Fundamental Analytics Team

Welcome to our weekly Commodity News Roundup, a curated newsletter featuring concise summaries of developments in the agriculture and energy commodities markets—along with direct links to the full articles and related charts from the Fundamental Analytics platform. Our goal is to give you a quick, insightful overview of the latest market drivers and spark your interest to explore the full stories.

This week’s energy topics include:

- LNG: U.S. natural gas prices edge modestly higher despite mounting storage surpluses, underscoring a well‑supplied market with weakening downside momentum but no clear catalyst for a sustained rally.

- Crude Oil: Near‑closure of the Strait of Hormuz triggers a historic supply shock, driving oil above $100/bbl and creating extreme backwardation as physical barrels trade at unprecedented premiums.

- Gasoline: California gasoline inventories fall to record lows as Hormuz disruptions tighten global supply chains, pushing state prices sharply higher and leaving the market vulnerable to further import declines.

- Wild Card: Brazil’s extensive biofuels infrastructure cushions the domestic impact of the global oil shock, highlighting structural resilience and a potential model for reducing exposure to fossil fuel volatility.

Let’s begin.

LNG

Source: Fundamental Analytics

U.S. Natural Gas Futures Settle Higher

Wall Street Journal

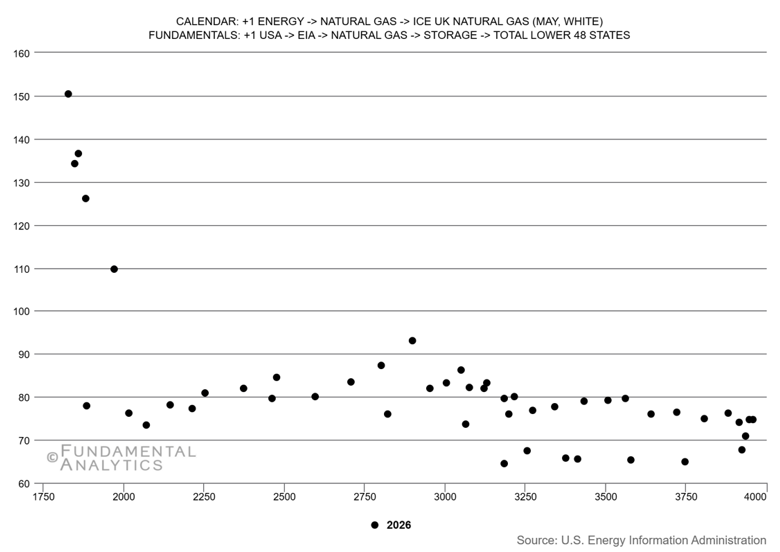

U.S. natural gas markets are showing signs of oversupply and muted price momentum as storage levels continue to build beyond seasonal norms, with inventories rising by 51–59 Bcf in recent reports and the surplus widening to roughly 100 Bcf above the five-year average. Despite these bearish fundamentals and mild spring weather limiting both heating and cooling demand, prices have only modestly increased to around $2.64/mmBtu, suggesting the market may be losing downside momentum but lacks a catalyst for a sustained rally. This dynamic is reinforced by the chart above, where elevated storage levels consistently align with subdued price ranges, indicating ample supply and weak pricing power. With injections expected to accelerate in the coming weeks, the absence of strong upward price movement points to a well-supplied market likely to remain rangebound unless demand conditions shift materially.

Crude Oil

Source: Fundamental Analytics

Why Oil Futures Are Trading Way Below Real-World Prices

Lucia Kassai, Bloomberg

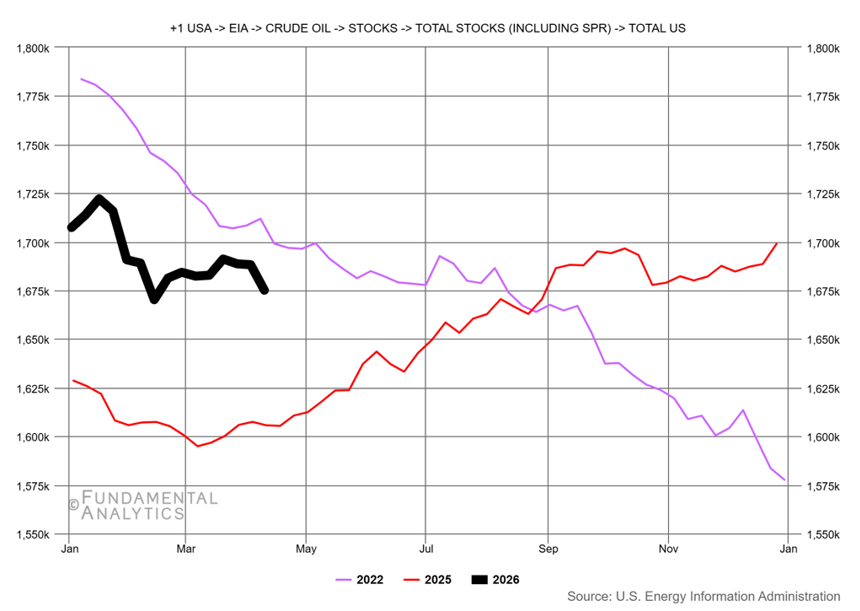

The near closure of the Strait of Hormuz has triggered a historic oil supply shock, disrupting roughly 20% of global crude flows and pushing prices above $100 per barrel, up nearly 30% since the start of the Iran conflict, with some forecasts warning of a potential surge to $200 if disruptions persist. Markets are exhibiting extreme backwardation, with physical crude trading at an unprecedented ~$30 premium to near-term futures versus a typical gap of under $2, reflecting urgent demand for immediate supply even as traders remain cautious about longer-term price sustainability. The disruption has led to refinery cutbacks in parts of the Middle East, supply shortages across Asia, and rising input costs globally, while US refiners remain relatively insulated but still face higher crude prices. For consumers, the shock is feeding directly into inflation, with US gasoline prices exceeding $4 per gallon and broader increases across transportation, food, and energy-linked goods, highlighting the wide economic spillover of the supply crunch.

Gasoline

Source: Fundamental Analytics

California gasoline stocks fall to record lows as Hormuz disruption bites

Nicole Jao, Investing.com

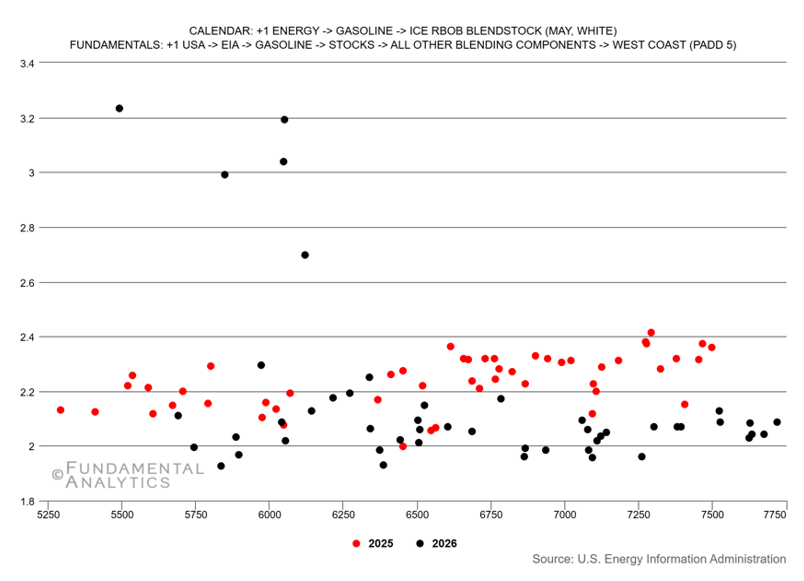

California gasoline markets are tightening sharply as the Iran conflict disrupts global supply chains, with statewide inventories falling to a record low of 9.44 million barrels and prices rising to $5.86 per gallon, about 26% higher since the start of the war and well above the $4.09 national average. The state is particularly vulnerable due to its reliance on imported refined products from Asia, which in turn depend on Middle Eastern crude transiting the Strait of Hormuz, through which roughly 20% of global oil flows. Analysts warn the full impact has yet to materialize, as shipping delays mean a sharper drop in imports is expected within one to two weeks, potentially further tightening supply and pushing prices higher. Structural factors, including refinery closures and a decline in state crude inventories, now down over 23% year over year, are compounding the risk, even as officials attempt to source alternative supplies and downplay immediate shortages.

Wild Card

Source: Grandview Research

Brazil has a secret weapon against oil shocks

The Economist

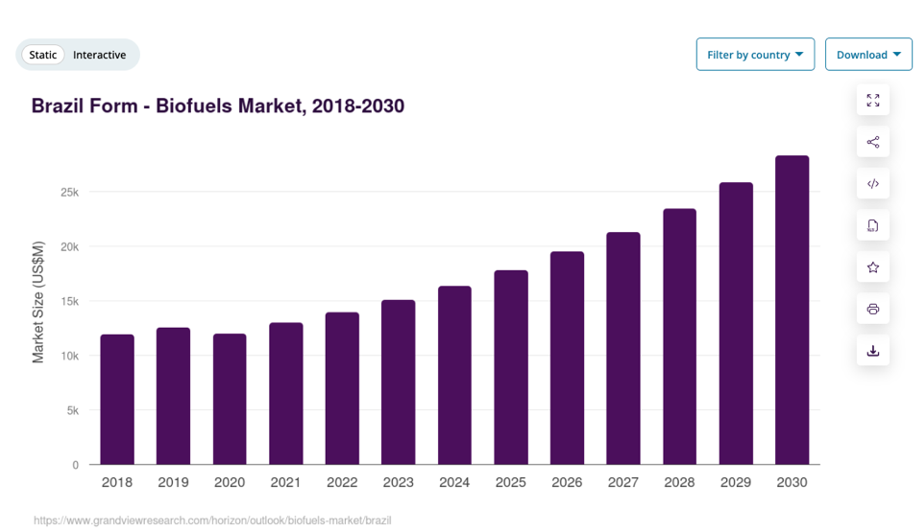

Brazil has been relatively insulated from the global oil shock caused by the Iran conflict due to its highly developed biofuels sector, which blends roughly 30% ethanol into gasoline and 15% biodiesel into diesel, supported by widespread flex-fuel vehicle adoption. As a result, fuel price increases have been more moderate, with gasoline up about 10% and diesel 20%, compared to 30–40% spikes in the United States, aided by both biofuel competitiveness and efforts by Petrobras to absorb some costs. Biofuel economics are improving further, with biodiesel now cheaper than imported diesel and ethanol prices rising only marginally, while upcoming harvests of soybeans, sugarcane, and corn are expected to boost supply and potentially lower prices. This long-standing strategy, rooted in energy security policies dating back to the 1970s, is now positioning Brazil as both more resilient to energy shocks and a potential model for other countries seeking to reduce dependence on volatile fossil fuel markets.

Trading Implications

Natural gas looks set to stay rangebound, with high storage levels and rising injections limiting upside and no clear catalyst to drive prices meaningfully higher. In contrast, oil markets are signaling acute near-term tightness, making front-month crude and time-spread longs more attractive, while deferred prices carry higher risk if disruptions ease. Gasoline, especially in California, remains the most bullish segment, supporting strength in regional basis and crack spreads as inventories continue to fall. Longer term, Brazil’s biofuel buffer highlights relative resilience to oil shocks, favoring selective relative-value trades versus more import-dependent markets.