Energy futures mixed: WTI steadied on U.S. draws but was capped by surplus outlook; RBOB tightened yet was constrained by demand and winter shift; natural gas was pressured by storage and muted LNG.

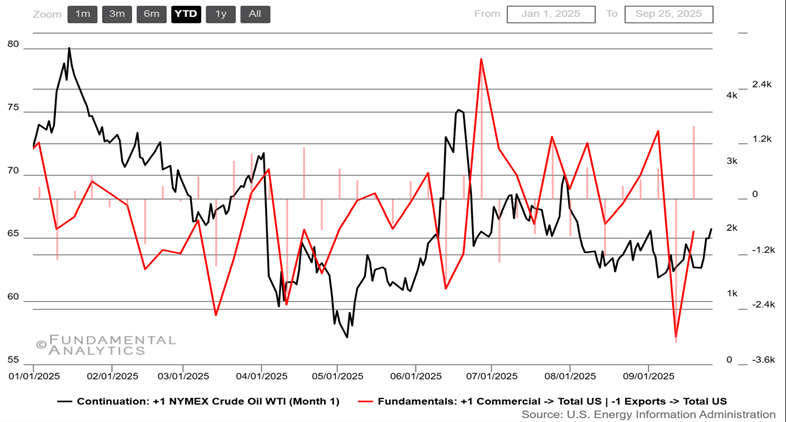

Crude Oil

US average Net Imports plummeted more than 40% y/y in September

- U.S. balances tightened, then eased modestly. Mid-September EIA data showed a much larger-than-expected crude draw alongside firm exports; the following week posted a small draw with refineries near 93% and gasoline/distillate stocks lower—supportive but not explosive for WTI.

- Global supply expectations stayed bearish-tilted. The IEA’s September report projected robust 2025 supply growth from both non-OPEC+ and OPEC+ producers, reinforcing a narrative of ample barrels that tempered rally attempts.

- Shale signals implied only a gradual response. Baker Hughes counts indicated a small uptick in U.S. oil rigs through September, suggesting incremental future supply additions.

- Geopolitics added flickers of risk premium. Reports of Ukrainian drone strikes impacting Russian fuel output and talk of Kurdish flows resuming to Ceyhan injected headline volatility, but disruptions were not large enough to reprice the broader supply outlook.

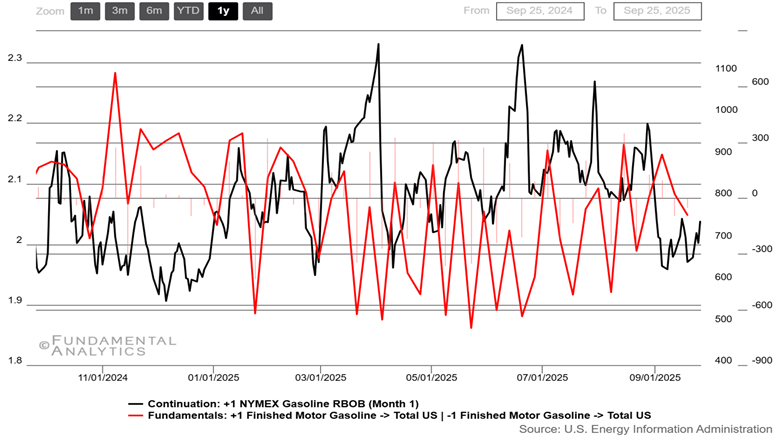

Gasoline

US struggles to strengthen Gasoline exports

- Stocks tightened, but demand remained steady. EIA reported back-to-back U.S. gasoline draws (-2.3 mb, then -1.1 mb), leaving inventories ~1–2% under the five-year norm while the 4-week “product supplied” hovered ~8.8–8.9 mb/d.

- Runs high; imports cushioned the East Coast. Refineries operated near 93% with gasoline output rising from ~9.4 to ~9.7 mb/d; gasoline (and components) imports averaged ~0.51–0.57 mb/d—an adequate supply that tempered RBOB rallies.

- Seasonal spec shift leaned bearish. The mid-September transition to winter-blend gasoline—cheaper to produce and more flexible on RVP—kicked in, historically easing wholesale costs and softening crack spreads.

- Weather/geopolitics added little net premium. Atlantic activity stayed mostly offshore (e.g., Hurricane Gabrielle near Bermuda), and with U.S. refining largely unaffected, headline risk didn’t translate into sustained NYH tightness.

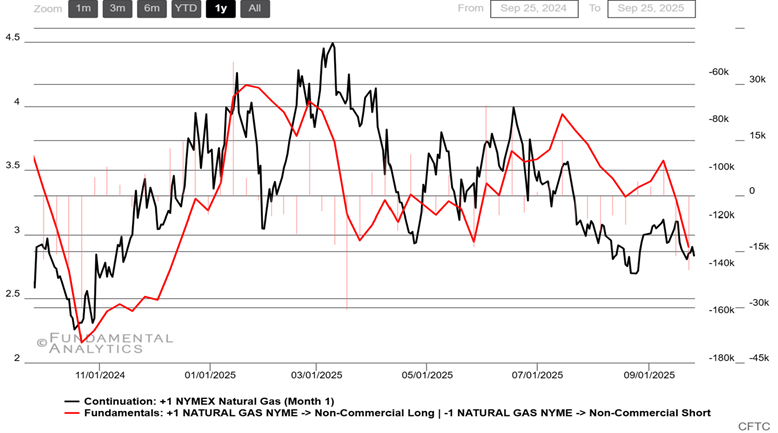

Natural Gas

Speculators’ funds indicate bearish cycle for Natural Gas

- Storage surplus capped rallies. EIA reported a +75 Bcf injection, lifting working gas to 3,508 Bcf (+6% vs 5-yr avg)—a comfortable cushion that kept NYMEX gains in check.

- Supply sturdy; LNG pull mixed. Dry output held near ~106–107 Bcf/d, while LNG feed-gas averaged ~16.3 Bcf/d; Cove Point maintenance and a Sabine Pass intake dip tempered overall receipts.

- Power burn firmed only modestly. Late-September warmth lifted gas-fired generation ~4% w/w, but the uptick wasn’t enough to overcome ample inventories and steady production.

- External demand signals stayed soft. Europe’s storage remained very high (EU above mandated thresholds; Poland at 100%), limiting urgency for U.S. LNG cargoes and reinforcing a bearish tilt.