Mid-Week, Weekly Review of Gold, Silver, and Palladium

October 28, 2020

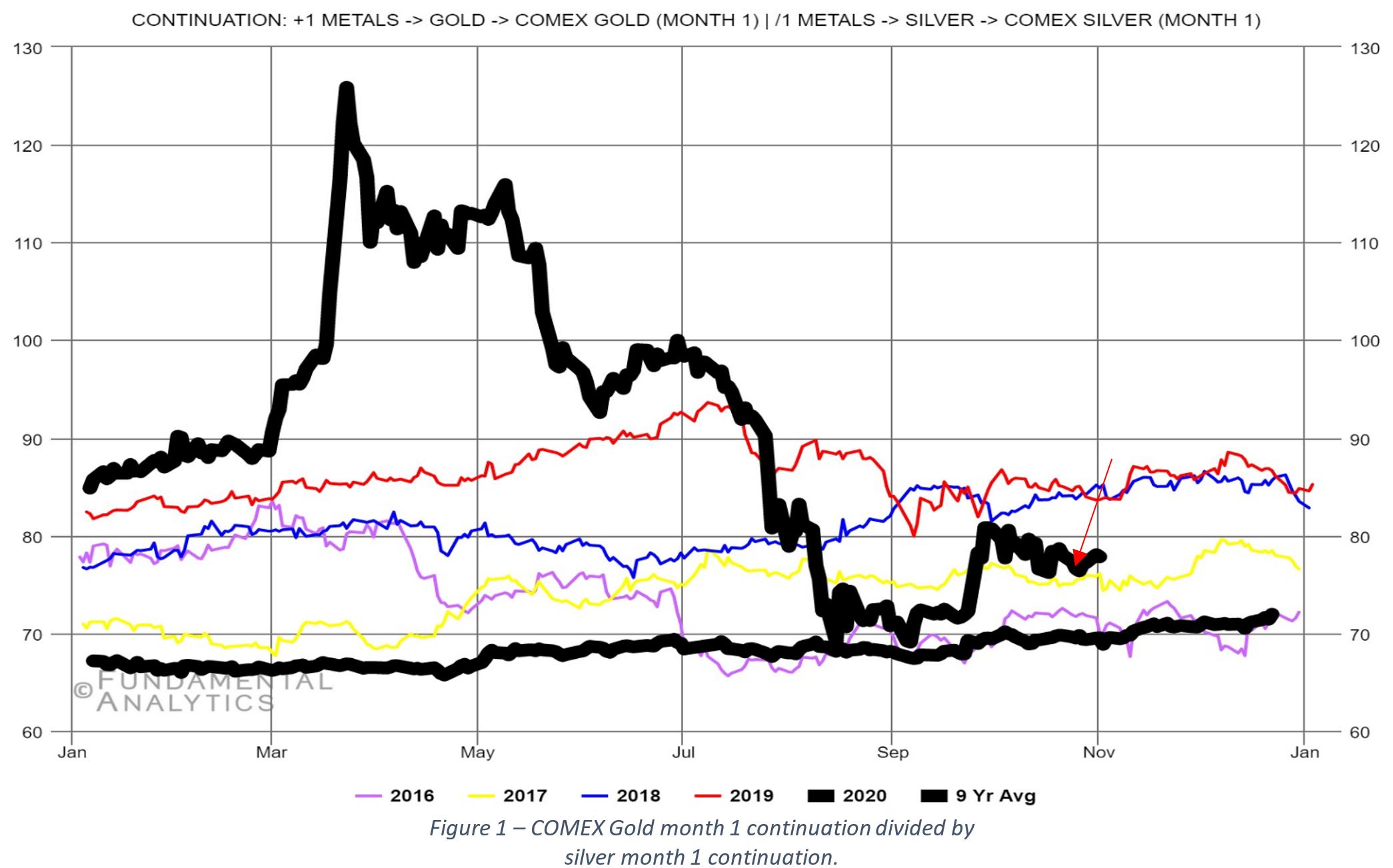

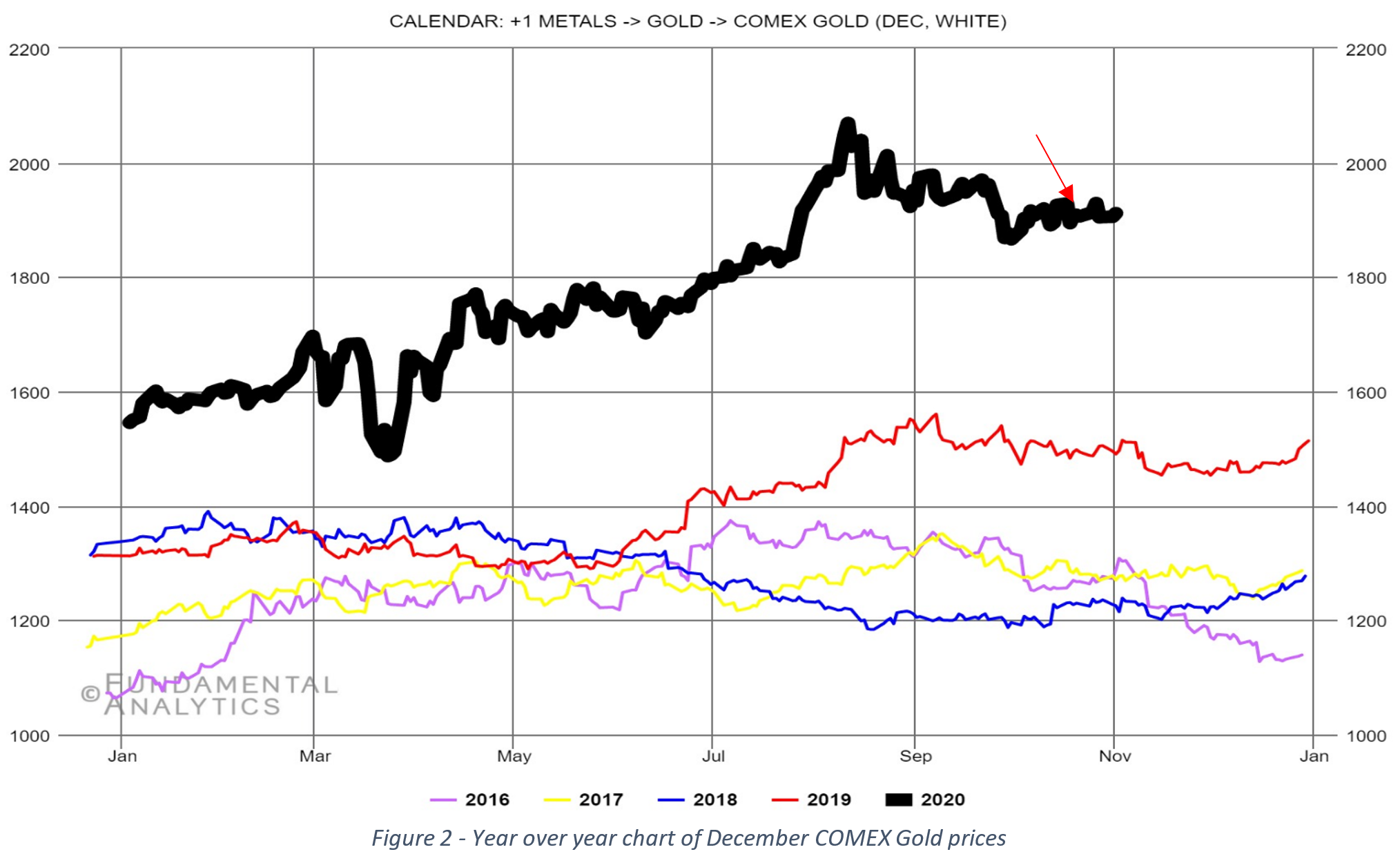

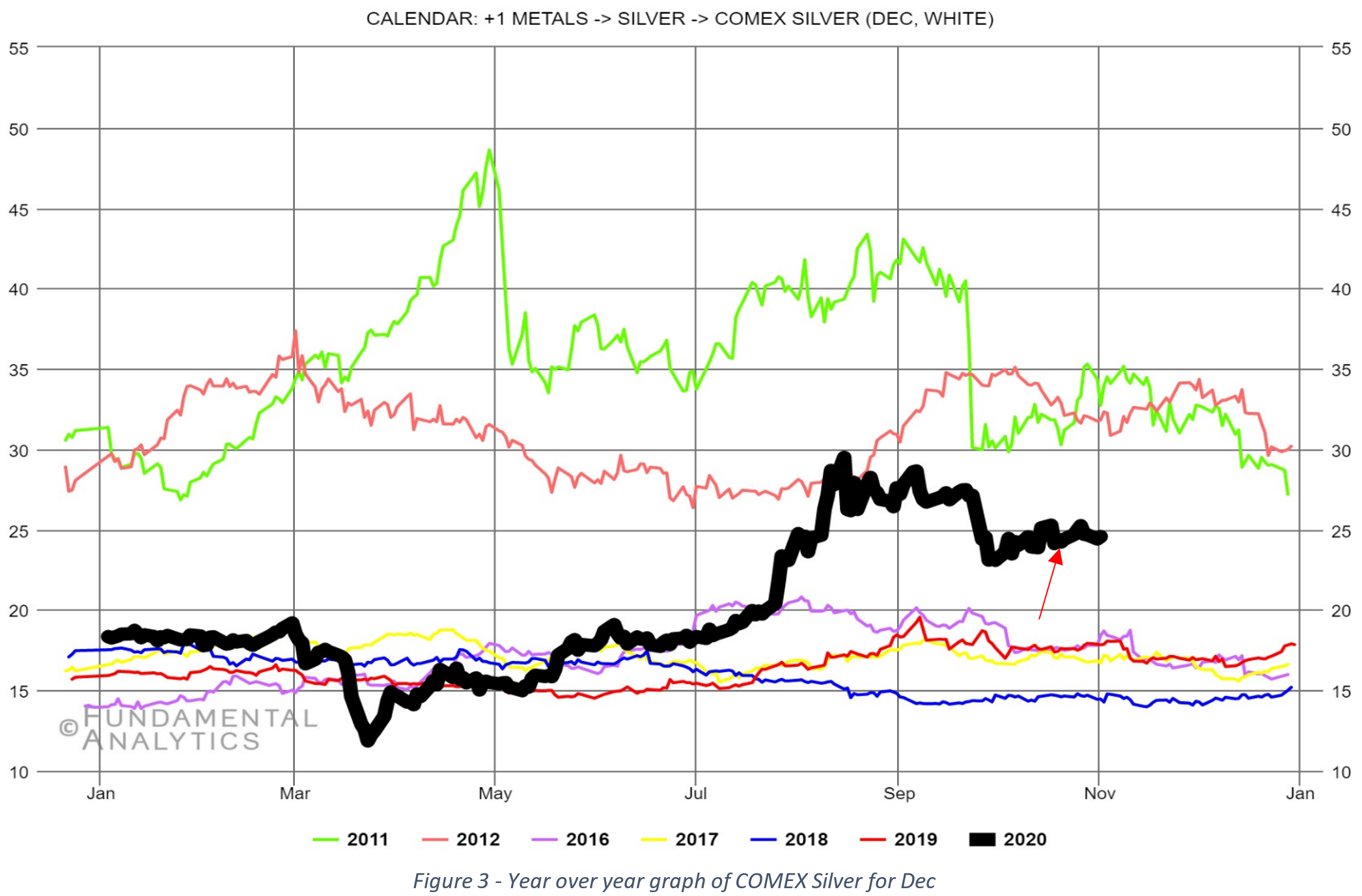

Prices for precious metals are down today, as partial lockdowns are implemented in Europe and record cases of Covid-19 are reported in the US and Europe. Demand for ICU beds is rising which exacerbates the fear that a second wave is taking hold in the US and Europe. Prices are pressured as liquidity demand increases given the market downturn, and especially as margin calls may be coming in. Such downward pressure on the precious metals might continue as market turmoil and volatility are rising. They should stabilize within 6-9 trading days and they have good chances of moving upwards from then on. The front month contracts for gold and silver were all down from the close on October 20, 2020, with gold and silver down 0.08% and 1.65%, respectively (red arrow identifies close on the 20th). The ratio of the month 1 Gold contract to the month 1 Silver contract (Figure 1) is up 1.59% compared to the close on the 20th. Since the end of September, the gold/silver ratio is descending, which tends to be positive for gold. With the front month gold and silver contracts closing yesterday at $1908.80 and $24.53, respectively, the gold/silver ratio is now 77.83, 17.6% higher than the corresponding 15-year average. December gold (Figure 2) closed yesterday at $1911.90, down 0.18% and December silver (Figure 3) closed at $24.57, down 1.64% from the close on October 20th.

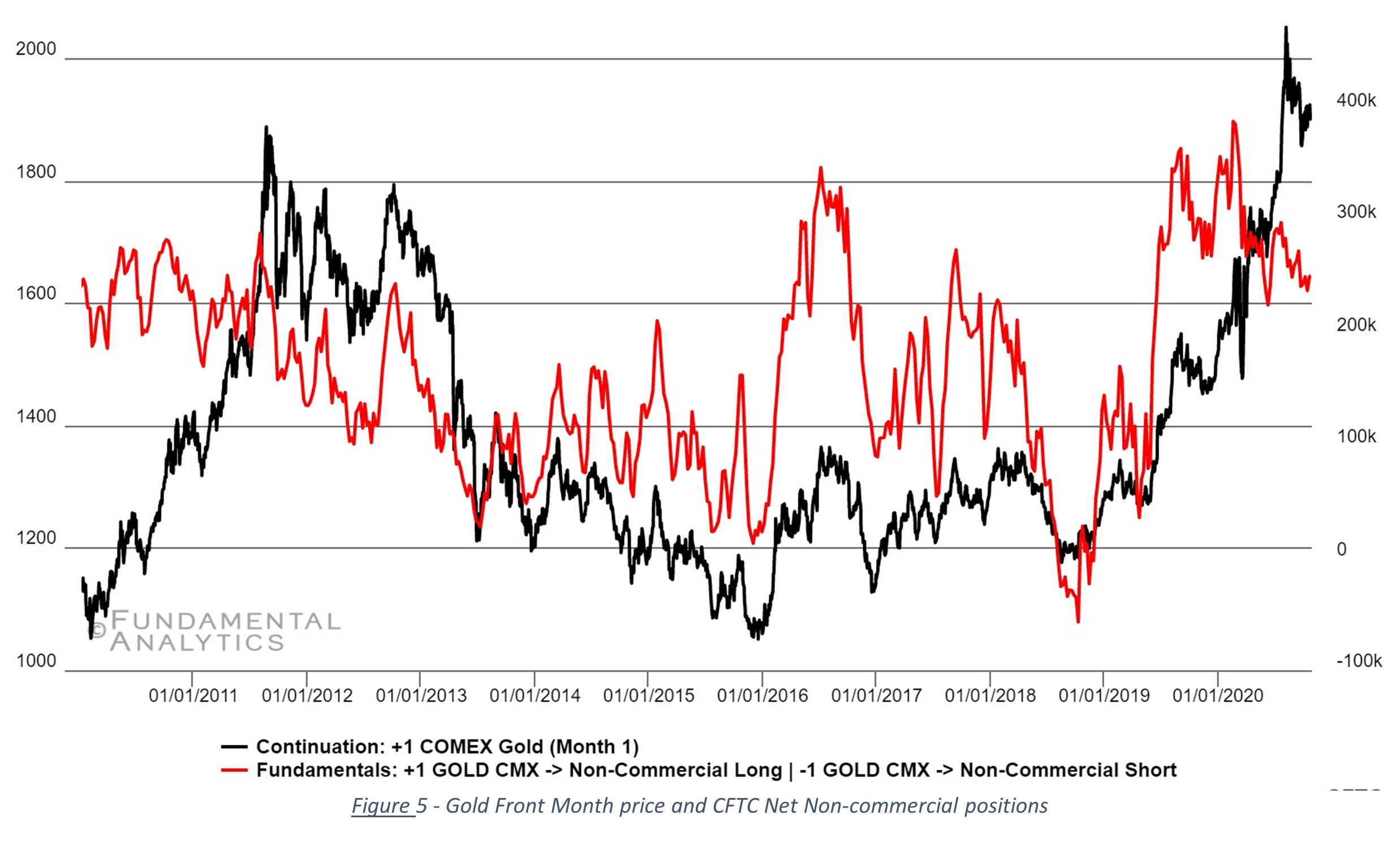

From an open interest perspective, gold’s total open interest has seen little movement over the last few weeks while its volume 50-day SMA continues to decline. The latest CFTC report for gold (10/20) for non-commercial net position of funds show funds net long positions rose 5.3% from the previous week’s report, but this move brings the net fund position back to a level seen in the October 6th report. From a longer-term perspective (since the end of July) the non-commercial funds continue to build their short positions, resulting in a gradual reduction in the number of net-long positions. Since the end of July non-commercial long positions decreased 8% while short positions increased by 27%. Now on to silver… Silver total open interest continues to slowly rise since the recent low at the end of September. Likewise, the latest CFTC data (10/20) show the silver non-commercial net positions also continue to rise, up 8.7% from the previous report. Since the August 11th CFTC report, the non-commercial funds have increased their net long positions by 12% at the same time reducing their short positions by 23%. It should be noted, this is opposite to how the funds are positioning their gold positions. At first glance one might think this means the non-commercial funds are preparing for lower gold prices. But with non-commercial fund gold net long positions near historic highs throughout 2019, they may be bringing the net long positions back in line with historic averages as seen in Figure 5.

Now for Palladium. December Palladium closed at $2353.90 yesterday, down 2.64% from the close last week Tuesday. Total open interest continues to slowly rise, up 4.9% from Tuesday last week. The Oct 20th CFTC report shows an increase of 0.8% in non-commercial net fund positions. As we have discussed palladium tends to follow the price of rhodium due to similar uses in catalytic converters in gasoline powered engines. As rhodium price rises, lower priced palladium is substituted for rhodium, increasing palladium demand, and thus keeping upward price pressure on the metal. With recent news of additional shutdowns, due to COVID across the US and Europe, this may put downward pressure on both metals over the next few weeks.

The final thought I leave with you today is a regarding the price of palladium. Michael A. Gayed, CFA wrote an article and published through Seeking Alpha on October 19th. Even though the article was published 9 days ago, it contains a good summary of potential upside and risks for palladium for the next few years. The article can be found here. In summary, he continues to see a long-term demand-supply mismatch, with demand larger than supply. Palladium demand is being driven by European consumers continuing to switch from diesel to gasoline powered vehicles, the introduction of RDE tests in Europe and increased exhaust standards in China. The risks (lower demand and more supply, but longer term) may be driven by newer lower priced materials to replace palladium and potentially new deposits of the metal.

If you would like access to the great insights and analysis provided by the Fundamental Analytics platform, sign up for a 15-day free trial and demonstration!

If you have any questions, please contact our Technology Manager, Mike Secen at mike.secen@fundamentalanalytics.com

We also invite you to read our other articles and follow us on social media!

Best Regards,

The Fundamental Analytics Team

The information provided here is for general informational purposes only and should not be considered individualized investment advice. All expressions of opinion are subject to change without notice in reaction to shifting market conditions.