Dr. Ken Rietz

The beginning of a new year is traditionally a time of both retrospection and prospects. For crude oil, we will examine various aspects that occurred in the past year in order to assemble a forecast for 2026. We begin with two graphs, the price and stocks of global crude oil.

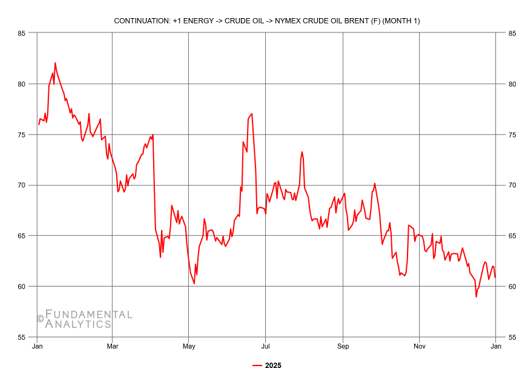

Figure 1: Front-month futures for NYMEX Brent crude, 2025

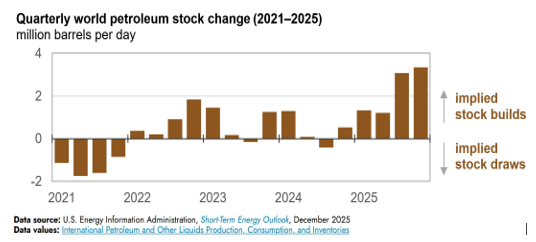

Figure 2: Changes in global stocks of crude oil over the past several years

These two graphs give a summary of what the crude oil prices were during 2025 and why. The prices were in a jagged downtrend all year, and the simplest reason is that the stocks were increasing. Indeed, January 1 Brent crude prices have been falling for three years. But as the EIA points out, the stocks in China are more likely to act as removing crude oil from global use. So, China’s importing oil both decreases supply and increases demand. That moderated the decline in the price of crude oil during 2025. While geopolitics would take us too far away from the current topic, it should also be noted that this general trend is not good news for Russia.

But all that extra crude oil has to go somewhere, and this amount of oil at this rate makes you wonder where. With production larger than consumption, storage for either crude oil or its products is filling up storage units. Forbes gives a May 2025 estimate of global available land storage of 0.9 to 1.8 billion barrels, and a detailed explanation of why there is so much variance. Filling up all available storage is a problem. The Merchant’s News gives a hair-raising, but probably accurate, listing of the outcomes of overflowing supply creating price destruction.

Of course, the event that throws a massive monkey wrench into forecasts of crude oil prices is the US capture of Venezuelan President Maduro and his trial in the US. President Trump has indicated that he will have US oil companies take over the operation of extracting Venezuelan oil. The biggest winners of this move will be US Gulf refineries, which are specifically designed to deal with the heavy, sour crude oil from Venezuela. The multiple billions of dollars to get the oil fields running again will produce products selling into very oversupplied markets, making this investment a “gamble” in the phraseology of The Economist. These factors by themselves are enough to make any predictions of crude oil price for 2026 tentative. Because the acknowledgement that it will take at least a year before crude oil flows from Venezuela, perhaps something can still be determined.

Every indication is that crude oil extraction globally is not going to slow down, indicating a further increase in supply. And a slowing down of the global economy will generally decrease demand. Hence, a decrease in oil prices is likely. But that might be a bit too simplistic. A resurgence of Venezuelan oil, even in the unspecified future, might not happen soon enough to make any difference in the supply of crude, no matter how much the market takes the entire future into account. Will some countries, especially OPEC (of which Venezuela is a member), slow down production, expecting more oil coming from Venezuela? Possibly. And a decrease in the cost of crude oil is also likely to help reinvigorate lagging economies (again, except for Russia). An increase in demand is not out of the question.

So, where does this say the price of oil is going to go? The momentum of crude oil prices is clearly downward, and the prospects of reduced supply and increased demand look less likely. If you throw in the chaotic aspect of the weather, the overall direction of crude oil prices is still pretty clearly down.