May-26 grains traded under supply pressure: USDA kept wheat/soy balances heavy, and South America remained large. Corn found support from higher exports and ethanol, while Black Sea risks offered intermittent floors.

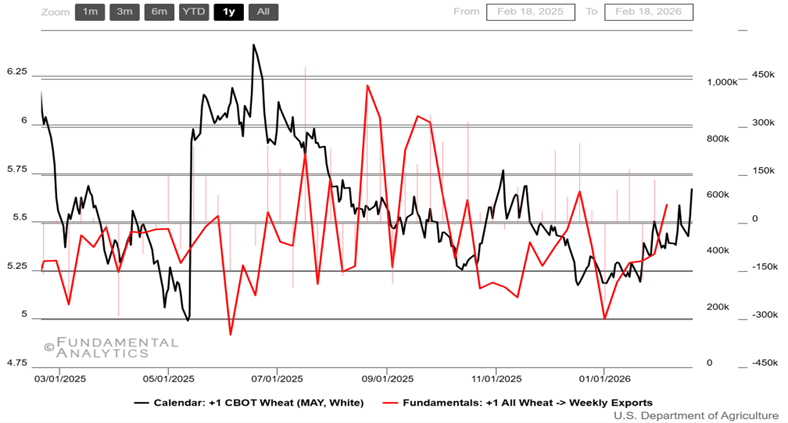

Wheat

May contracts reach 3-month high, as exports amplify

- CBOT May ’26 capped by USDA balance-sheet math: The USDA lifted U.S. ending stocks to 931 mb (largest since 2019/20) on lower domestic use, while world ending stocks stayed a 5-year high even after a small cut, limiting upside follow-through.

- Russia kept export pricing aggressive: The in-quota wheat export duty stayed at zero, and a 20 MMT quota framework took effect, reinforcing the “Black Sea supply overhang” for global tenders.

- Black Sea geopolitics added basis risk, not a structural squeeze: Odesa-area port strikes reduced throughput capacity and raised logistics costs, while storms/ice intermittently slowed regional loadings—supportive on dips, but not enough to change the broader supply narrative.

- Import demand stayed price-led and origin-competitive: Algeria’s OAIC kept tenders active for late-winter/early-spring cover, but the USDA flagged that incremental trade continued to flow toward the cheapest origins (notably Argentina, where exports were raised on competitive offers).

- Weather watch + short covering put a floor under the selloff: Trade commentary pointed to dry-weather monitoring and continued short covering lifting May SRW into the latter part of the window, while Black Sea cold-risk headlines periodically injected a brief risk premium.

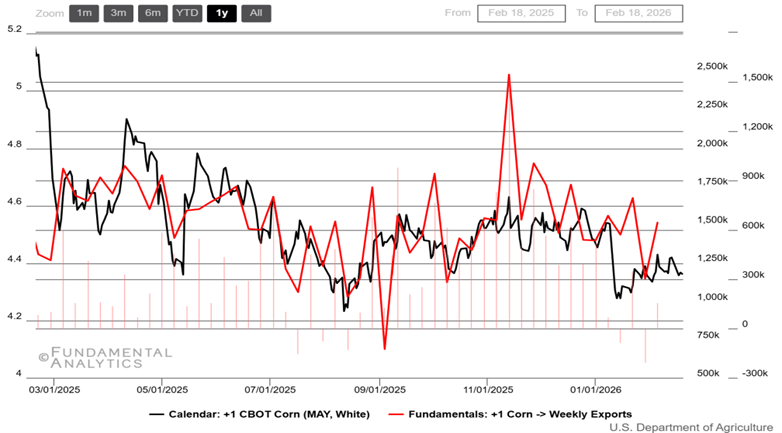

Corn

Corn futures trade below $4.4, but near-term outlook is bullish

- Export-led tightening in the official balance sheet: The USDA raised the 2025/26 U.S. corn export outlook and trimmed ending stocks, improving near-term demand optics for May ’26.

- South America remained the competitiveness anchor: Conab kept Brazil’s 2025/26 corn outlook large with rising export potential, while Argentina weather uncertainty lingered, and a Cargill terminal access dispute in Brazil added episodic logistics noise—overall reinforcing “ample supply, tough competition.”

- Ethanol demand stabilized the downside: U.S. EIA data showed ethanol output rebounding/holding near recent highs, supporting domestic corn grind even as export competition stayed intense.

- Black Sea geopolitics stayed a background bid: Russia strikes on Ukraine’s Black Sea ports cut capacity and raised costs, sustaining a modest risk premium in global feedgrain pricing (supportive on dips for CBOT corn).

- Forward-looking U.S. supply hinted tighter: The USDA outlook commentary pointed to fewer U.S. corn acres in 2026 versus the prior year’s record, a medium-term supportive signal that helped keep May ’26 breaks relatively shallow.

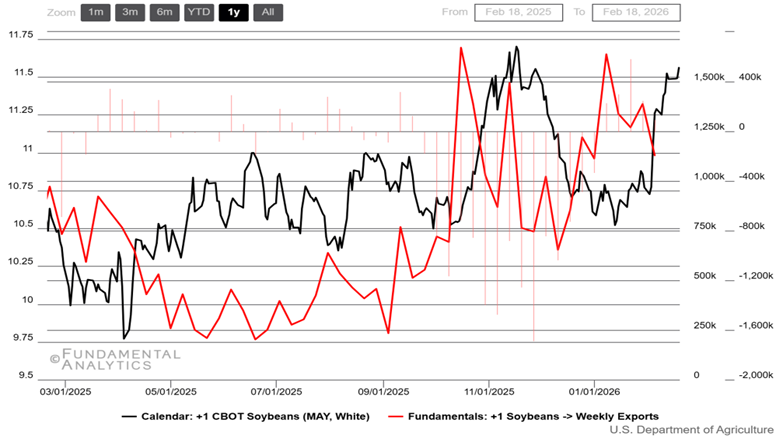

Soybeans

Soybeans prices lift above $11.5 mark after 3 months on Chinese Demand

- USDA February balance sheet felt heavier: Higher global ending stocks (driven by larger South American supply/stocks) and higher palm-oil output assumptions weighed on May ’26 risk-premia.

- Conab confirmed “record-crop” pressure: Near-average harvest progress and record yield expectations reinforced seasonal supply headwinds, even as intermittent rains slowed fieldwork/logistics in spots.

- Argentina weather volatility kept a small premium alive: Drought damage concerns were partially relieved by later rains, but uneven recovery left yield uncertainty in the regional supply outlook.

- China demand headlines swung sentiment, but price reality dominated: Talk of incremental U.S. buying met skepticism after a Supreme Court of the United States tariff ruling reduced leverage, while cheaper South American offers kept buyers selective.

- Crush strong, oil leg capped: The National Oilseed Processors Association reported a record January crush but sharply higher soyoil stocks, while the U.S. Environmental Protection Agency biofuel quota review kept soyoil demand expectations “policy-sensitive,” limiting upside for the bean complex.