Brent whipsawed on Hormuz reopening hopes versus renewed strikes and softer China demand. Gasoline stayed supported by persistent inventory draws and export pull. Natgas firmed on a smaller injection and early heat.

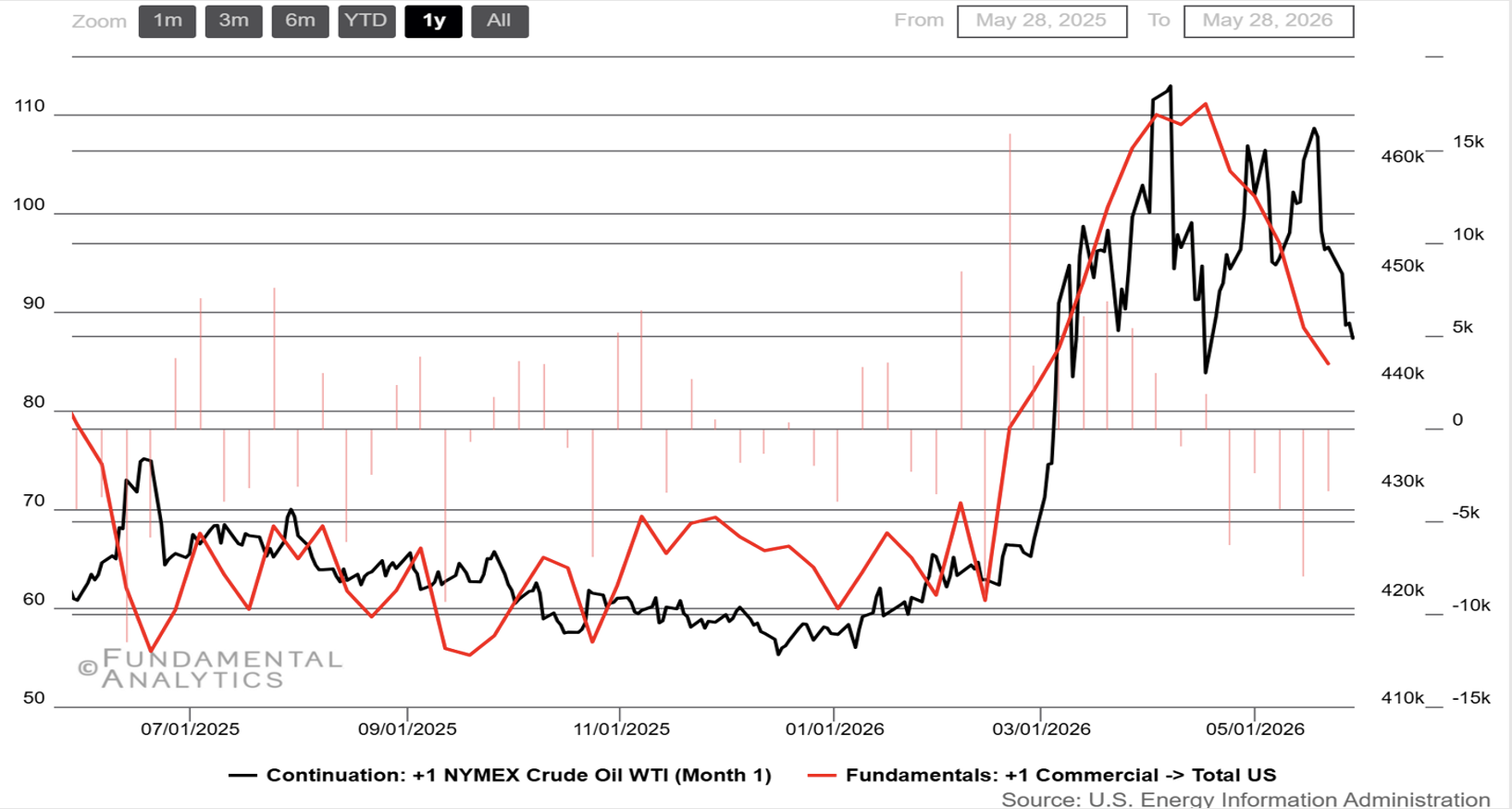

Crude Oil

WTI fell below $90 mark as ceasefire hope amplify

- Ceasefire “framework” optimism repeatedly deflated the war premium: reports of a draft U.S.–Iran understanding and talk of reopening the Strait of Hormuz triggered sharp selloffs (including a ~5% Brent drop at one point), with follow-up headlines showing key terms still unresolved.

- Renewed U.S.–Iran strikes rebuilt the risk premium fast: fresh exchanges and broader regional escalation (including Israel’s Lebanon front) pushed Brent back higher as traders re-priced supply interruption risk and mine threats around Hormuz.

- Supply fears dominated even as demand signals softened: Reuters reporting explicitly noted that “supply concerns” from the conflict outweighed weak macro data, keeping Brent headline-driven rather than purely balance-sheet driven.

- China’s import response signaled economic triage, not demand strength: China’s seaborne crude imports slumped to multi-year lows as refiners leaned on inventories and optimized product output—supportive for regional balances, but a bearish demand read-through for Brent at the margin.

- Month-end positioning amplified the move lower: Brent and WTI posted their steepest monthly declines since March 2020, underscoring how quickly “deal hopes” can overwhelm disruption pricing when traders believe physical constraints may ease

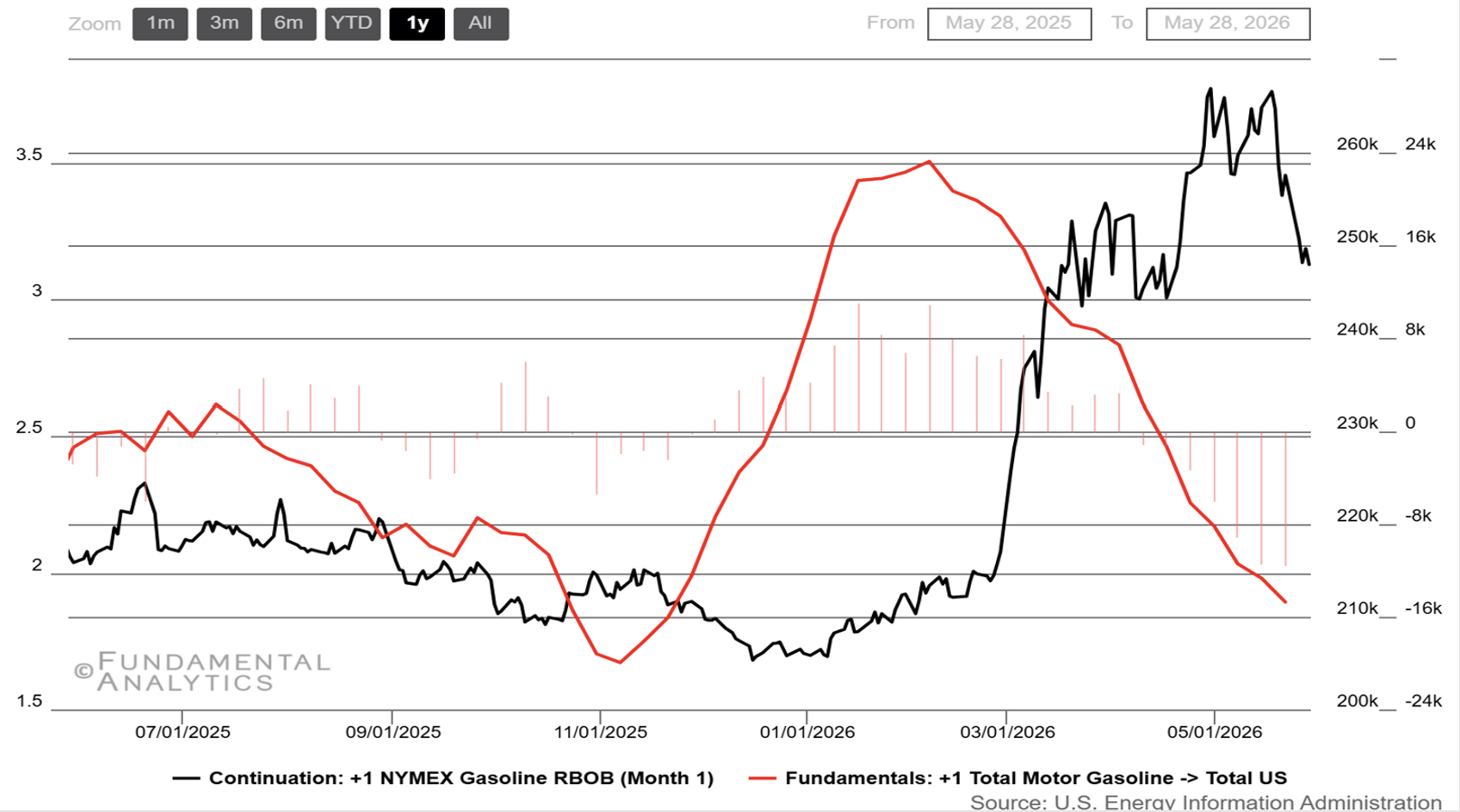

Gasoline

Gasoline futures decline to a one-month low, Inventory significantly depletes

- Buffer erosion became the story: U.S. gasoline stocks extended a near-record drawdown streak, leaving inventories around 211.5m bbl and roughly 5.5% below the seasonal 5-year average—raising sensitivity to any supply hiccup as summer demand ramps.

- Weekly EIA print stayed outright supportive: for the latest reported week, total motor gasoline inventories fell ~2.6m bbl and remained ~6% below the 5-year average, even as gasoline production ran near ~9.9 mb/d and utilization jumped to ~94.5%.

- Demand improving, but not “boom” strong: four-week motor gasoline product supplied averaged about ~8.9 mb/d, only slightly below last year—tight enough to keep draws going, not strong enough to justify runaway pricing on demand alone.

- Refinery response risk: more runs, but barrels may not stay domestic: refiners lifted crude processing to the highest since November (per Reuters), yet the incentive to export into higher international prices risks limiting how much incremental supply rebuilds U.S. inventories.

- Geopolitics rewired product flows and freight, keeping a risk premium live: near-total Hormuz disruption slashed crossings (~88% drop vs pre-conflict) and tightened global refined-product logistics, supporting U.S. gasoline via higher freight/arbitrage and export pull.

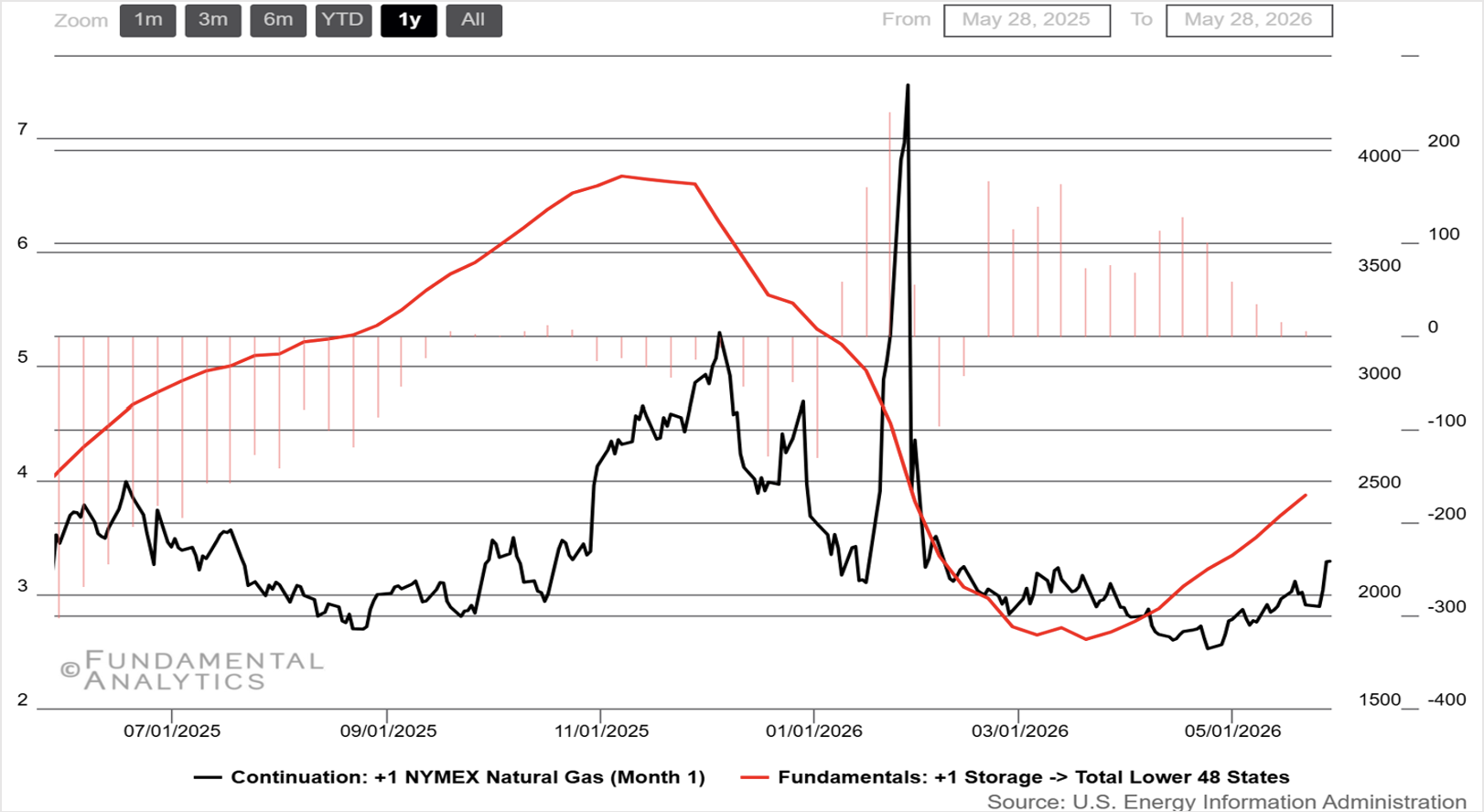

Natural Gas

Natural Gas soar on hotter than expected forecasts

- Storage print tightened the near-term balance: EIA reported a 92 Bcf injection (below typical seasonal builds), lifting working gas to ~2,483 Bcf and trimming the storage surplus—supportive for the front month.

- Early heat risk revived power-burn demand: forecasts of hotter conditions into June underpinned expectations for stronger gas-fired generation, pushing futures to multi-week highs before some profit-taking.

- Exports remained the key demand floor, but maintenance muted the marginal bid: LNG feedgas stayed structurally high, yet scheduled liquefaction maintenance temporarily reduced export-pull versus April’s record pace.

- Supply stayed resilient (cap on runaway rallies):S. gas production remained elevated in monthly data (with Texas at a record), keeping the market sensitive to any demand disappointment once weather premiums fade.

- Geopolitics lifted volatility and hedging demand more than “physical” U.S. tightness: Hormuz disruption continued to reroute global LNG flows and drove record open interest in gas/power derivatives—supportive for risk premia even with comfortable U.S. inventories.