Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s energy topics include:

- LNG: The US is set to overtake Norway as Europe’s largest gas supplier in 226, with American terminals now accounting for two-thirds of European LNG.

- Crude Oil: Brent has held above $100/barrel for the past two months, though the backward-dated futures curve is being misread as a price forecast rather than a reflection of physical market tightness.

- Gasoline: The House passed year-round E15 sales legislation, offering a potential pump price relief valve pending approval from the Senate.

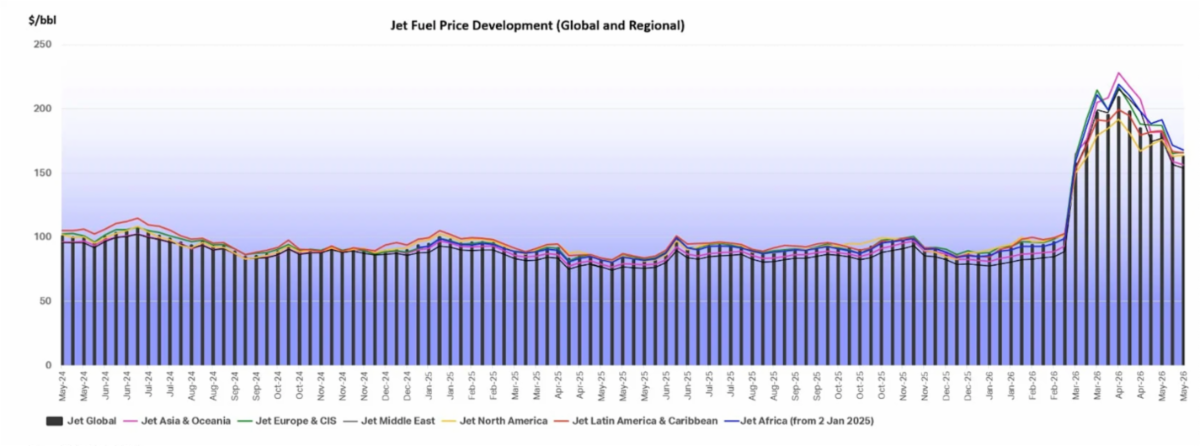

- Wild Card: Global jet fuel prices spiked above $200/barrel in April before easing to around $150 in May, forcing airlines to absorb billions in additional costs ahead of travel season.

Let’s begin.

LNG

Source: Fundamental Analytics

Source: Trading Economics

US is Set to Become Europe’s Largest Gas Supplier, Overtaking Norway

The Maritime Executive

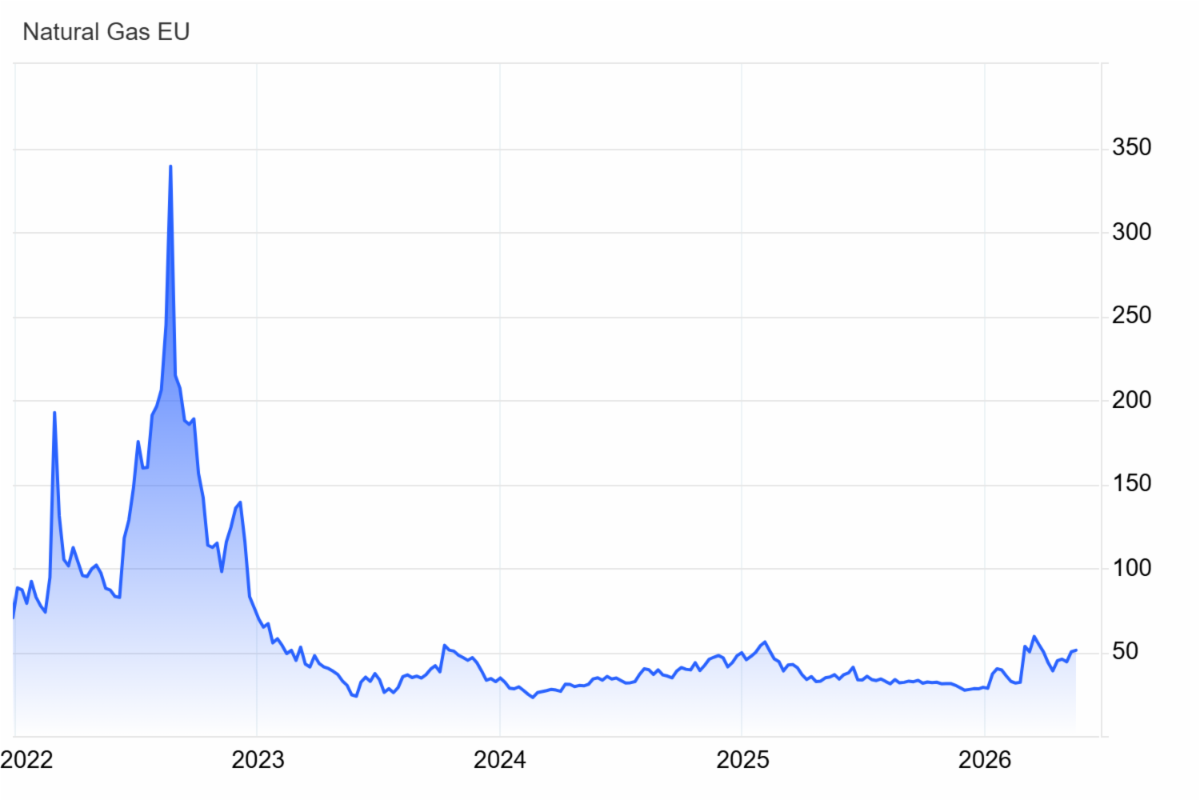

The United States is on track to become the European Union’s largest gas supplier in 2026, overtaking Norway for the first time, according to a new analysis by the Institute for Energy Economics and Financial Analysis. The shift is being driven by the rapid buildout of U.S. Gulf Coast liquefaction capacity and the sudden displacement of Middle Eastern supplies following the Iran conflict, which has left Qatar, normally the world’s second-largest LNG exporter, effectively locked out of efficient global shipping lanes by the situation in the Strait of Hormuz. American terminals now account for roughly two-thirds of all European LNG imports, a share IEEFA projects could reach 80% by 2028. In contrast, Russian LNG flows into Europe are simultaneously rising to their highest level since the invasion of Ukraine, up 16% year-on-year in Q1, even as the EU moves toward a formal ban on those cargoes by the end of next year. IEEFA analyst Ana Maria Jaller-Makarewicz warned that LNG has become “the Achilles’ heel of Europe’s energy security strategy,” exposing the continent to price volatility and new forms of supply disruption. The two charts below illustrate the transatlantic dynamic at play: NYMEX natural gas (Chart 1) surged to nearly $8/MMBtu in early 2026 before pulling back to around $3, while EU natural gas (Chart 2) after its dramatic 2022 crisis spike above 340, has stabilized in the €40–60/MWh range but remains elevated relative to 2024 lows, reflecting Europe’s continued role as the premium destination market pulling U.S. LNG volumes eastward despite ongoing geopolitical uncertainty.

Crude Oil

Source: Fundamental Analytics

Why the Oil Futures Curve is Not a Crystal Ball

Jonathan Vincent & Malcolm Moore, Financial Times

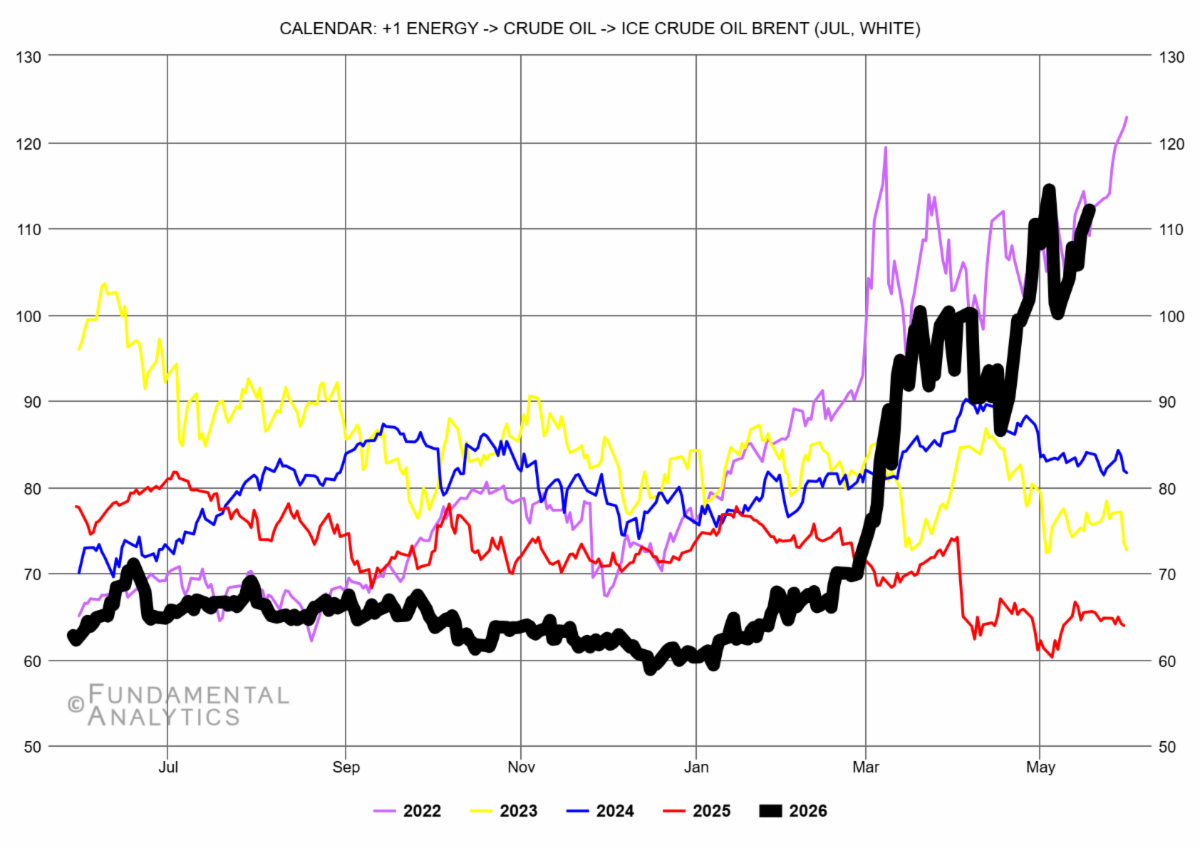

Brent crude has remained above $100/barrel for most of the past two months as the Iran conflict has effectively halted flows through the Strait of Hormuz. The White House has repeatedly pointed to the oil futures curve as evidence that high prices are temporary. Treasury Secretary Scott Bessent cited the backward-dated structure on May 4 as proof that traders expect relief within months, but analysts and traders are pushing back hard on that interpretation. Futures contracts represent what hedgers are willing to lock in today, not a consensus forecast of future prices: oil producers selling forward to secure revenue and refineries buying to fix input costs are the dominant forces shaping the curve, not directional price bets. As Spencer Dale, former BP chief economist, noted, the steep front-end slope signals an extraordinarily tight physical market right now, not a reliable read on where prices will be in 12 months. Meanwhile, the options market is telling a more candid story about uncertainty. The probability implied by options of oil reaching $140 by December has risen sharply since the war began, and contracts tied to $150, or even $200 oil, are now regularly trading as hedges against a prolonged supply disruption. Traders remain reluctant to load up on deferred contracts precisely because a ceasefire or Strait reopening could flood the market quickly. The calendar chart outlines 2026’s trajectory: Brent (black) bottomed near $60 in late 2025 before surging above $115 by May, a move that has now eclipsed 2023 and 2024 price ranges entirely and is approaching the volatility levels last seen during the 2022 energy shock.

Gasoline

Source: Fundamental Analytics

US House Passes Bill Allowing Year-Round Sales of E15 Gasoline

Siddharth Cavale, Reuters

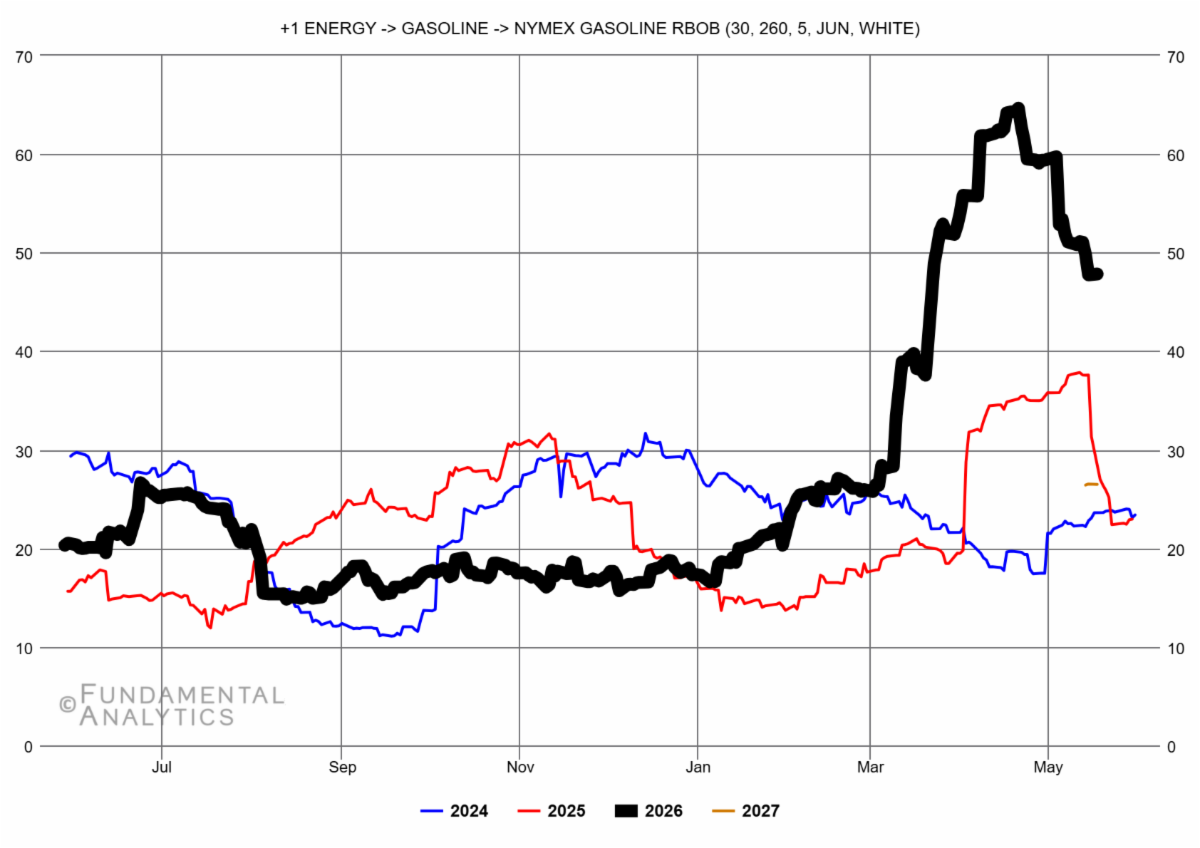

The U.S. House passed the Nationwide Consumer and Fuel Retailer Choice Act on May 14 by a narrow 218-203 vote, clearing the way for year-round nationwide sales of E15 gasoline. If it clears the Senate’s 60-vote threshold and receives President Trump’s signature, the legislation will remove existing seasonal restrictions on E15 tied to summertime smog concerns, handing a significant victory to corn farmers and biofuel producers who have pursued the measure for years. Supporters argue E15, typically 20–40 cents cheaper per gallon than regular gasoline, could provide meaningful relief at the pump, an increasingly urgent political concern for Republicans heading into November midterms. Opposition has come primarily from refining-state lawmakers in Texas and Oklahoma and smaller refiners, who warn that the bill tightens EPA biofuel blending exemptions and raises compliance costs. The Congressional Budget Office estimates the legislation would add approximately $2.3 billion to the deficit over the next decade. Farm groups welcomed the potential demand boost for corn, though the American Soybean Association cautioned the policy could shift planting incentives away from soybeans at a time when corn output is already projected to fall roughly 6% from last year. The NYMEX RBOB crack spread chart places the legislative backdrop in sharp context: the 2026 crack (black) surged from around 17 cents/gallon in January to a peak near 65 cents by late April before pulling back to around 48 cents, a level that still dwarfs 2024 and 2025 comparable periods and underscores that price relief has become a top political priority.

Wild Card

Source: Fundamental Analytics

Source: International Air Transport Association

Rising Jet Fuel and Ticket Prices Could Disrupt Summer Air Travel

Tsvetana Paraskova, OilPrice.com

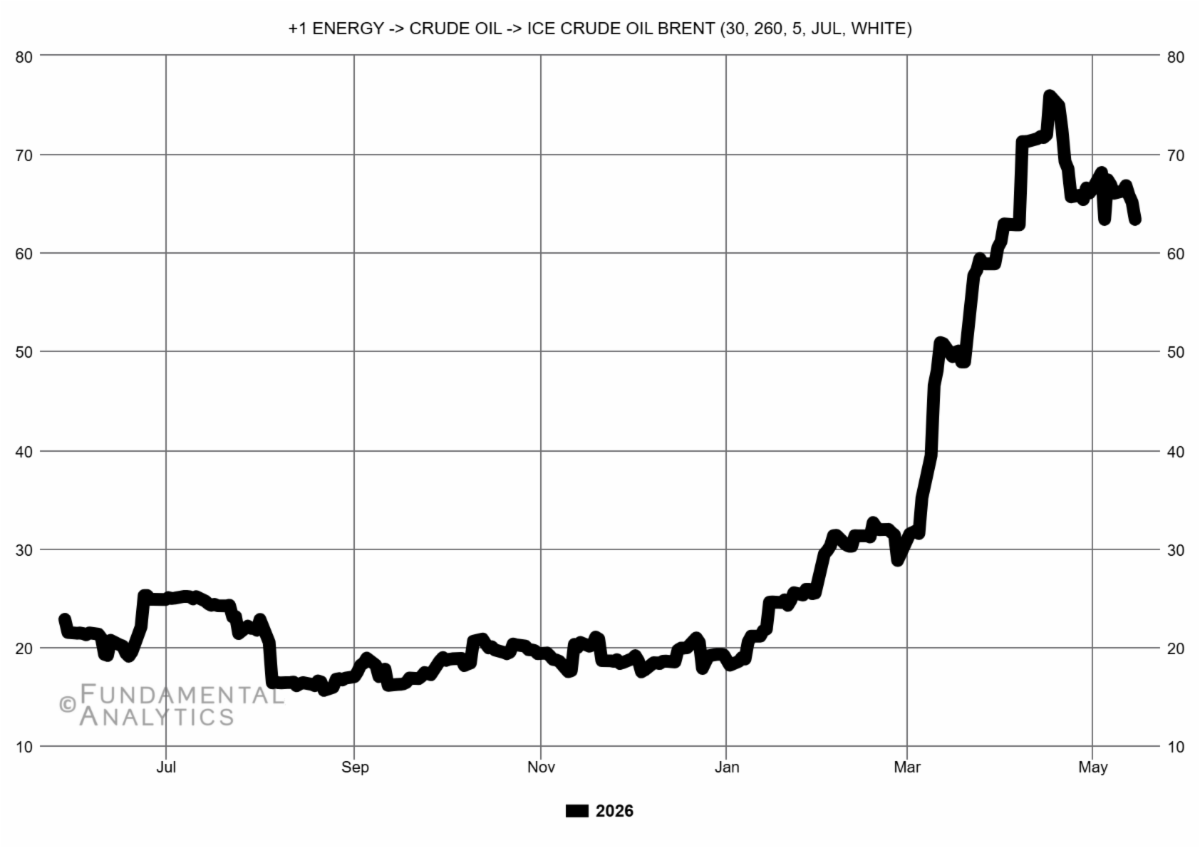

The Strait of Hormuz closure has sent global jet fuel prices above $200/barrel in April before easing to around $150 in May, still roughly double pre-war levels, as Middle Eastern exports stalled, and Asian refiners cut shipments to protect domestic supply. The IEA warned Europe had weeks of supply remaining, though the industry’s primary concern has since shifted from outright shortage to sustained price pain, with Lufthansa flagging an additional $2 billion in fuel costs this year and airlines increasingly passing costs to passengers or canceling unprofitable routes. The two charts capture the shock in context: the Brent crack spread surged from a stable $18–20/bbl through most of 2025 to nearly $76/bbl at peak, while the global jet fuel price chart shows the same violent rupture, two years of $80–100/bbl pricing obliterated by a near-vertical spike, illustrating how disproportionately jet fuel has borne the brunt of this supply disruption relative to crude oil itself.

Trading Implications

The Strait of Hormuz closure remains the dominant variable across the entire energy complex, and the key trading question is the same one markets have been wrestling with for weeks: how quickly prices could unwind if a ceasefire materializes. Crude’s backward dated futures curve is being misread by some as a price forecast, but as analysts noted this week, it reflects physical tightness and hedging behavior rather than trader conviction, meaning a reopening of the Strait could trigger a swift and disorderly selloff that catches leveraged longs off guard. In LNG, the U.S. has structurally cemented itself as Europe’s dominant supplier, a relationship unlikely to reverse even post-conflict, supporting longer-term Henry Hub demand. Gasoline’s crack spread has already pulled back sharply from its April peak, and the E15 legislation, if it clears the Senate, could provide incremental demand relief at the pump while simultaneously boosting corn markets. Jet fuel remains the most stressed barrel in the complex with prices still near $150/bbl after retreating from $200. Aviation-exposed equities and route-dependent carriers face continued margin pressure through the summer travel season regardless of how the geopolitical situation evolves.