We’re pleased to announce that the Fundamental Analytics Carbon Services website is now live—explore insights and tools driving carbon compliance and market access here.

The FACS platform, linked to ICE, enables direct EUA trading and streamlined onboarding for compliance markets.

Welcome to our monthly newsletter, Carbon Market News Roundup, the goal of which is to introduce our audience to a new asset class market in the making: the carbon market. Our previous issues, along with the rest of our commentaries, may be read here.

In this month’s edition of Carbon Market News Roundup, we cover key developments shaping compliance and voluntary carbon markets worldwide. From the IMO’s forthcoming framework and the challenges of maritime decarbonization, to EU ETS pricing trends and the latest CBAM updates, the newsletter highlights how regulation and market forces are driving change across shipping, industry, and global trade. We also look at emerging market reforms in Asia, advances in carbon capture and storage in Southeast Asia, and the growing debate around blockchain and tokenization in the voluntary carbon market.

Maritime & Shipping Updates

Top shipping players want overhaul of UN ship fuel emissions deal

Jonathan Saul and Renee Maltezou, Reuters

Significant costs ahead for shipping industry to decarbonize, UNCTAD says

Naida Hakirevic Prevljak, Offshore Energy

Alternative marine fuels uptake will speed up after 2030, shipping executives say

Jeslyn Lerh and Siyi Liu, Reuters

Maritime Decarbonization: Japanese Shipping Giant NYK Partners with 1PointFive for DAC Credits

Saptakee S, Carbon Credits

The UN’s forthcoming Net-Zero Framework (NZF) for international shipping, scheduled for adoption in October, is facing turbulence. Major shipping companies voiced “grave concerns” over its current design, warning it could impose disproportionate costs without ensuring a fair playing field. Their opposition aligns with the U.S., which has threatened retaliatory tariffs and restrictions if the agreement proceeds. The IMO remains confident the deal will be adopted, but resistance from both industry and governments raises questions about whether consensus can be achieved at this critical stage. UNCTAD’s latest Review of Maritime Transport reinforces the scale of the challenge: global shipping emissions rose 5% in 2024. Only 8% of the global fleet is equipped for alternative fuels, while port infrastructure and recycling capacity remain underdeveloped.

Looking further ahead, executives from Maersk, MOL, and other carriers see alternative fuels taking off in earnest after 2030, once regulatory pressure and supply chains mature. LNG and methanol are likely to dominate the near term, while dual-fuel vessels are becoming the default investment to ensure flexibility. In parallel, NYK has deepened its decarbonization strategy by securing carbon removal credits from 1PointFive’s direct air capture project in Texas which marks the second such purchase by the Japanese carrier. This signals an emerging approach: pairing efficiency gains and low-carbon fuels with durable removals to address residual emissions. These developments illustrate how the sector is caught between near-term regulatory disputes and long-term technological transformation, with the pathway to net zero hinging on coordination across policy, finance, and innovation.

EU ETS & CBAM

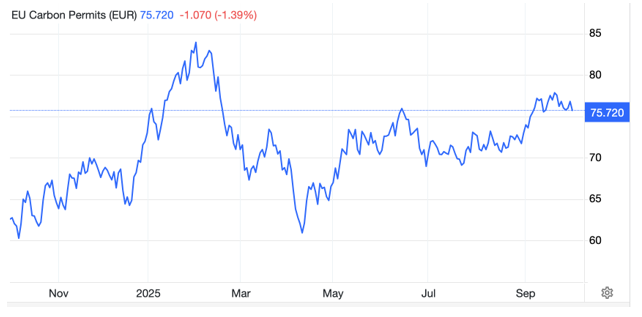

EU Carbon Permits – Price – Chart – Historical Data – News

Trading Economics

There will be no delay to EU CBAM, senior EU official says

Rebecca Gualandi, Carbon Pulse

CBAM impact on US would only be 0.07% of total trade, finds new report

Silvia Andreoletti, Trade Finance Global

EU carbon allowance prices ended September at €75.72/t, down 1.39% on the day but still higher compared to recent months. Over the past month, prices gained 2.4% and remain nearly 19% above the same period last year. The market has trended upward from the lows of early summer, consolidating in the mid-to-high €70s/t through September. Analysts point to subdued industrial demand and steady auction volumes keeping a lid on stronger price moves, while firm power-sector emissions and expectations around tighter supply next year have provided underlying support. With the first maritime ETS compliance deadline now passed, traders are watching whether residual demand from shipping operators and the seasonal shift in the power mix will be sufficient to push EUAs out of their current range. For now, the market appears balanced, with carbon pricing signals broadly stable but sensitive to policy headlines and fourth-quarter energy dynamics.

On the CBAM front, officials in Europe reaffirmed that there will be no delay to CBAM’s full implementation in January 2026. The phased withdrawal of free allowances under the EU ETS and the parallel rollout of CBAM remain central to ensuring the integrity of Europe’s climate ambition. Across the Atlantic, new analysis challenges U.S. criticisms of the EU’s CBAM. A Sandbag report finds that the mechanism would cost U.S. exporters only about £307 million annually (or under 0.2% of total trade volumes), far below earlier claims of £3.5 billion. With U.S. exports of steel, aluminum, and cement already relatively low in emissions, the CBAM could even provide a competitive advantage. While political opposition persists, particularly around regulatory sovereignty, the study shows that U.S. exporters are better positioned than many of their global peers.

Voluntary Market & Emerging Compliance Markets

China’s carbon market set to introduce absolute emissions caps by 2027

Niu Yuhan and Lin Zi, Dialogue Earth

India Sets Up National Designated Authority for Carbon Market Governance

Mercom

Malaysia, Indonesia accelerate carbon capture and storage projects

Nana Shibata and Norman Goh, Nikkei Asia

Carbon Credits Supply to Skyrocket 35x by 2050 – But at What Price?

Saptakee S, Carbon Credits

China and India are both advancing critical reforms that will reshape their carbon markets and global climate positioning. China has announced plans to introduce absolute emissions caps by 2027, expanding coverage to sectors such as chemicals, petrochemicals, papermaking, and aviation. This shift away from its current intensity-based system is expected to tighten supply, lift carbon prices, and strengthen incentives for low-carbon investment, while also responding to external trade pressures like the EU’s CBAM that demand accurate emissions reporting. Meanwhile, India has established a National Designated Authority (NDA) to govern participation under Article 6 of the Paris Agreement, authorizing projects, maintaining registries, and ensuring environmental integrity through corresponding adjustments. By prioritizing sustainable development benefits and building a financial framework for oversight, the NDA aims to accelerate carbon credit trading while keeping India’s NDC commitments at the core.

Malaysia and Indonesia are accelerating carbon capture and storage (CCS) efforts, with Malaysia enacting a comprehensive CCUS Act in 2025 to streamline permitting, enable cross-border CO₂ imports, and support early project bankability through tax incentives. Petronas’ $1.07 billion Kasawari project, slated to inject 3.3 MtCO₂ annually by 2029, highlights the scale of investment, while Indonesia’s BP-led Tangguh project and Pertamina–ExxonMobil ventures show the country’s vast storage potential despite regulatory hurdles. These national initiatives align with a broader global reset in carbon markets: BloombergNEF projects carbon credit supply could increase up to 35-fold by 2050, but with costs diverging sharply depending on project integrity. High-quality credits, especially technology-based removals like direct air capture, could command $100+/t, while lower-quality offsets risk undermining trust despite cheaper prices.

Tokenization of Carbon Credits

Blockchain Put to Use in Voluntary Carbon Market

Shanny Basar, Markets Media

The Problem of Tokenizing Carbon Offset Credits (available at request)

Alfred Evans

Blockchain is increasingly being applied to the voluntary carbon market as developers seek to resolve issues of fragmentation, inefficiency, and lack of transparency. J.P. Morgan’s Kinexys unit is piloting tokenization of carbon credits at the registry layer, embedding credits with standardized metadata such as issuance date, credit type, and location. Northern Trust has similarly expanded its Carbon Ecosystem, enabling near real-time recording and settlement of verified credits using private blockchain infrastructure. These initiatives aim to streamline transactions, create a more unified ecosystem, and support new financial products tied to tokenized credits, while also allowing insurers, rating agencies, and marketplaces to plug directly into digital registries.

Yet despite the promise of efficiency, tokenization alone cannot resolve structural shortcomings in voluntary carbon markets. Critics warn that pooled tokens risk reflecting the price of the lowest-quality credit, discouraging high-quality project developers from participating and deterring buyers who demand co-benefits and robust verification. Experience from earlier offset contracts shows that market integrity often suffers when diverse project types are aggregated under a single price. To succeed, the next generation of carbon-crypto strategies will need to move beyond replicating existing weaknesses, tackling issues of credit quality, fungibility, and reliable price discovery.

Recommended Reads

Long-Term Carbon Credit Supply Outlook 2025

BloombergNEF

CFTC Withdraws Voluntary Carbon Market Guidance

Holland & Knight

Exclusive European carbon market prepares for future changes

Halina Yermolenko, GMK Center

EU’s carbon cost rules are changing: how companies can prepare for CBAM

Valerio Giovannini and Thomas Delille, Reuters