Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s agriculture topics include:

- Corn: July corn gave back nearly 10 cents of gains on May 20 as the post-China trade deal rally stalled and investors wait for confirmed export demand.

- Soybeans: Despite bearish near-term price pressure, CBOT soybean open interest in 2026 is running at historically elevated levels.

- Wheat: July wheat closed near key technical support as funds exited record long positions, though rising open interest alongside the YTD price rally confirms the broader move was built on genuine participation.

- Wild Card: NOAA has upgraded the probability for a strong-or-greater El Niño to 67%, with JPMorgan warning an event could deliver a material global inflation shock.

Let’s begin.

Corn

Source: Fundamental Analytics

Corn and Soybeans Close Down Nearly 10 Cents

Cassidy Walter, SuccessfulFarming

CBOT July corn closed down 9 ½ cents at $4.65 on May 20, giving back a portion of gains accumulated over the prior two months as a weaker energy complex, favorable weather, and slowing US export competitiveness weighed on the market. Karl Setzer of Consus Ag Consulting noted that the US is “rapidly becoming less competitive on corn” in global markets, with elevated transit costs increasingly factoring into trade flows. The session’s weakness following a telling price action signal visible on the chart: after a steady climb from around $4.30 in February to a high near $4.80. The market gapped lower on May 19 in the wake of the US-China trade deal announcement over the weekend of May 17 following the Trump-Xi meeting. While the deal initially provided a broad boost to grains and oilseeds, Arlan Suderman of StoneX captured the market’s subsequent consolidation well, traders are now in a “waiting game” to see which commodities benefit from the confirmed purchase commitments before extending the rally. The chart reflects this dynamic clearly: a constructive two-month uptrend punctuated by a sharp, post-announcement pullback, suggesting the market had already priced in optimism ahead of the deal and is now demanding concrete export demand before making another leg higher.

Soybeans

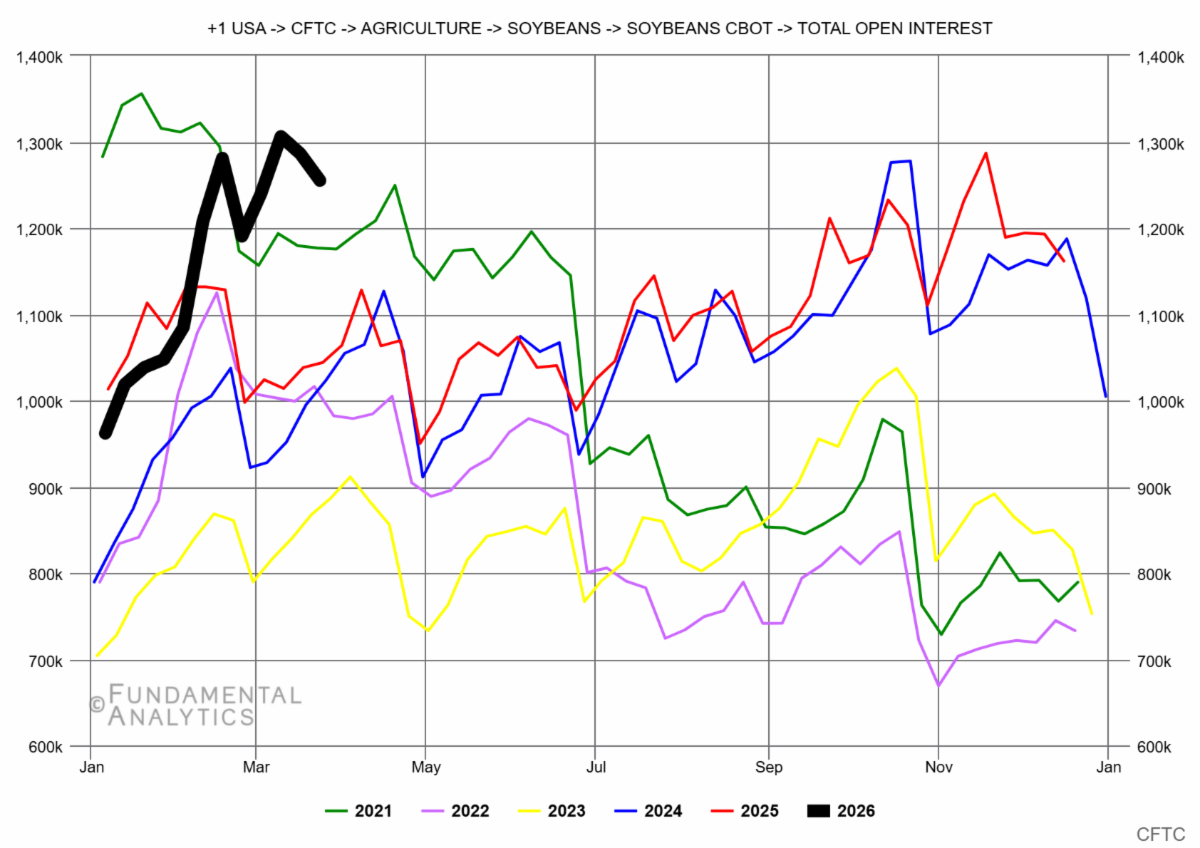

Source: Fundamental Analytics

Soybeans Slipping on Wednesday, on Outside Pressure

Austin Schroeder, Barchart

July soybeans closed down 9 ¾ cents at $11.99 on May 20, with similar pressures from the weakening energy complex. The US continues to face a structural competitiveness problem in global soy markets as well. Brazil’s Abiove raised its 2026 export estimate to 114.1 MMT from the US, reinforcing South America’s dominant position as the world’s largest soybeans buyer. Thursday’s USDA export sales report will be a likely near-term catalyst, with analyst estimates ranging from 150,000-450,000 MMT for old crop, a wide band that reflects genuine uncertainty about whether the US-China trade deal is translating into confirmed purchase commitments. What makes the current environment particularly notable, however, is what the open interest chart revels. Despite the bearish price pressure, CBOT soybean total open interest in 2026 (black line) has surged to approximately 1.25-1.3 million contracts through late February and March, comfortably above every comparable prior-year period going back to 2021. That level of market participation amid a consolidating price environment signals that traders are not abandoning the soybean complex but rather accumulating positions, likely reflecting ongoing uncertainty around the China trade relationship, Southeast Asian biofuel demand, and the eventual resolution of the Iran conflict’s effect on freight and vegetable oil spreads.

Wheat

Source: Fundamental Analytics

Grains Fall on Pre-Holiday Profit Taking

Michelle Rook, AgWeb Farm Journal

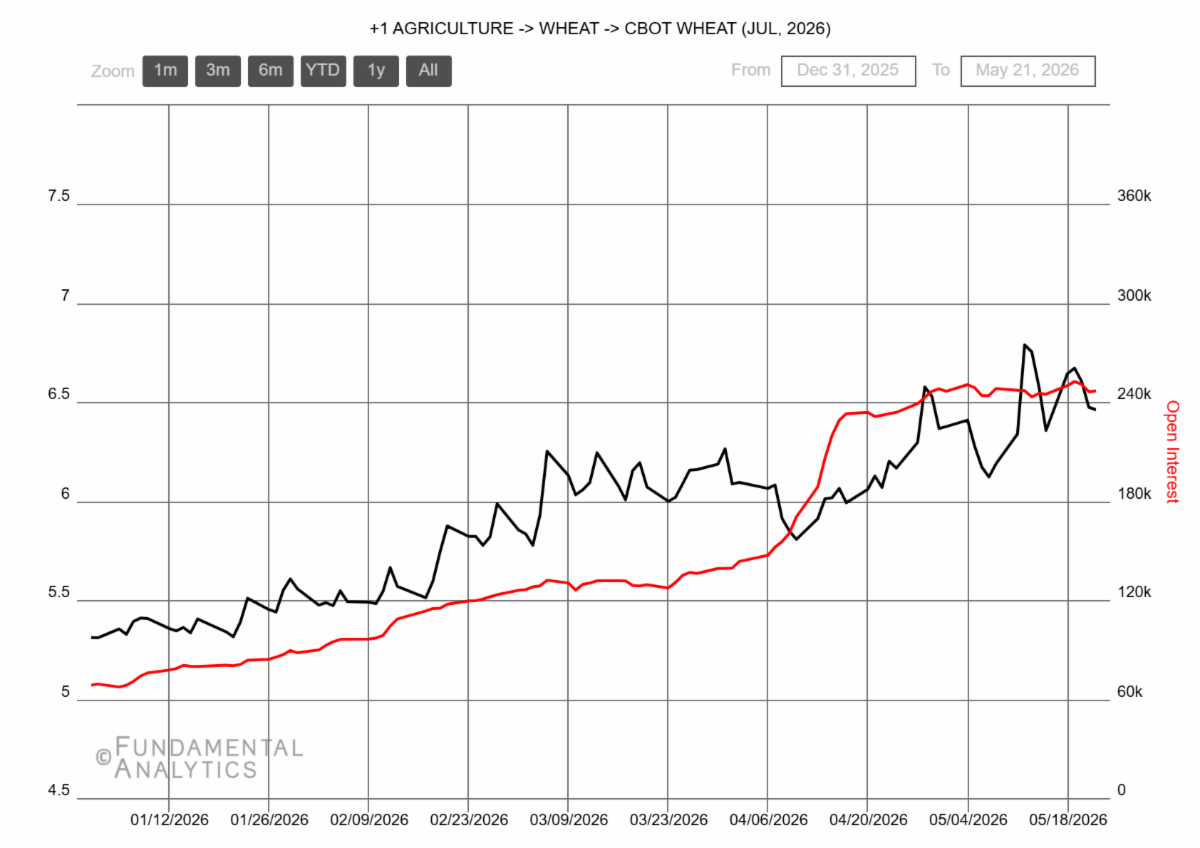

July CBOT wheat closed down 6 ¾ cents at $6.60 on May 20, pressured by profit taking ahead of the three-day Memorial Day weekend, fund liquidation, and the disappointment over China’s lack of confirmed agricultural purchases. Naomi Blohm of Total Farm Marketing noted that wheat put in its highs immediately after the May WASDE report shocked traders with the lowest US winter wheat crop since 1972, and the market has since been digesting that bullish news while battling a seasonal tendency to sell off this time of year. Funds that entered the China summit near a record combined grain long, comparable only to positioning seen after the Russia-Ukraine war, have been systematically exiting, and Blohm noted they are now moving short in wheat. Near term, she sees the path of least resistance as sideways to lower unless a weather scare, or Middle East escalation provides a fresh catalyst. Longer-term views, however, turns more constructive: Australia and Canada are already projecting lower acreage for 2027, fertilizer cost pressures are rippling through global planting decisions, and she notes that “wheat always leads those big rallies.” The chart reinforces the bifurcated story well – CBOT July futures (black) climbed steadily from around $5.20 in early January to a peak above $6.50 in early May. Open interest (red) rose in near lockstep from roughly 65k to 240k contracts, confirming that the rally was built on genuine and expanding market participation rather than thin speculative positioning.

Wild Card

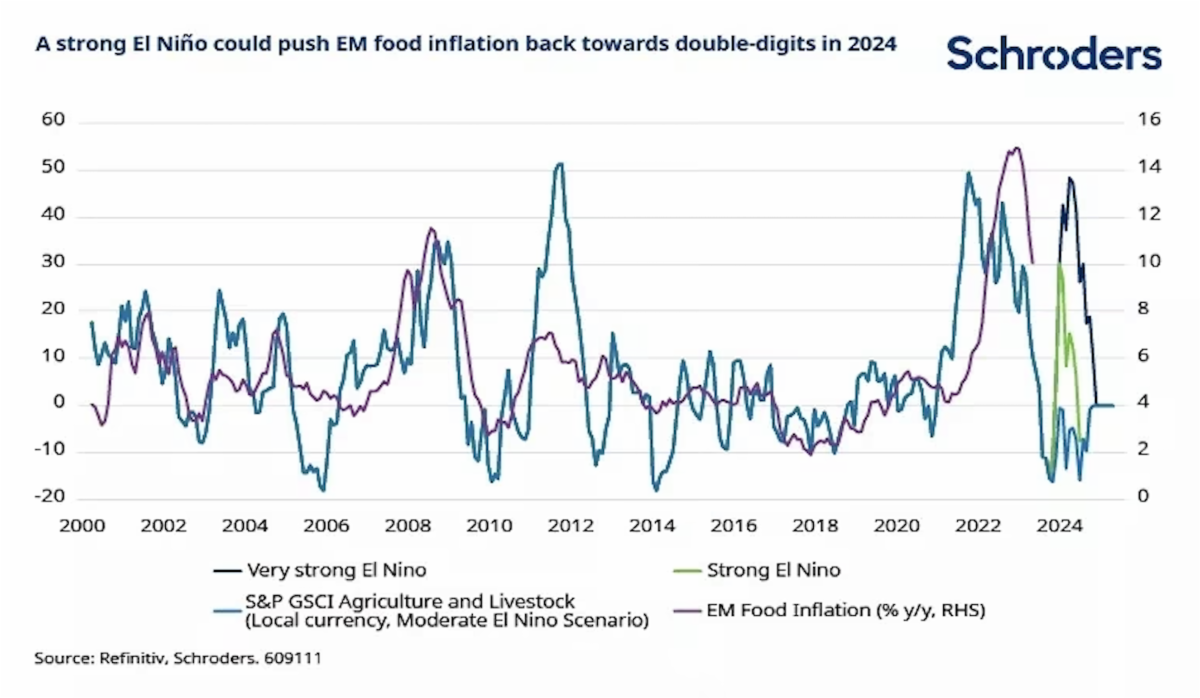

Source: Schroders

Kraken El Niño is Coming for the Crops

Bryce Elder, Financial Times

The National Oceanic and Atmospheric Administration is now forecasting a warming phase in the tropical Pacific by July with near certainty, and JPMorgan analyst Diego Pereira is flagging a meaningful shift in the probability distribution. The odds of a strong-or-greater event have jumped from 51% to 67% over the past month, with a so-called “Kraken El Niño” comparable to the historic 2015-2016 episodes. JPMorgan’s own modeling warns a Kraken event could produce a material region-wide inflation shock, with peak effects emerging in the second half of the year and inflation pressures typically peaking four to eight months after first impact, meaning consequences would bleed well into 2027. The agricultural implications are asymmetric and geography dependent. Argentina’s Pampas could see improved soybean, corn, and wheat yields from increased rainfall, a relative winner, while Brazil faces to opposite risk of floods in its agricultural south and drought threatening its northern hydroelectric capacity. Colombia’s coffee and hydropower, Peru and Ecuador’s coastal agriculture, West African cocoa, and rice yields in Southeast Asia all represent meaningful tail risks. The chart draws from 2024 data but remains instructive in illustrating how a strong El Niño can correlate with food price inflation approaching double digits. A scenario layered on top of already elevated energy prices and supply disruptions, would present a compounding challenge for central banks already navigating a difficult inflation environment.

Trading Implications

The China trade deal, which funds had positioned for aggressively going into the summit with near record combined grain longs, has so far failed to deliver confirmed purchase volumes, triggering systematic long liquidation across corn, soybeans, and wheat heading into the holiday weekend. The key near-term question is whether China steps in to buy at harvest-low prices in August and September, as some analysts expect, or whether the absence of near-term demand flow breaks key technical levels, $4.75 December corn and $11.75 November beans, and opens the door to a deeper correction. Wheat’s longer-term setup is arguably the most interesting: open interest climbed in lockstep with prices all year, confirming genuine market conviction behind the rally, and with Australia, Canada, and several other producers already flagging lower 2027 acreage and fertilizer cost pressures rippling globally, the stage may be setting for wheat to lead the next leg higher. Layered on top of this is the El Niño wildcard, with JPMorgan now modeling a 37% probability of a Kraken event capable of producing double-digit food inflation, commodity markets may be significantly underpricing the tail risk of a synchronized weather, energy, and supply shock converging in the second half of 2026 and into 2027.