Dr. Ken Rietz

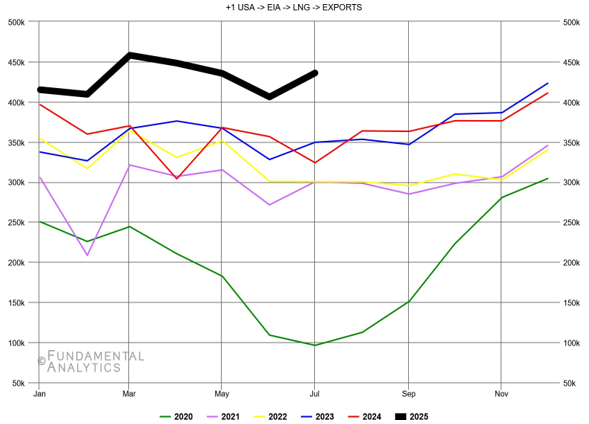

LNG has only recently been used as a method of transporting natural gas, particularly by ocean tankers. Its influence has been dramatic, given its short time span. So, forecasting its degree of use is important to many countries around the world. Two entities, the International Energy Agency (IEA) and the Independent Commodity Intelligence Services (ICIS) have both produced outlooks for LNG to 2050. They aren’t exactly the same; it isn’t realistic to assume they would be. But they are remarkably similar, giving both of them increased credibility. In this article, we will look at the forecasts in some detail. But first, it is important to tell where we are starting from. Here is the graph of US exports of natural gas for the past several years.

Figure 1: Millions of cubic feet of natural gas exported from the US

Except for a dip during the COVID pandemic in March 2020, the amount of natural gas shipped from the US has been increasing rather steadily and rapidly. Starting in 2023, the US has been the top country exporting LNG in the world. The amount of LNG is fairly constant over most years, with no clear seasonality, since most countries importing LNG will try to store LNG for use over a long period of time.

Now, let’s look at the two forecasting entities. The IEA produced World Energy Outlook 2023, and ICIS published 2050 Global LNG Outlook in 2025.

2025–2030

ICIS expects that North American LNG exports will grow rapidly until 2027, mostly due to Mexican and Canadian exports entering in 2026 and due to US exports increasing substantially in 2027. Those countries will supply nearly half of the estimated global increase in LNG supply of 210 million tonnes per year (mt/y) in the next five years. Qatar and Nigeria will supply about a third of the increase, and other Middle East and African countries will fill out the rest. Note that Russian LNG exports (almost 20 mt/y) are excluded by ICIS because of sanctions.

The IEA projections are mostly based on STEPS (the Stated Policies Scenario), although APS (the Announced Pledges Scenario) and NZE (the Net Zero Energy by 2050 scenario) are also included. The IEA looks closely at China, since it caused about a third of the increase in LNG exports in the past few years. The slowing economy in China is a reason to be less optimistic about gains in LNG usage there. The growth of green energy, particularly in the EU, is another reason to soften the growth of LNG exports. For these reasons, the IEA sees LNG growth slowing before 2030, which is similar to the ICIS prediction, but with less detail.

2030–2040

The ICIS predictions for this decade are appropriately wrapped in cautions. The overall problem of pumping natural gas from existing wells for many years must be taken into account, so they predict a reduction of LNG exports from Asia and Australia. On the other hand, North American LNG is expected to rise, but not enough to counter the decline elsewhere. Overall, the global export of LNG is expected to be 388 mt/y at the start of the decade and drop to 361 mt/y, a drop of about 1% per year. This will also trigger longer shipping distances, adding a bit more delay in shipments. Taking into account the time lag from FID to production, ICIS predicts that there will be a tightening of the LNG market around 2037.

The IEA again worries about the slowing of the Chinese economy in this decade. China has been a major instrument of change in the LNG (and indeed in all energy as well) world, but China itself is now changing and slowing down. Seeing this current trend back in 2023 is impressive. As China moves more toward green energy, its dependence on, and therefore import of LNG, is expected to drop. It will not go to zero, since LNG is also used as a source material for physical objects, such as plastics. The net result is that the demand for LNG will drop well below the supply, and prices will drop a lot.

2040–2050

The ICIS predicts that the total global supply of LNG in 2040 to be 564 mt/y, and dropping by 1% per year until at least 2050. This will lead to a restructuring of the major LNG producers, such as Qatar, well before 2045. The global LNG market will grow by only 0.2% year-over-year. The two major markets for LNG (northeast Asia and Europe) will shift to the rest of Asia, Africa, and the Middle East. The need for LNG will continue to grow in size, value, and relevance during this time.

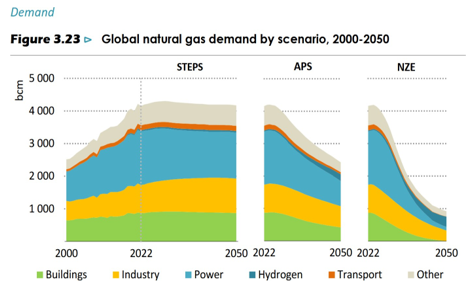

The IEA predictions diverge considerably for this decade, as seen in this graph.

Figure 2: LNG predicted use, different scenarios. Source: IEA

The driving factor in the APS and NZE scenarios is reduced amounts of LNG needed due to the decreasing need for fossil fuels as the world shifts to green energy. The IEA gives no particular weight to which scenario they expect. They simply show the consequences of differing scenarios, and leave the reader to discover the results of their different assumptions.

Trading

In terms of trading, this entire commentary is filled with directions that the LNG market is expected to move. To be more explicit, the predictions for 2025–2030 can be translated into potential trades. It is not possible to buy directly Mexican, Canadian, or Chinese LNG futures, but you can buy options on big Mexican, Canadian, or some Chinese LNG companies. And you can certainly buy US LNG futures, which are likely to move lower with the actual increasing supply, or the expectation of increasing supply, of LNG in 2026 and 2027.