreads.

- Export demand is steady but unspectacular. USDA’s weekly report logged 377.5 Kt in net sales and 774.8 Kt shipped, decent volumes yet below recent averages—supportive for basis but not enough to drive a board breakout.

- Europe/Black Sea competition weighed. Euronext softened as a firmer euro and cheaper Russian offers eroded EU export hopes, while FranceAgriMer flagged lower protein shares in the new French crop, complicating milling premiums and inter-origin spreads.

- Geopolitics and global demand signals cut two ways. Odesa-region drone strikes kept corridor risk in headlines, but India’s government stocks swelling to a four-year high reduced near-term import prospects, netting to a muted risk premium in December CBOT.

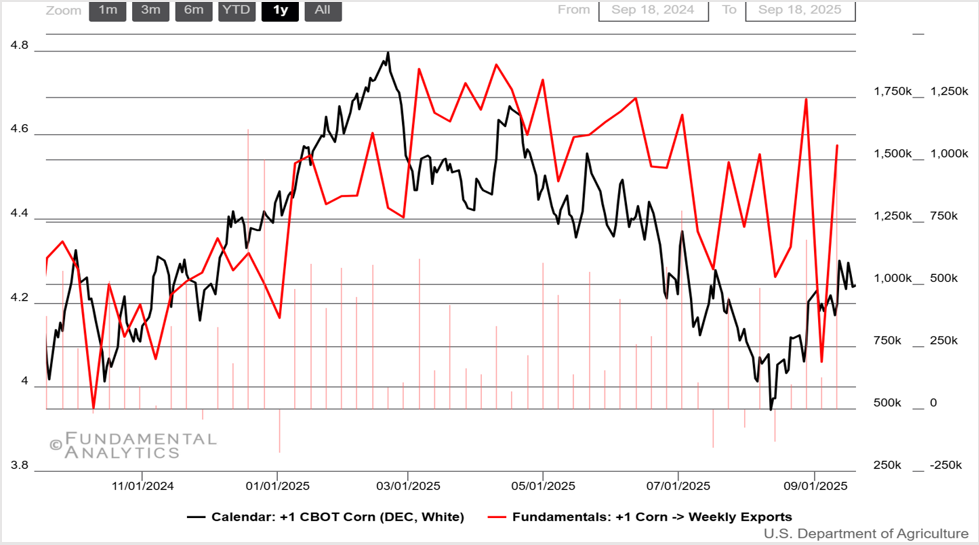

Corn

Corn exports elevated, prices reach 2-month high

- Heavy U.S. supply narrative persisted. September WASDE projected a record U.S. corn crop (~16.8 billion bushels), while Crop Progress kept conditions in the high-60% good/excellent and harvest just starting, limiting weather premia in Dec.

- New-crop export bookings improved, but not decisively. Weekly FAS tallied ~1.23 MMT of 2025/26 sales (week ended Sept 11) and brisk shipments, offering support yet failing to shift overall bearish sentiment for December futures.

- Brazilian competition stayed formidable. ANEC lifted September corn-export guidance to ~7.1 MMT, extending South America’s price advantage and pressuring U.S. Gulf offers and CBOT spreads.

- Domestic demand remains steady, geopolitics mostly neutral. EIA-tracked ethanol metrics showed demand is steady while production slipped w/w, and EU tariff resets mainly targeted wheat/barley, leaving corn flows largely unaffected during the window.

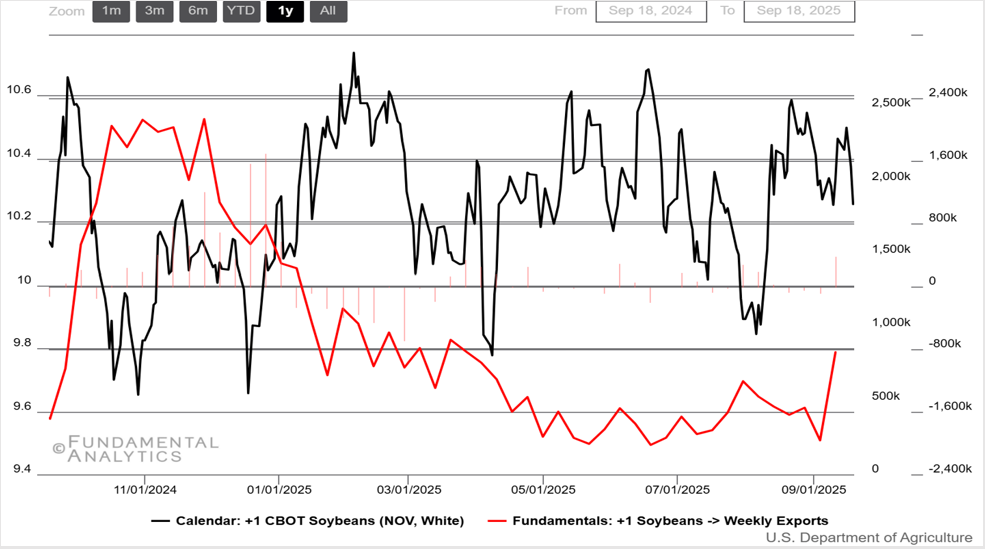

- Soybeans

Exports strengthened, futures range 10.3-10.5

- U.S. balance sheet tilted heavier as fields held up. September WASDE nudged 2025/26 U.S. soybean ending stocks higher while production was raised; mid-month Crop Progress kept conditions in the mid-60s % good/excellent, muting weather premia in Nov futures.

- New-crop export sales improved, but China remained scarce. USDA tallied 541 Kt of week-one sales, then 923 Kt the next week, led by Europe and Mexico; Reuters noted Chinese buyers were still leaning heavily on South America.

- Brazilian flow undercut U.S. offers. ANEC lifted its September soybean export projection toward ~7.5 MMT, reinforcing aggressive FOB Paranaguá values and weighing on Chicago spreads during the window.

- Policy signals added background noise without curbing supply. Brazil’s competition authority ordered a suspension of the industry’s “soy moratorium,” injecting ESG/policy uncertainty even as export programs proceeded apace.